The past six months have been a windfall for Encore Capital Group’s shareholders. The company’s stock price has jumped 46.2%, hitting $57.99 per share. This was partly due to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is there a buying opportunity in Encore Capital Group, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is Encore Capital Group Not Exciting?

Despite the momentum, we're cautious about Encore Capital Group. Here are three reasons we avoid ECPG and a stock we'd rather own.

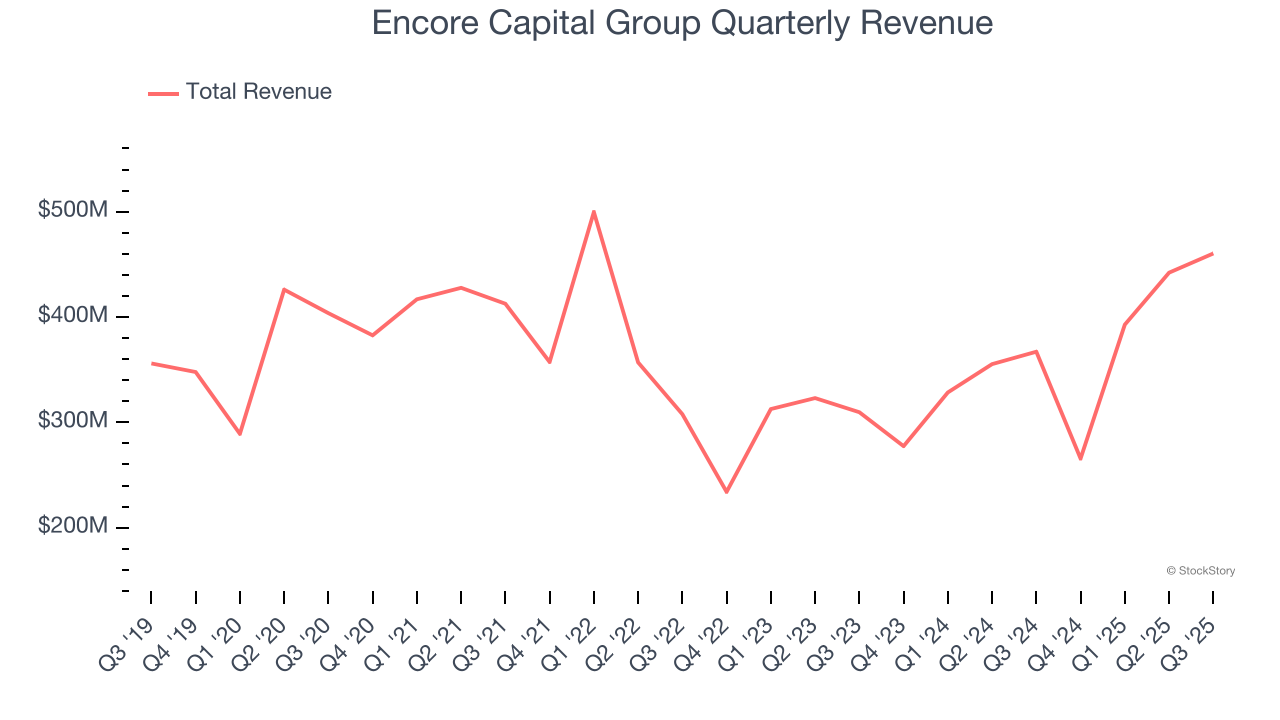

1. Long-Term Revenue Growth Disappoints

Examining a company’s long-term performance can provide clues about its quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years.

Over the last five years, Encore Capital Group grew its revenue at a weak 1.3% compounded annual growth rate. This was below our standards.

