Zeta Global presents an unusual valuation puzzle. While AI infrastructure companies—those selling chips and cloud computing—command valuations of 10-20x sales, Zeta trades at 3.2x despite actually deploying AI to generate revenue today. This discount appears to reflect the market's focus on AI infrastructure over applications—a gap that we believe should narrow as investors increasingly recognize the value of companies already monetizing AI at scale. This report examines why Zeta's combination of execution, growth, and valuation merits serious consideration.

Company Overview

Co-founded by former Apple CEO John Sculley, Zeta Global (NYSE:ZETA) provides software and data analytics tools that help companies market their products to billions of customers.

As customers have increasingly moved online, more data has become available to businesses, which allows them to market their products. Zeta Global helps businesses utilize this data to market more effectively.

Today, much of what we do on the internet can be tracked and used to determine what types of products we may be interested in. Historically, brands had very limited data on who their customers were and how they were reaching them. With old advertising methods such as billboards and television ads, businesses had no way of ensuring that the people who saw their ads would be their target customers.

Using trillions of data points from activity across the internet, Zeta Global determines which customers would be interested in which products and helps businesses find customers that are most likely to buy their products.

1. Why We Like Zeta Global

Powered by an AI engine that processes over one trillion consumer signals monthly, Zeta Global (NYSE:ZETA) operates a data-driven cloud platform that helps companies target, connect, and engage with consumers through personalized marketing across channels like email, social media, and video.

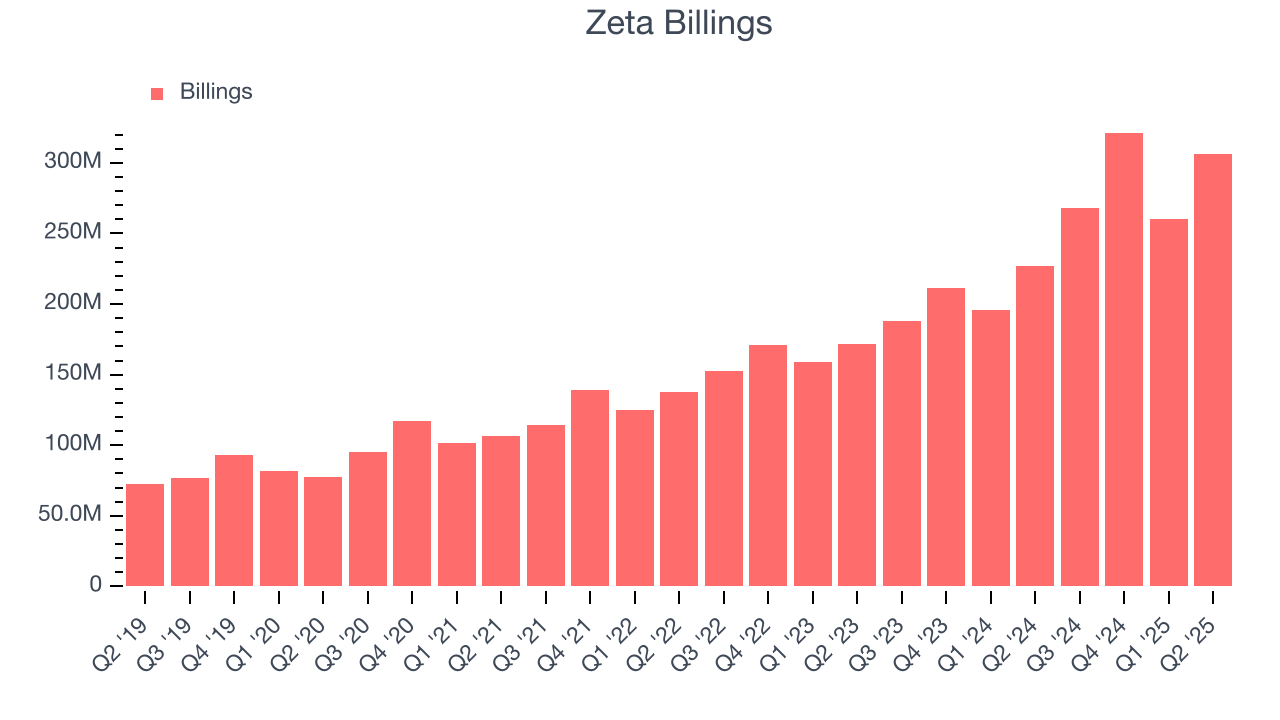

- Winning new contracts that can potentially increase in value as its billings growth has averaged 40.6% over the last year

- User-friendly software enables clients to ramp up spending quickly, leading to the speedy recovery of customer acquisition costs

- Sales outlook for the upcoming 12 months implies the business will stay on its desirable two-year growth trajectory

2. Why Is Now The Time To Buy Zeta Global?

Zeta Global’s stock price of $20.50 implies a valuation ratio of 3.2x forward price-to-sales. This valuation is attractive, and we think the stock is likely trading below its intrinsic value when considering its fundamentals.

