Subscription management platform Zuora (NYSE:ZUO) fell short of analysts' expectations in Q2 FY2024, with revenue up 9.39% year on year to $108 million. Next quarter's outlook also missed expectations with revenue guided to $108.5 million at the midpoint, or 2.06% below analysts' estimates. Zuora made a GAAP loss of $22.6 million, improving from its loss of $29.9 million in the same quarter last year.

Is now the time to buy Zuora? Find out by accessing our full research report, it's free.

Zuora (ZUO) Q2 FY2024 Highlights:

- Revenue: $108 million vs analyst estimates of $108.8 million (0.69% miss)

- EPS (non-GAAP): $0.07 vs analyst estimates of $0.04 ($0.04 beat)

- Revenue Guidance for Q3 2024 is $108.5 million at the midpoint, below analyst estimates of $110.8 million

- The company dropped revenue guidance for the full year from $435.5 million to $430.5 million at the midpoint, a 1.15% decrease

- Free Cash Flow of $4.02 million, down 69% from the previous quarter

- Net Revenue Retention Rate: 107%, in line with the previous quarter

- Gross Margin (GAAP): 65%, up from 60.9% in the same quarter last year

“The second quarter was another solid quarter. We executed on our strategy and delivered on our guidance,” said Tien Tzuo, Founder and CEO of Zuora. “As the world continues to embrace recurring revenue, companies are coming to Zuora for our differentiated, hard-to-replicate technology. Our amazing list of customers is helping us build a long-term, durable business.”

Founded in 2007, Zuora (NYSE:ZUO) offers software as a service platform that allows companies to bill and accept payments for recurring subscription products.

Consumers want the ability to make payments whenever and wherever they prefer – and to do so without having to worry about fraud or other security threats. However, building payments infrastructure from scratch is extremely resource-intensive for engineering teams. That drives demand for payments platforms that are easy to integrate into consumer applications and websites.

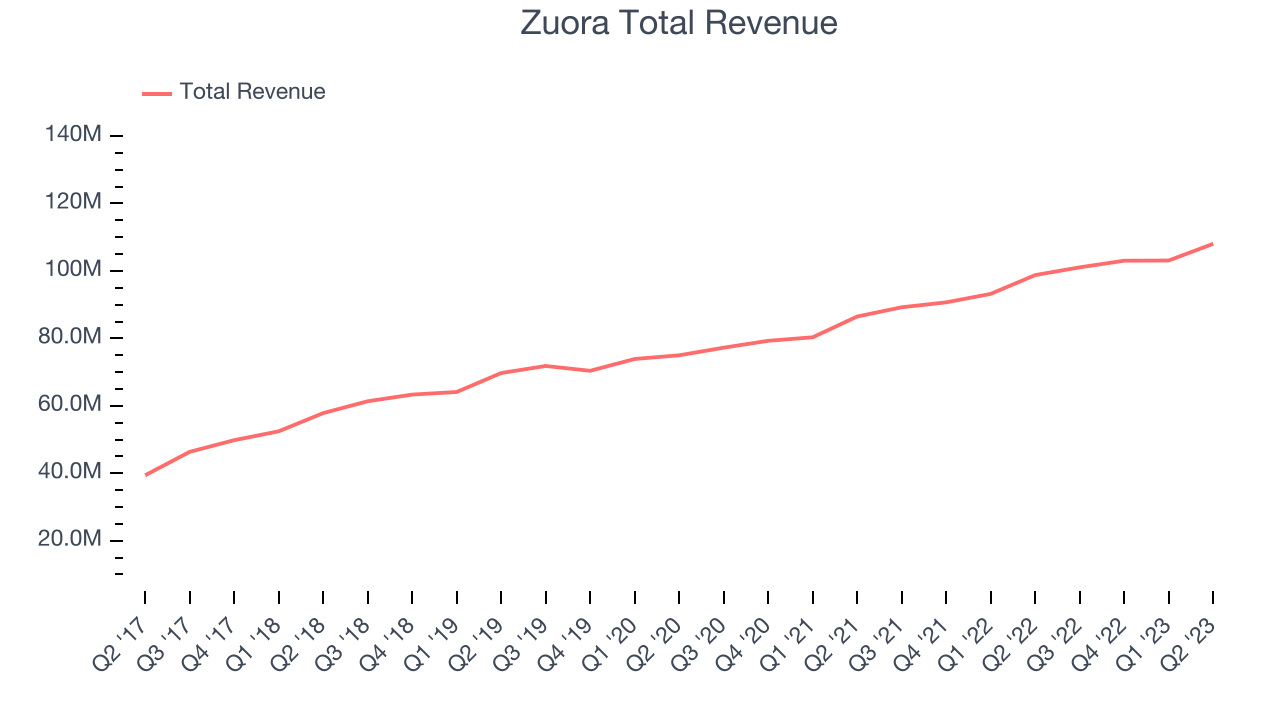

Sales Growth

As you can see below, Zuora's revenue growth has been mediocre over the last two years, growing from $86.5 million in Q2 FY2022 to $108 million this quarter.

Zuora's quarterly revenue was only up 9.39% year on year, which might disappoint some shareholders. However, we can see that the company's revenue grew by $4.95 million quarter on quarter, accelerating from $54 thousand in Q1 2024.

Next quarter's guidance suggests that Zuora is expecting revenue to grow 7.35% year on year to $108.5 million, slowing down from the 13.3% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 10.6% over the next 12 months before the earnings results announcement.

The pandemic fundamentally changed several consumer habits. There is a founder-led company that is massively benefiting from this shift. The business has grown astonishingly fast, with 40%+ free cash flow margins. Its fundamentals are undoubtedly best-in-class. Still, the total addressable market is so big that the company has room to grow many times in size. You can find it on our platform for free.

Key Takeaways from Zuora's Q2 Results

With a market capitalization of $1.37 billion, Zuora is among smaller companies, but its more than $323.3 million in cash on hand and near break-even free cash flow margins put it in a stable financial position.

It was great to see Zuora improve its gross margin this quarter. That really stood out as a positive in these results. On the other hand, its full-year revenue guidance was below expectations and its revenue guidance for next quarter missed Wall Street's estimates. However, investors should note that this drop stems from lower-than-expected professional services revenue, which is lower margin than the company's subscription revenue. Thus, Zuora is still raising its adjusted operating income and EPS guidance. Despite this, the market was likely looking for stronger top-line growth and company is down 4.44% on the results. It currently trades at $9.25 per share.

Zuora may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.

One way to find opportunities in the market is to watch for generational shifts in the economy. Almost every company is slowly finding itself becoming a technology company and facing cybersecurity risks and as a result, the demand for cloud-native cybersecurity is skyrocketing. This company is leading a massive technological shift in the industry and with revenue growth of 50% year on year and best-in-class SaaS metrics it should definitely be on your radar.

The author has no position in any of the stocks mentioned in this report.