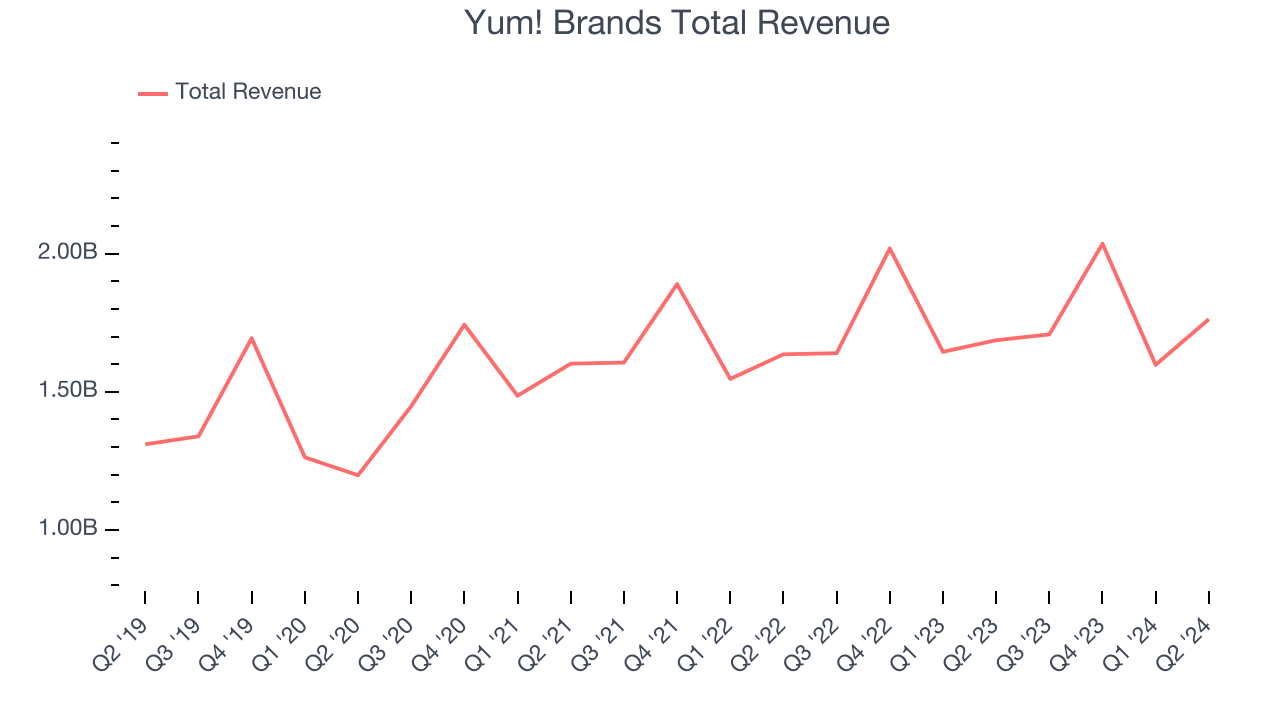

Fast-food company Yum! Brands (NYSE:YUM) fell short of analysts' expectations in Q2 CY2024, with revenue up 4.5% year on year to $1.76 billion. It made a non-GAAP profit of $1.35 per share, down from its profit of $1.44 per share in the same quarter last year.

Is now the time to buy Yum! Brands? Find out by accessing our full research report, it's free.

Yum! Brands (YUM) Q2 CY2024 Highlights:

- Revenue: $1.76 billion vs analyst estimates of $1.80 billion (2.2% miss)

- Operating Profit: $607 million vs analyst estimates of $607 million (in line)

- EPS (non-GAAP): $1.35 vs analyst estimates of $1.33 (1.4% beat)