A powerful double-play is a business that can both grow earnings and achieve a loftier multiple over time. Elite companies trading at meaningful discounts are good ways to set up this play.

3. Zeta Global (ZETA) Research Report: Q2 CY2025 Update

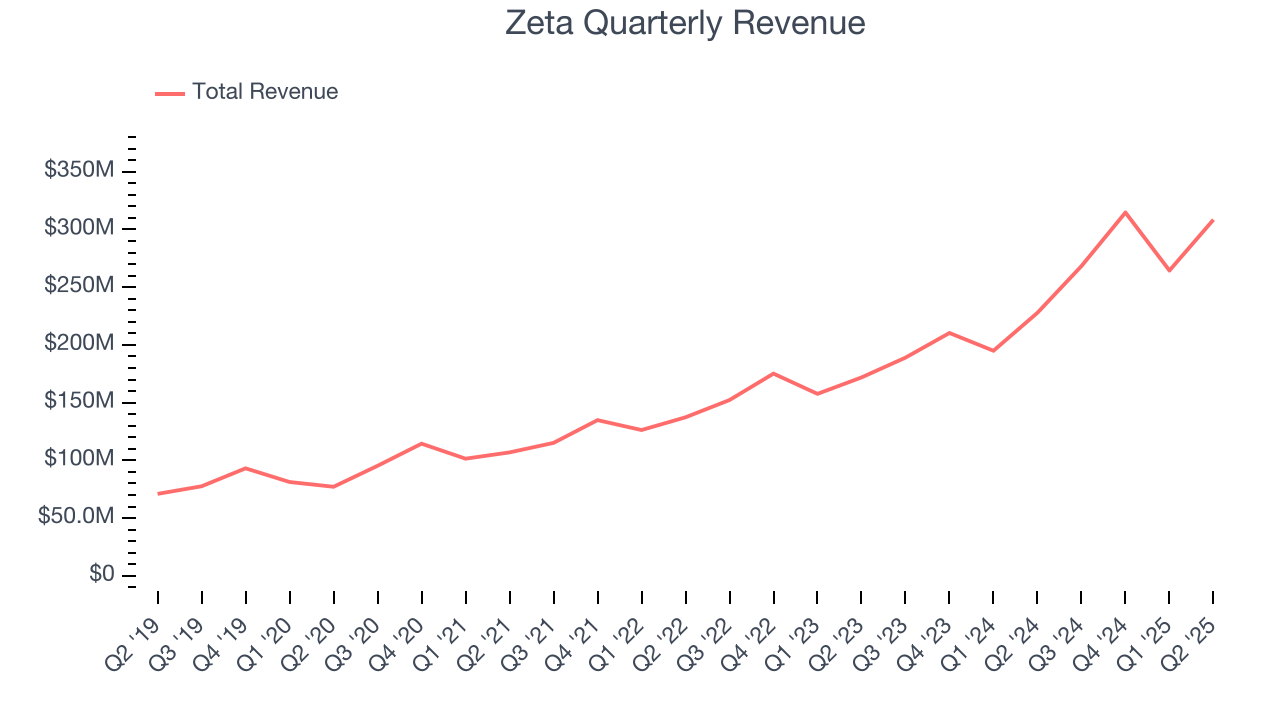

Advertising and marketing company Zeta Global (NYSE:ZETA) announced better-than-expected revenue in Q2 CY2025, with sales up 35.4% year on year to $308.4 million. Guidance for next quarter’s revenue was better than expected at $328 million at the midpoint, 1.2% above analysts’ estimates.

4. Advertising Software

The digital advertising market is large, growing, and becoming more diverse, both in terms of audiences and media. As a result, there is a growing need for software that enables advertisers to use data to automate and optimize ad placements.

