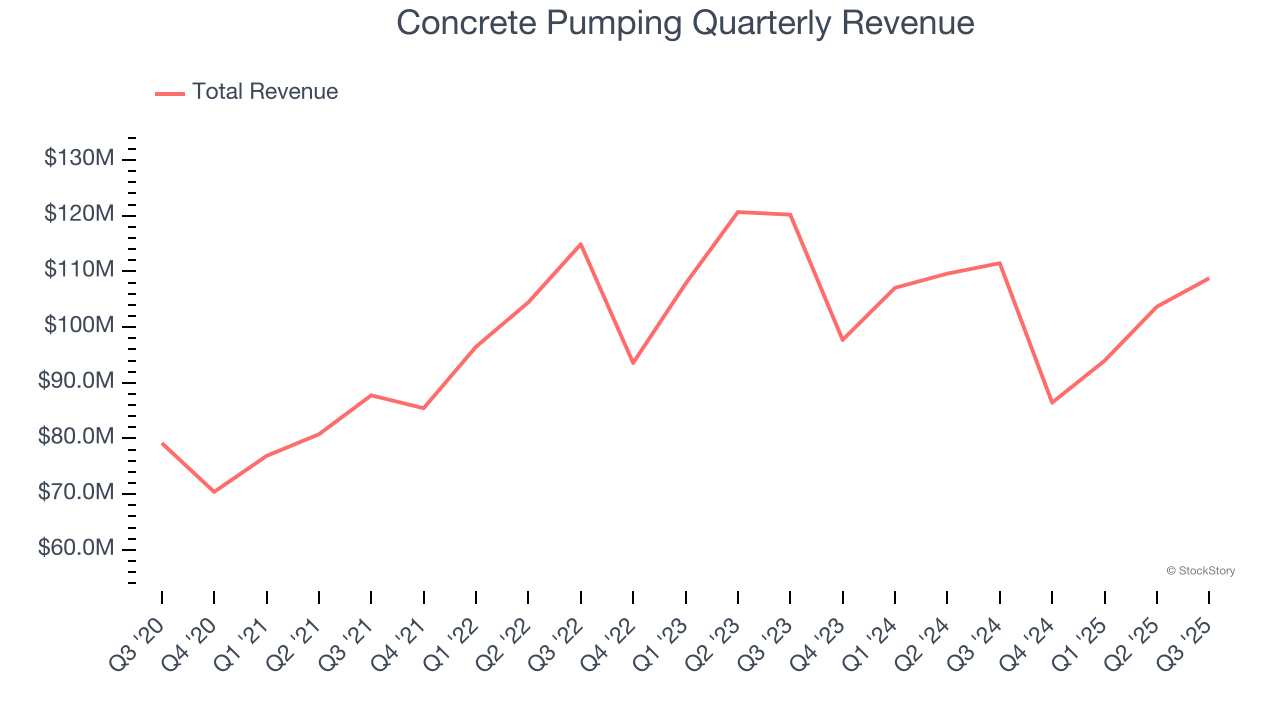

Concrete and waste management company Concrete Pumping (NASDAQ:BBCP) reported Q3 CY2025 results exceeding the market’s revenue expectations, but sales fell by 2.4% year on year to $108.8 million. The company’s full-year revenue guidance of $400 million at the midpoint came in 2% above analysts’ estimates. Its GAAP profit of $0.09 per share was in line with analysts’ consensus estimates.

Is now the time to buy Concrete Pumping? Find out by accessing our full research report, it’s free.

Concrete Pumping (BBCP) Q3 CY2025 Highlights:

- Revenue: $108.8 million vs analyst estimates of $102.9 million (2.4% year-on-year decline, 5.7% beat)