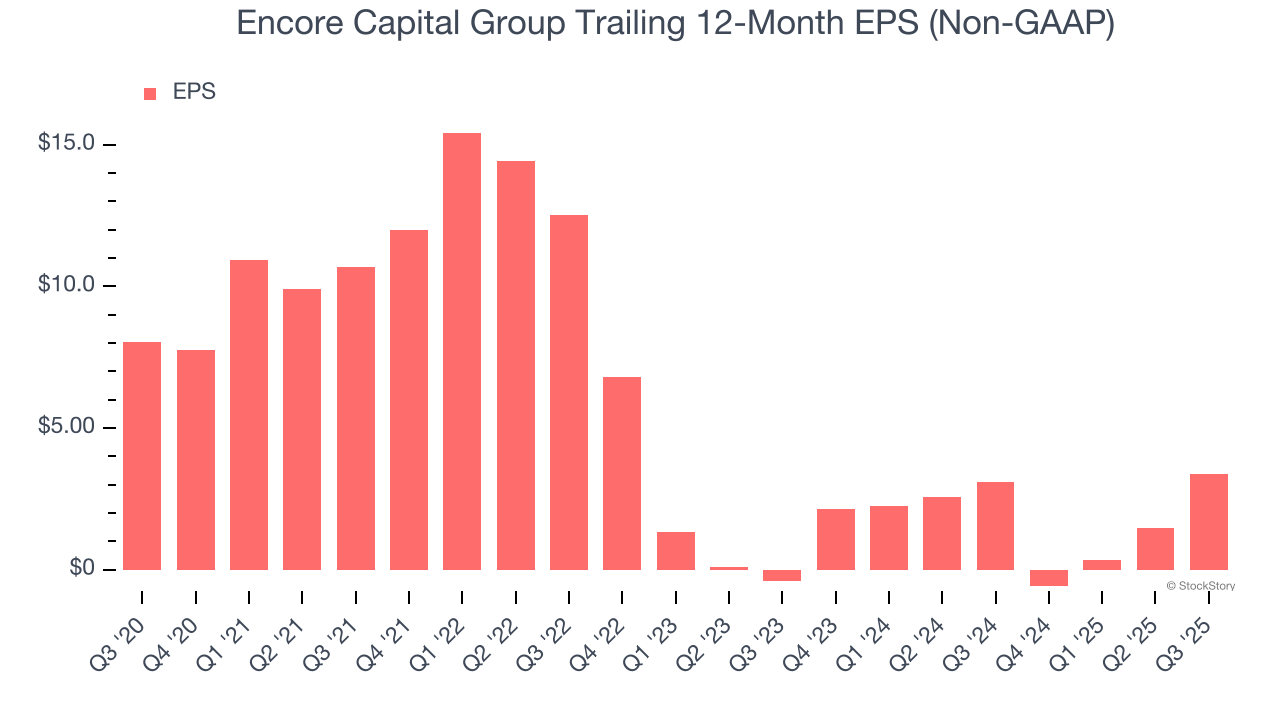

2. EPS Trending Down

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Encore Capital Group, its EPS declined by 15.9% annually over the last five years while its revenue grew by 1.3%. This tells us the company became less profitable on a per-share basis as it expanded.

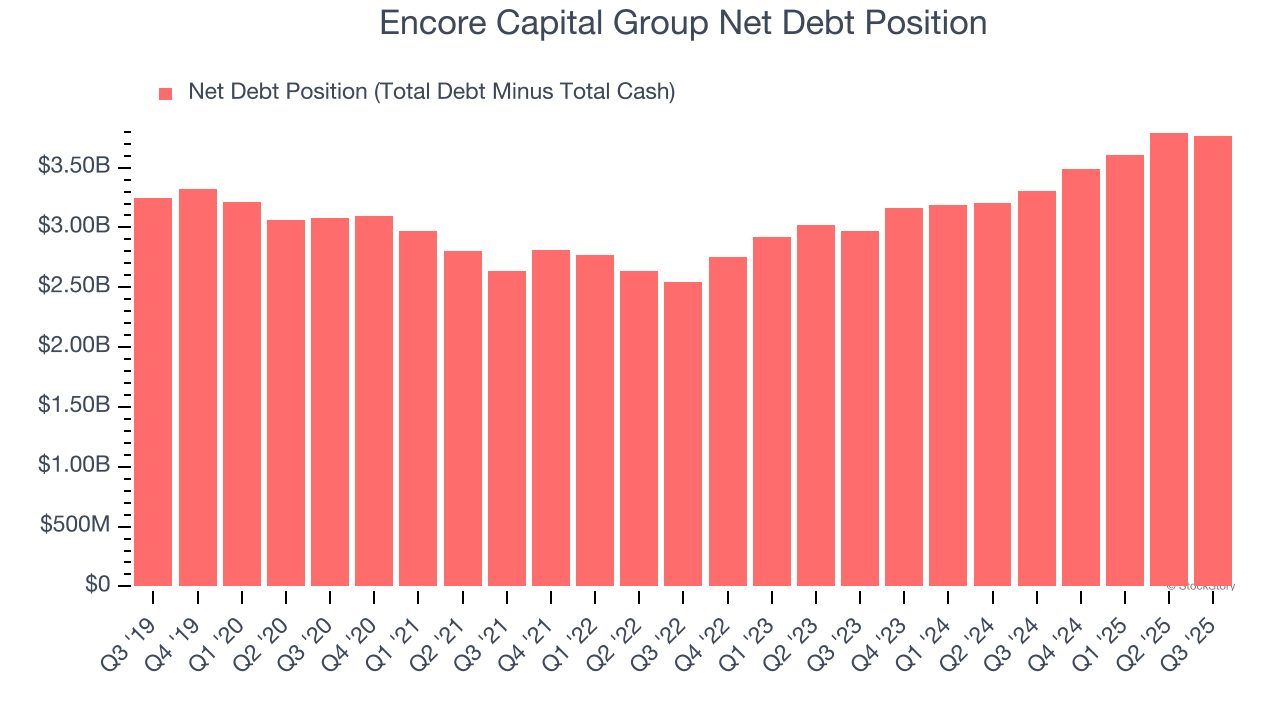

3. High Debt Levels Increase Risk

Encore Capital Group reported $172.5 million of cash and $3.93 billion of debt on its balance sheet in the most recent quarter.

As investors in high-quality companies, we primarily focus on whether a company’s profits can support its debt.

With $349.9 million of EBITDA over the last 12 months, we view Encore Capital Group’s 10.8× net-debt-to-EBITDA ratio as inadequate. The company’s lacking profits relative to its borrowings give it little breathing room, raising red flags.

Final Judgment

Encore Capital Group isn’t a terrible business, but it doesn’t pass our quality test. Following the recent surge, the stock trades at 7.9× forward P/E (or $57.99 per share). While this valuation is optically cheap, the potential downside is big given its shaky fundamentals. We're pretty confident there are superior stocks to buy right now. We’d recommend looking at a top digital advertising platform riding the creator economy.

Stocks We Like More Than Encore Capital Group

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.