Other providers of sales and marketing solutions include AppLovin (NASDAQ:APP), DoubleVerify (NYSE:DV), LiveRamp (NYSE:RAMP), PubMatic (NASDAQ:PUBM), The Trade Desk (NASDAQ:TTD)

5. Revenue Growth

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Luckily, Zeta’s sales grew at an impressive 31.1% compounded annual growth rate over the last three years. Its growth beat the average software company and shows its offerings resonate with customers.

This quarter, Zeta reported wonderful year-on-year revenue growth of 35.4%, and its $308.4 million of revenue exceeded Wall Street’s estimates by 3.9%. Company management is currently guiding for a 22.3% year-on-year increase in sales next quarter.

Looking further ahead, sell-side analysts expect revenue to grow 16% over the next 12 months, a deceleration versus the last three years. Despite the slowdown, this projection is noteworthy and indicates the market is forecasting success for its products and services.

6. Billings

Billings is a non-GAAP metric that is often called “cash revenue” because it shows how much money the company has collected from customers in a certain period. This is different from revenue, which must be recognized in pieces over the length of a contract.

Zeta’s billings punched in at $306.3 million in Q2, and over the last four quarters, its growth was fantastic as it averaged 40.6% year-on-year increases. This performance aligned with its total sales growth, indicating robust customer demand. The high level of cash collected from customers also enhances liquidity and provides a solid foundation for future investments and growth.

7. Customer Acquisition Efficiency

The customer acquisition cost (CAC) payback period measures the months a company needs to recoup the money spent on acquiring a new customer. This metric helps assess how quickly a business can break even on its sales and marketing investments.

Zeta is extremely efficient at acquiring new customers, and its CAC payback period checked in at 4.6 months this quarter. The company’s rapid recovery of its customer acquisition costs indicates it has a highly differentiated product offering and a strong brand reputation. These dynamics give Zeta more resources to pursue new product initiatives while maintaining the flexibility to increase its sales and marketing investments.