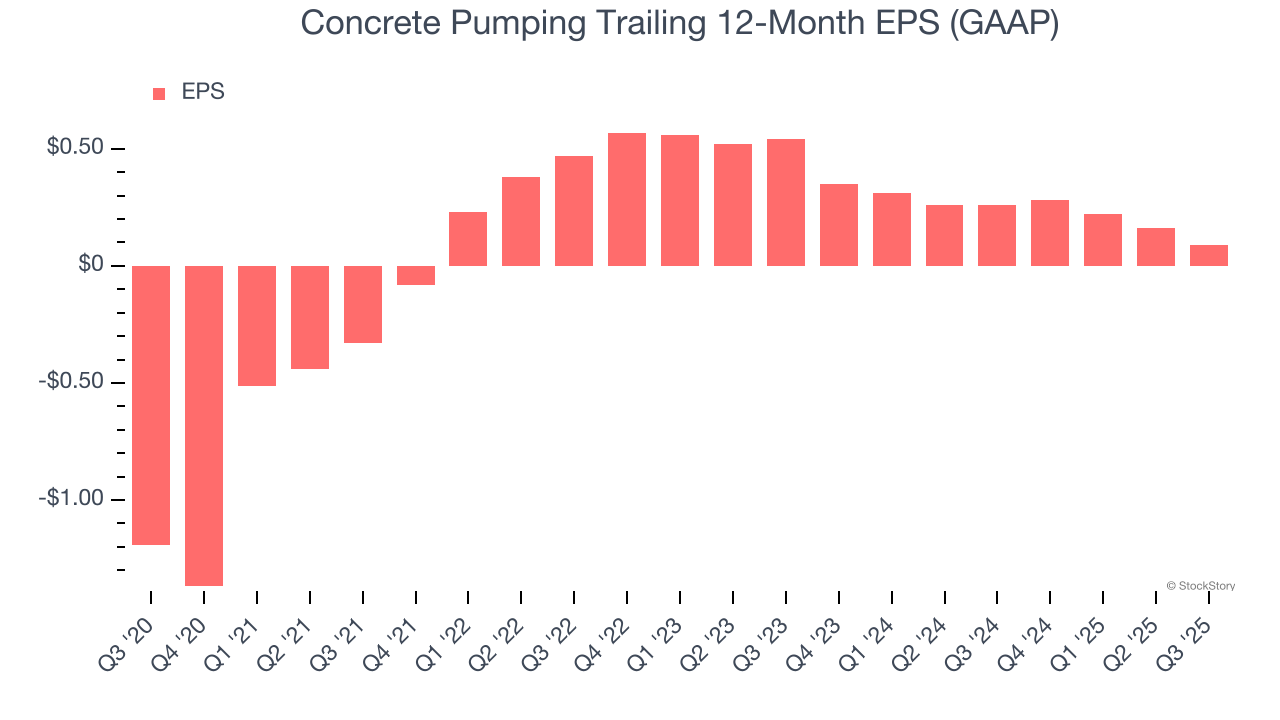

- EPS (GAAP): $0.09 vs analyst estimates of $0.09 (in line)

- Adjusted EBITDA: $30.67 million vs analyst estimates of $28.9 million (28.2% margin, 6.1% beat)

- EBITDA guidance for the upcoming financial year 2026 is $95 million at the midpoint, below analyst estimates of $102.1 million

