Since February 2021, the S&P 500 has delivered a total return of 73.6%. But one standout stock has nearly doubled the market - over the past five years, Popular has surged 131% to $146.02 per share. Its momentum hasn’t stopped as it’s also gained 27.4% in the last six months thanks to its solid quarterly results, beating the S&P by 20.8%.

Is now still a good time to buy BPOP? Or is this a case of a company fueled by heightened investor enthusiasm? Find out in our full research report, it’s free.

Why Is Popular a Good Business?

Founded in 1893 as the first bank in Puerto Rico to serve the working class, Popular (NASDAQ:BPOP) is a financial holding company that provides retail, mortgage, and commercial banking services primarily in Puerto Rico and the mainland United States.

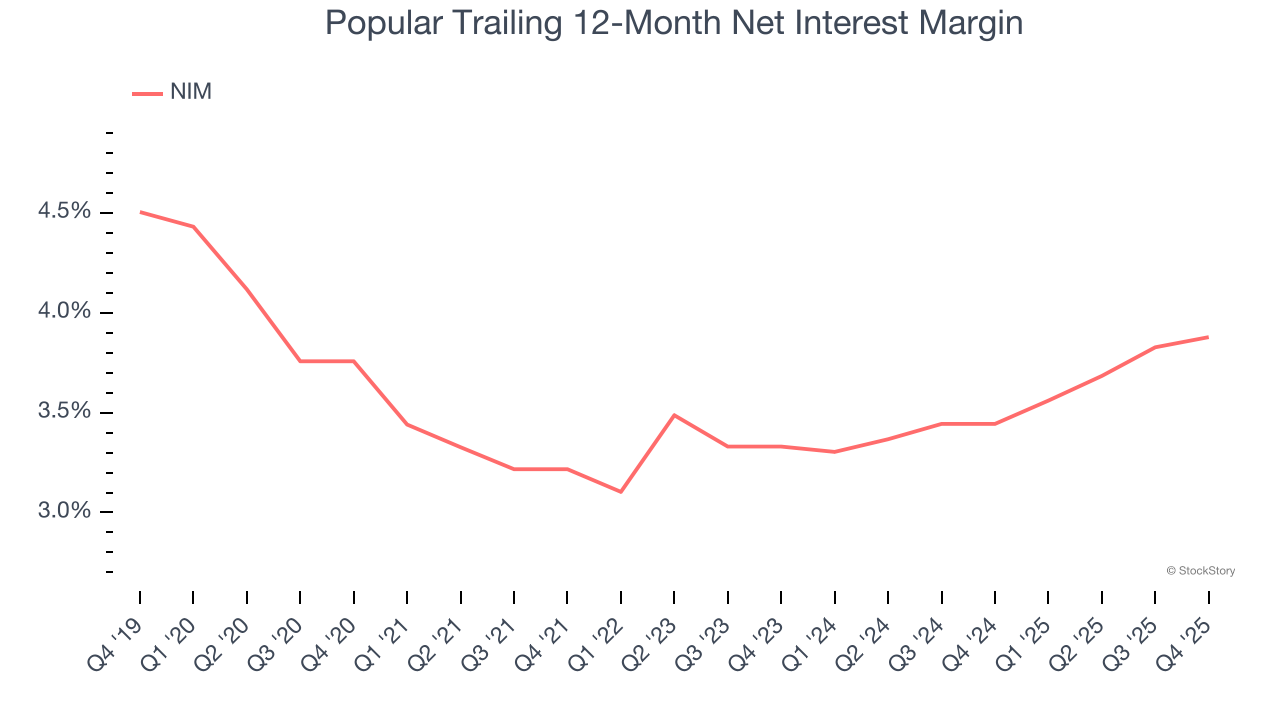

1. Increasing Net Interest Margin Juices Financials

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, Popular’s net interest margin averaged 3.7%, climbing by 54.8 basis points (100 basis points = 1 percentage point) over that period.

This expansion was a tailwind for its net interest income, and while prevailing interest rates matter the most for industry net interest margins, banks that consistently increase this figure generally boast higher-earning loan books (all else equal such as the risk of those loans) or provide differentiated services that give them the ability to charge higher rates (pricing power).