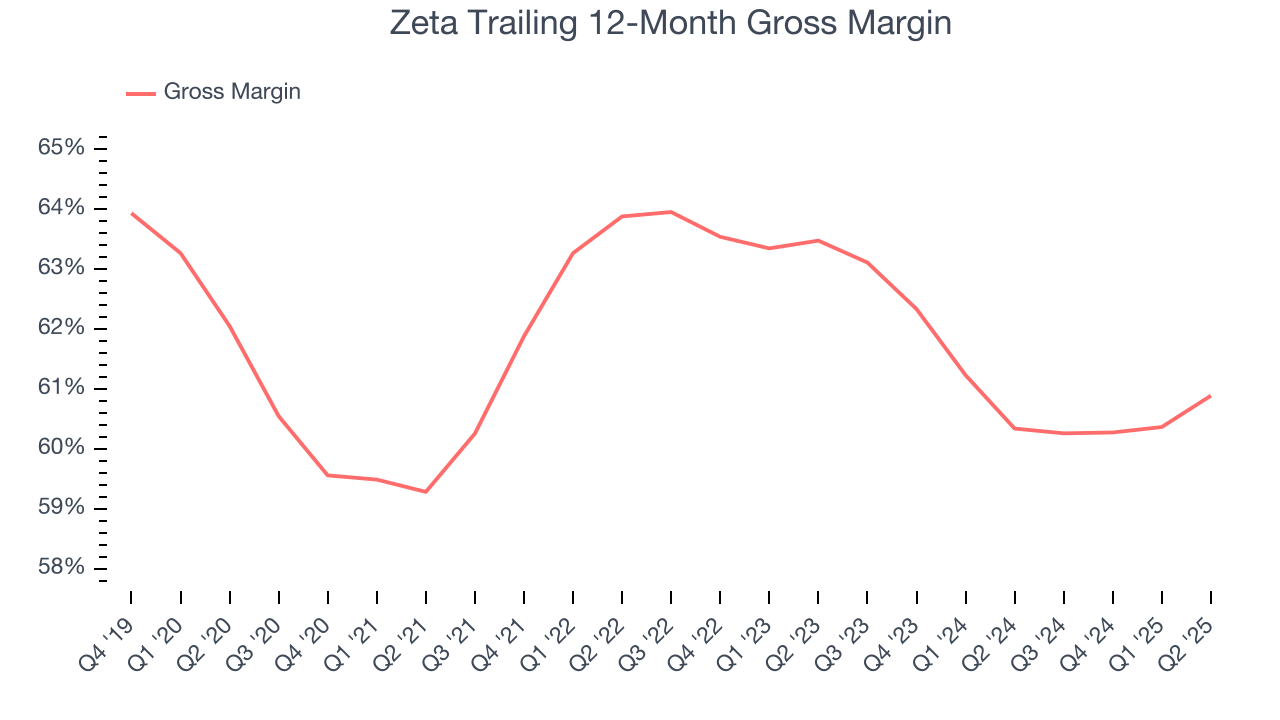

8. Gross Margin & Pricing Power

For software companies like Zeta, gross profit tells us how much money remains after paying for the base cost of products and services (typically servers, licenses, and certain personnel). These costs are usually low as a percentage of revenue, explaining why software is more lucrative than other sectors.

Zeta’s gross margin is substantially worse than most software businesses, signaling it has relatively high infrastructure costs compared to asset-lite businesses like ServiceNow. As you can see below, it averaged a 60.9% gross margin over the last year. That means Zeta paid its providers a lot of money ($39.11 for every $100 in revenue) to run its business.

In Q2, Zeta produced a 62.1% gross profit margin, marking a 2 percentage point increase from 60% in the same quarter last year. On a wider time horizon, the company’s full-year margin has remained steady over the past four quarters, suggesting its input costs have been stable and it isn’t under pressure to lower prices.

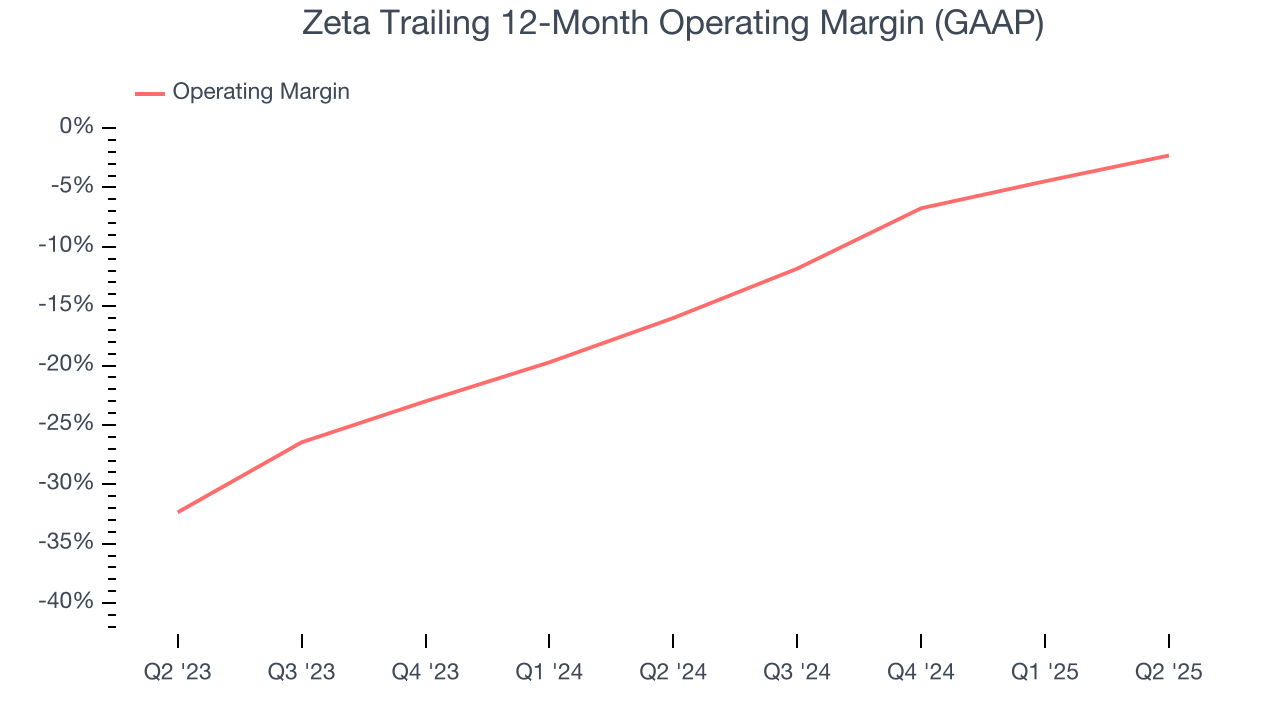

9. Operating Margin

Zeta’s expensive cost structure has contributed to an average operating margin of negative 2.3% over the last year. Unprofitable, high-growth software companies require extra attention because they spend heaps of money to capture market share. As seen in its fast historical revenue growth, this strategy seems to have worked so far, but it’s unclear what would happen if Zeta reeled back its investments. Wall Street seems to be optimistic about its growth, but we have some doubts.