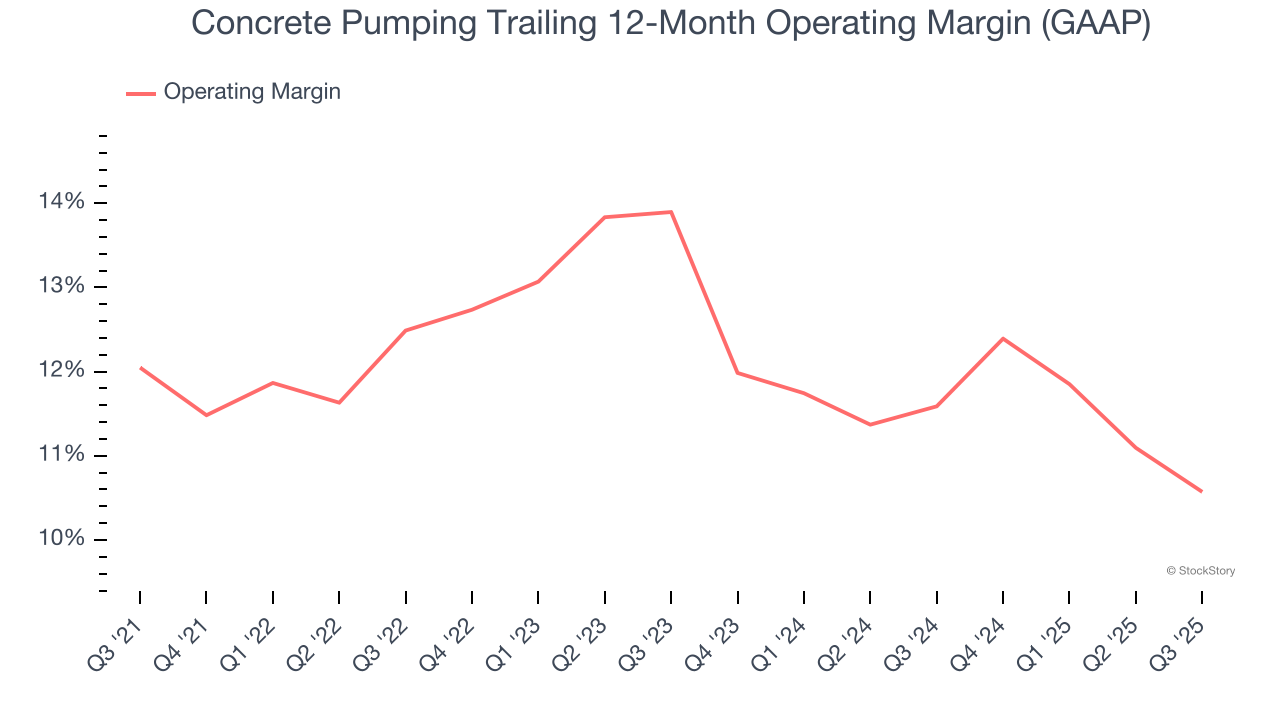

- Operating Margin: 15.5%, down from 17.2% in the same quarter last year

- Free Cash Flow Margin: 1.8%, down from 14.4% in the same quarter last year

- Market Capitalization: $386.1 million

"This quarter, our results again reflected the resilience and adaptability of our business model amid persistent macroeconomic challenges," said CPH CEO Bruce Young.

Company Overview

Going public via SPAC in 2018, Concrete Pumping (NASDAQ:BBCP) is a provider of concrete pumping and waste management services in the United States and the United Kingdom.

Revenue Growth

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Concrete Pumping grew its sales at a tepid 5.2% compounded annual growth rate. This was below our standard for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Concrete Pumping’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 5.7% annually.

This quarter, Concrete Pumping’s revenue fell by 2.4% year on year to $108.8 million but beat Wall Street’s estimates by 5.7%.

Looking ahead, sell-side analysts expect revenue to remain flat over the next 12 months. While this projection indicates its newer products and services will spur better top-line performance, it is still below average for the sector.

Microsoft, Alphabet, Coca-Cola, Monster Beverage—all began as under-the-radar growth stories riding a massive trend. We’ve identified the next one: a profitable AI semiconductor play Wall Street is still overlooking. Go here for access to our full report.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

Concrete Pumping has been an efficient company over the last five years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 12.2%. This result isn’t surprising as its high gross margin gives it a favorable starting point.

Analyzing the trend in its profitability, Concrete Pumping’s operating margin decreased by 1.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability.

This quarter, Concrete Pumping generated an operating margin profit margin of 15.5%, down 1.7 percentage points year on year. Since Concrete Pumping’s operating margin decreased more than its gross margin, we can assume it was less efficient because expenses such as marketing, R&D, and administrative overhead increased.

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Concrete Pumping’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Concrete Pumping, its EPS declined by more than its revenue over the last two years, dropping 59.2%. This tells us the company struggled to adjust to shrinking demand.

In Q3, Concrete Pumping reported EPS of $0.09, down from $0.16 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Concrete Pumping’s full-year EPS of $0.09 to grow 74.1%.

Key Takeaways from Concrete Pumping’s Q3 Results

We were impressed by how significantly Concrete Pumping blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. On the other hand, its full-year EBITDA guidance missed. Overall, we think this was still a solid quarter with some key areas of upside. Investors were likely hoping for more, and shares traded down 3.4% to $7.16 immediately following the results.

So do we think Concrete Pumping is an attractive buy at the current price? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here (it’s free).