IT solutions provider Connection (NASDAQ:CNXN) will be reporting earnings this Wednesday after the bell. Here’s what to look for.

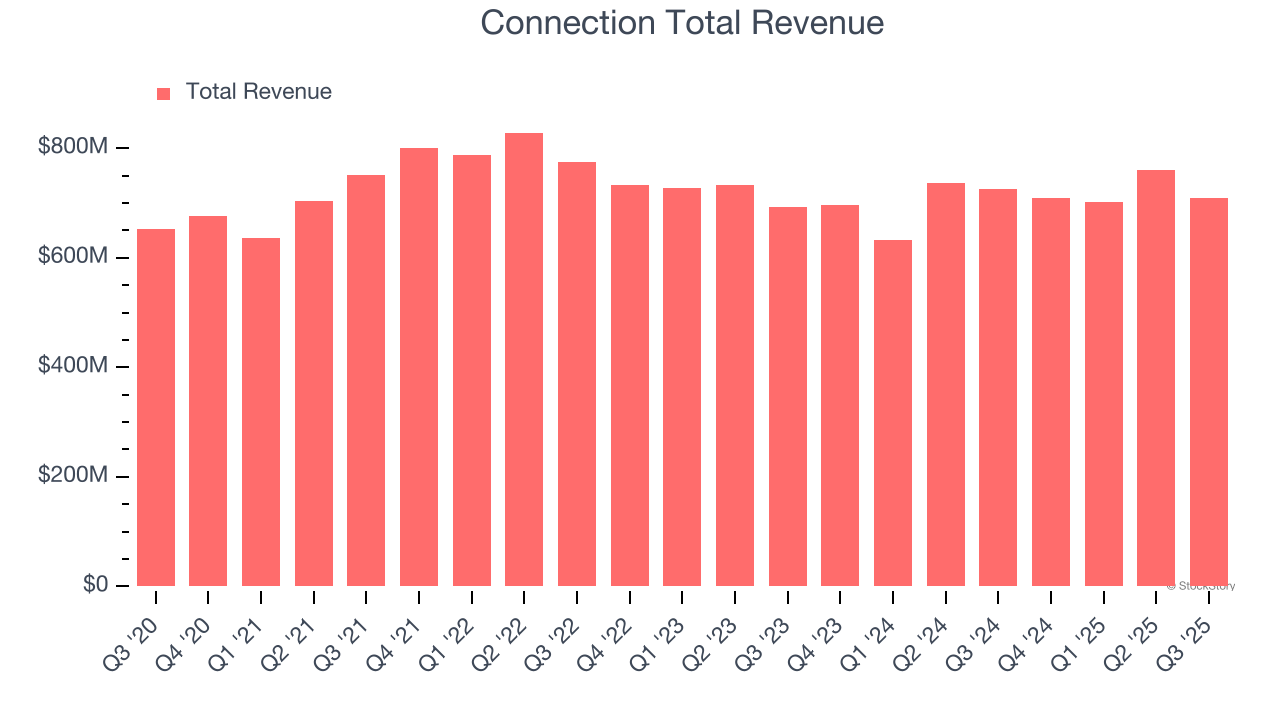

Connection missed analysts’ revenue expectations by 4.7% last quarter, reporting revenues of $709.1 million, down 2.2% year on year. It was a disappointing quarter for the company, with a significant miss of analysts’ revenue estimates and a significant miss of analysts’ EPS estimates.

Is Connection a buy or sell going into earnings? Read our full analysis here, it’s free for active Edge members.

This quarter, analysts are expecting Connection’s revenue to grow 3.8% year on year to $735.5 million, improving from the 1.8% increase it recorded in the same quarter last year. Adjusted earnings are expected to come in at $0.86 per share.

Analysts covering the company have generally reconfirmed their estimates over the last 30 days, suggesting they anticipate the business to stay the course heading into earnings. Connection has missed Wall Street’s revenue estimates five times over the last two years.

Looking at Connection’s peers in the tech hardware & electronics segment, some have already reported their Q4 results, giving us a hint as to what we can expect. Avnet delivered year-on-year revenue growth of 11.6%, beating analysts’ expectations by 4.5%, and TD SYNNEX reported revenues up 9.7%, topping estimates by 2.6%. Avnet traded up 19.1% following the results while TD SYNNEX’s stock price was unchanged.

Read our full analysis of Avnet’s results here and TD SYNNEX’s results here.

Investors in the tech hardware & electronics segment have had steady hands going into earnings, with share prices up 1.6% on average over the last month. Connection is up 4.1% during the same time and is heading into earnings with an average analyst price target of $76 (compared to the current share price of $60.11).

P.S. STOP buying the AI stocks everyone's talking about. The real money? It’s in the profitable pick nobody’s watching yet. We’ve identified an AI profit machine that’s flying under Wall Street’s radar—for now. We can’t keep this research public forever—grab your FREE copy before we pull it offline. GO HERE NOW.