Over the last year, Zeta’s expanding sales gave it operating leverage as its margin rose by 13.7 percentage points. Still, it will take much more for the company to reach long-term profitability.

This quarter, Zeta generated a negative 1.7% operating margin.

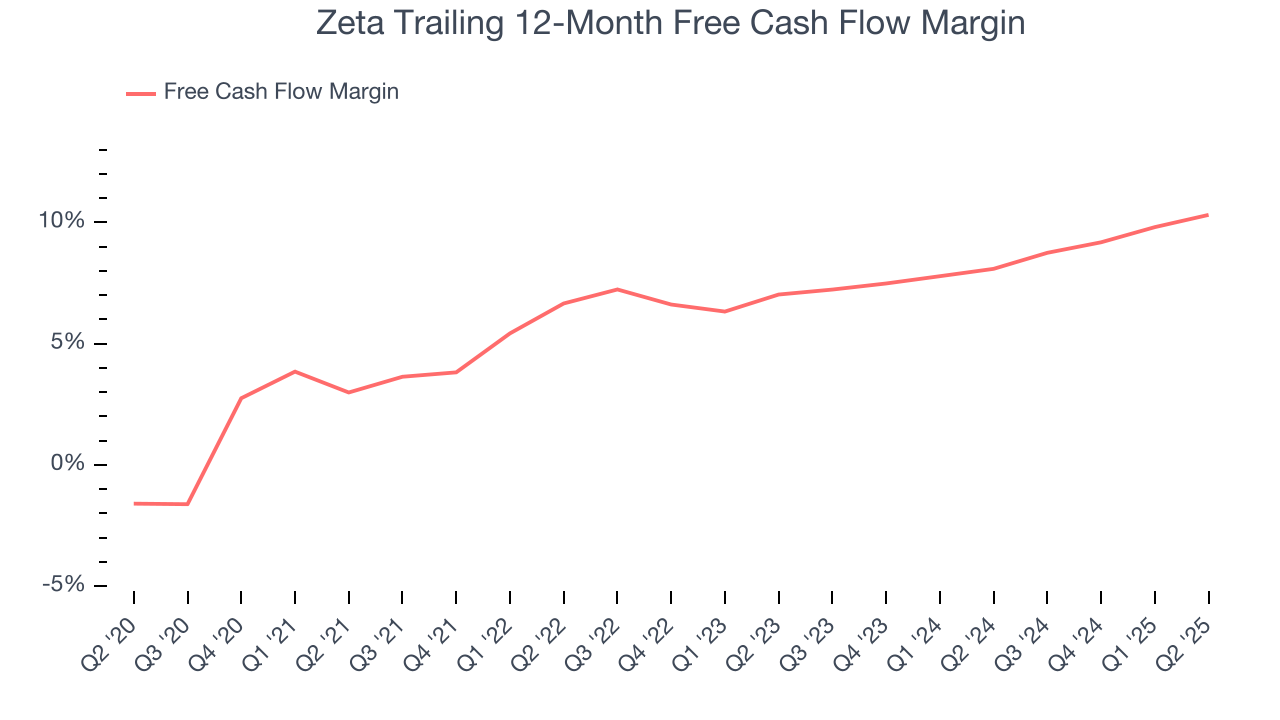

10. Cash Is King

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Zeta has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company’s free cash flow margin averaged 10.3% over the last year, slightly better than the broader software sector.

Zeta’s free cash flow clocked in at $33.56 million in Q2, equivalent to a 10.9% margin. This result was good as its margin was 2.2 percentage points higher than in the same quarter last year, but we wouldn’t put too much weight on the short term because investment needs can be seasonal, causing temporary swings. Long-term trends carry greater meaning.

Over the next year, analysts’ consensus estimates show they’re expecting Zeta’s free cash flow margin of 10.3% for the last 12 months to remain the same.