- Gross Margin (GAAP): 49.3%, down from 50.5% in the same quarter last year

- Free Cash Flow of $292 million, similar to the previous quarter

- Locations: 59,118 at quarter end, up from 56,425 in the same quarter last year

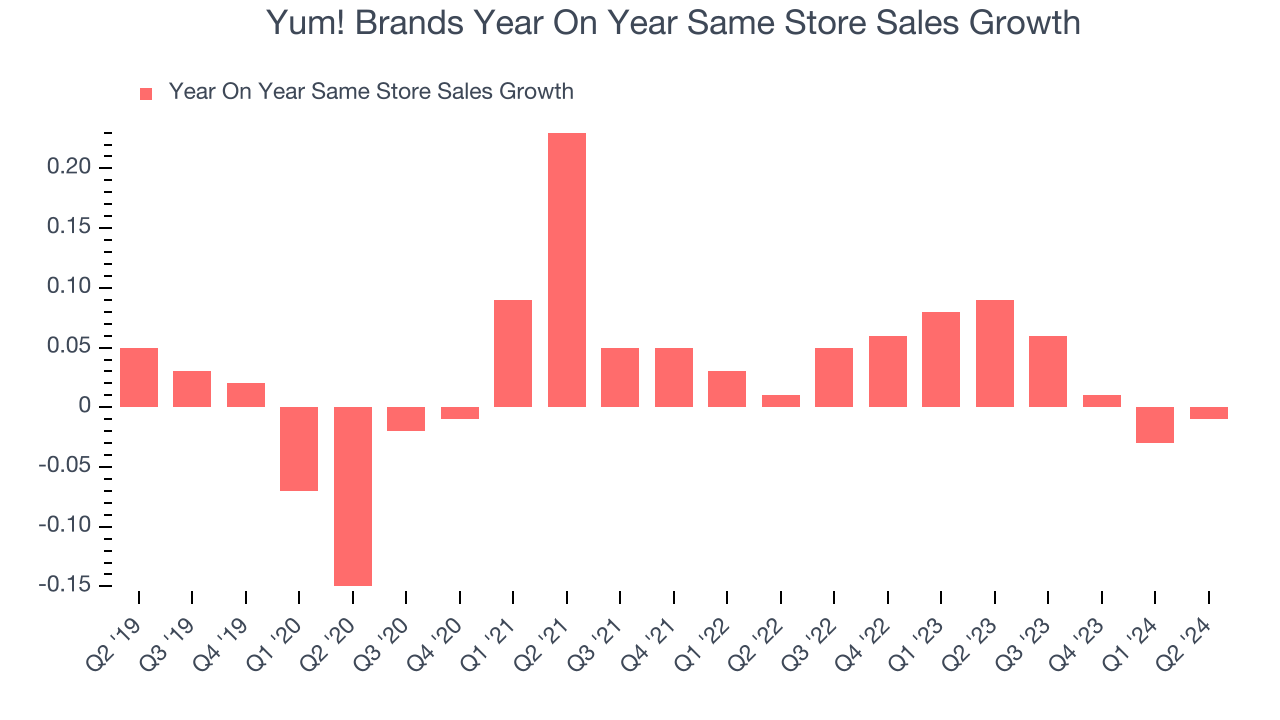

- Same-Store Sales fell 1% year on year (9% in the same quarter last year)

- Market Capitalization: $37.55 billion

Spun off as an independent company from PepsiCo, Yum! Brands (NYSE:YUM) is a multinational corporation that owns KFC, Pizza Hut, Taco Bell, and The Habit Burger Grill.

Traditional Fast Food

Traditional fast-food restaurants are renowned for their speed and convenience, boasting menus filled with familiar and budget-friendly items. Their reputations for on-the-go consumption make them favored destinations for individuals and families needing a quick meal. This class of restaurants, however, is fighting the perception that their meals are unhealthy and made with inferior ingredients, a battle that's especially relevant today given the consumers increasing focus on health and wellness.

Sales Growth

Yum! Brands is one of the most widely recognized restaurant chains in the world and benefits from brand equity, giving it customer loyalty and more influence over purchasing decisions.

As you can see below, the company's annualized revenue growth rate of 5.2% over the last five years was sluggish, but to its credit, it opened new restaurants and grew sales at existing, established dining locations.

This quarter, Yum! Brands's revenue grew 4.5% year on year to $1.76 billion, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 13.2% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Yum! Brands's demand within its existing restaurants has generally risen over the last two years but lagged behind the broader sector. On average, the company's same-store sales have grown by 3.9% year on year. With positive same-store sales growth amid an increasing number of restaurants, Yum! Brands is reaching more diners and growing sales.

In the latest quarter, Yum! Brands's year on year same-store sales were flat. By the company's standards, this growth was a meaningful deceleration from the 9% year-on-year increase it posted 12 months ago. We'll be watching Yum! Brands closely to see if it can reaccelerate growth.

Key Takeaways from Yum! Brands's Q2 Results

We were impressed by how significantly Yum! Brands blew past analysts' gross margin expectations this quarter. On the other hand, its revenue unfortunately missed analysts' expectations. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on track. The market was likely expecting more, and the stock traded down 2.2% to $130.50 immediately following the results.

So should you invest in Yum! Brands right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.