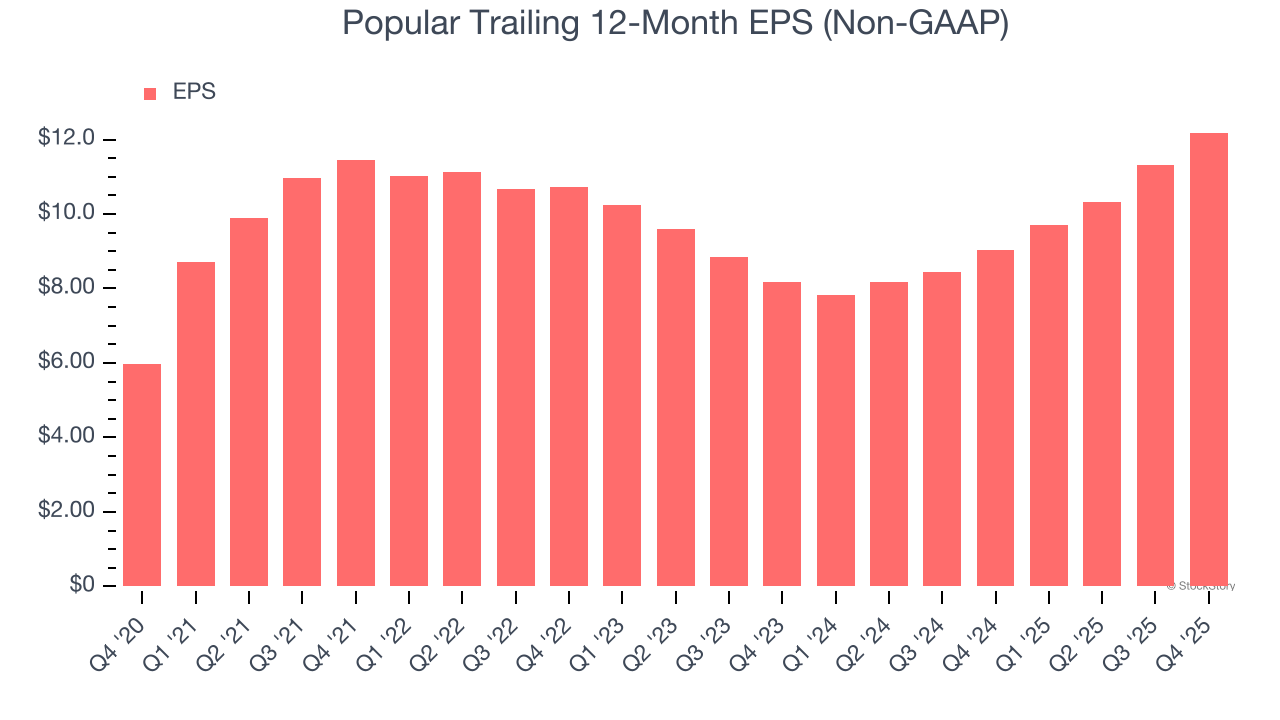

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Popular’s EPS grew at a spectacular 15.4% compounded annual growth rate over the last five years, higher than its 8.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

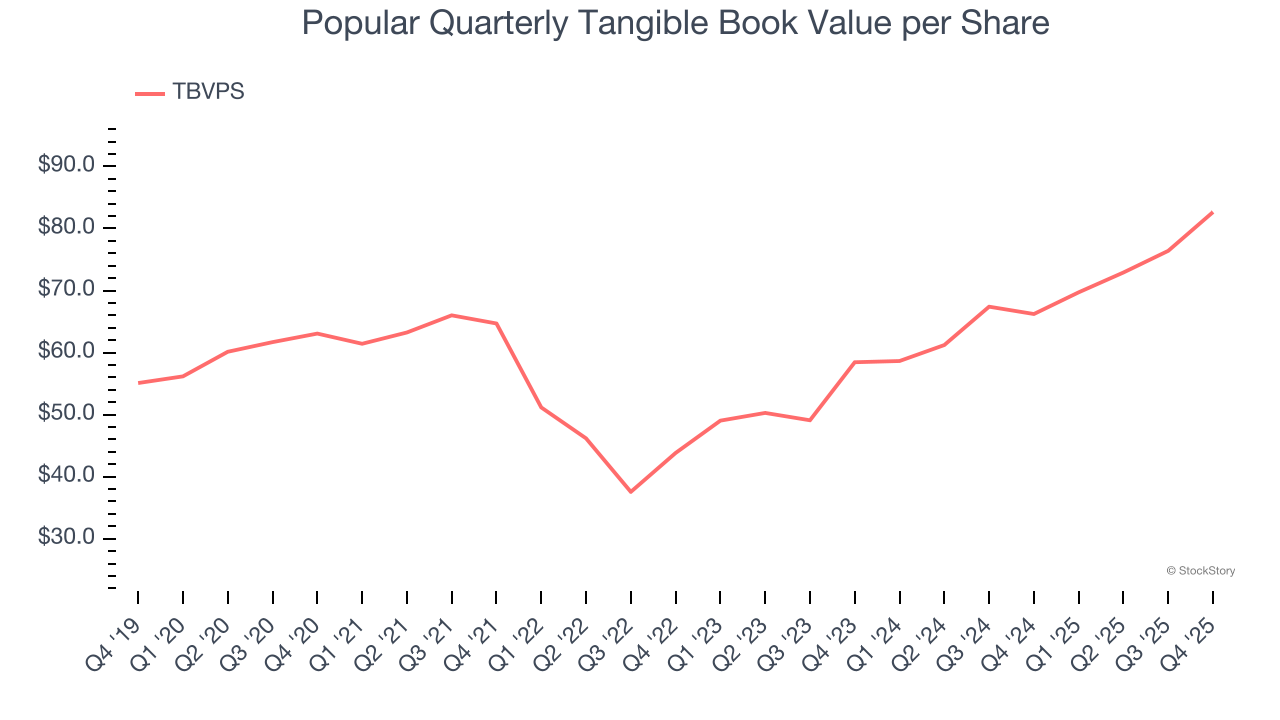

3. Growing TBVPS Reflects Strong Asset Base

For banks, tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Popular’s TBVPS increased by 5.6% annually over the last five years, and growth has recently accelerated as TBVPS grew at an exceptional 18.9% annual clip over the past two years (from $58.45 to $82.65 per share).

Final Judgment

These are just a few reasons why Popular ranks highly on our list, and with its shares beating the market recently, the stock trades at 1.3× forward P/B (or $146.02 per share). Is now the time to initiate a position? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than Popular

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.