11. Balance Sheet Assessment

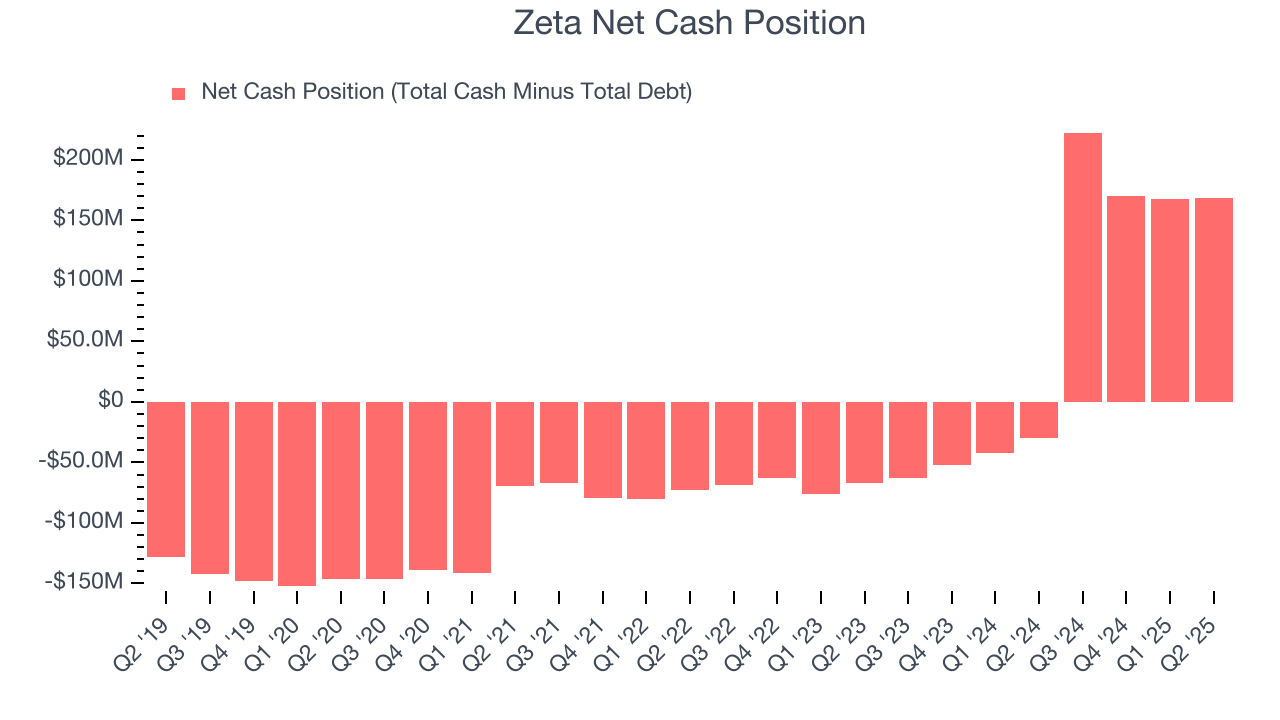

Companies with more cash than debt have lower bankruptcy risk.

Zeta is a well-capitalized company with $365.3 million of cash and $196.7 million of debt on its balance sheet. This $168.6 million net cash position is 4.5% of its market cap and gives it the freedom to borrow money, return capital to shareholders, or invest in growth initiatives. Leverage is not an issue here.

12. Key Takeaways from Zeta’s Q2 Results

This was a beat and raise quarter. We enjoyed seeing Zeta beat analysts’ EBITDA expectations this quarter. We were also glad its full-year EBITDA guidance exceeded Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The stock traded up 5.8% to $16.80 immediately following the results.

13. Is Now The Time To Buy Zeta Global?

Before making an investment decision, investors should account for Zeta Global’s business fundamentals and valuation in addition to what happened in the latest quarter.

There are several reasons why we think Zeta Global is a great business. For starters, its revenue growth was strong over the last five years. And while its gross margins show its business model is much less lucrative than other companies, its efficient sales strategy allows it to target and onboard new users at scale. On top of that, Zeta Global’s expanding operating margin shows it’s becoming more efficient at building and selling its software.

Zeta Global’s price-to-sales ratio based on the next 12 months is 3.2x. Looking across the spectrum of software companies today, Zeta Global’s fundamentals shine bright. We like the stock at this price.