Over the last six months, MGP Ingredients’s shares have sunk to $25.87, producing a disappointing 6.6% loss - a stark contrast to the S&P 500’s 8.4% gain. This may have investors wondering how to approach the situation.

Is there a buying opportunity in MGP Ingredients, or does it present a risk to your portfolio? Check out our in-depth research report to see what our analysts have to say, it’s free.

Why Do We Think MGP Ingredients Will Underperform?

Despite the more favorable entry price, we're sitting this one out for now. Here are three reasons we avoid MGPI and a stock we'd rather own.

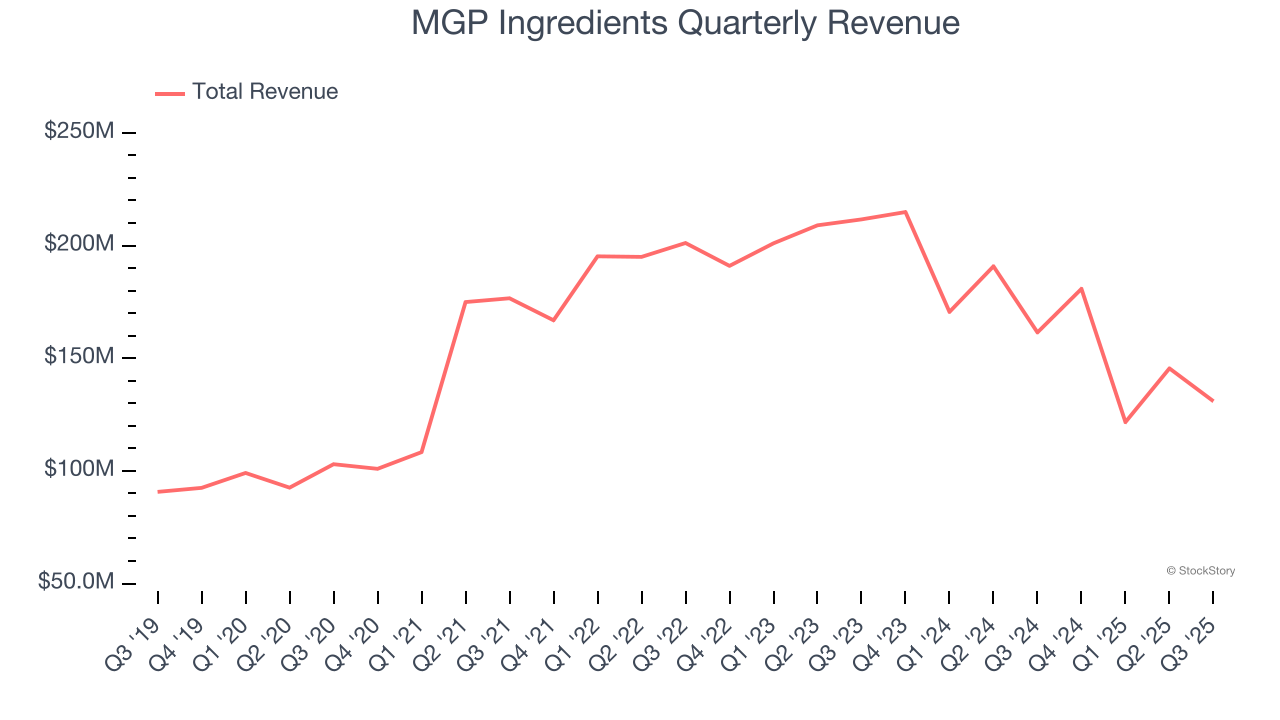

1. Revenue Spiraling Downwards

Reviewing a company’s long-term sales performance reveals insights into its quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Over the last three years, MGP Ingredients’s demand was weak and its revenue declined by 8.6% per year. This wasn’t a great result and signals it’s a low quality business.

2. Revenue Projections Show Stormy Skies Ahead

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect MGP Ingredients’s revenue to drop by 11.3%, a decrease from This projection doesn't excite us and indicates its products will face some demand challenges.

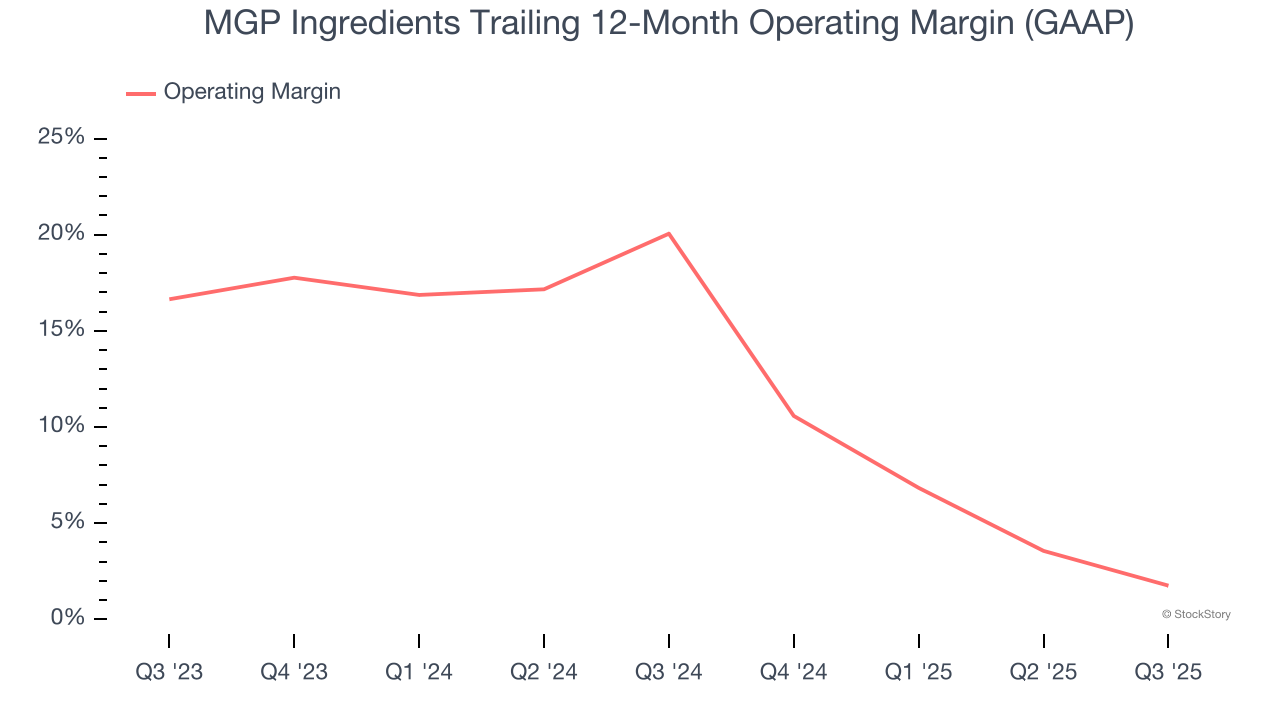

3. Shrinking Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

Analyzing the trend in its profitability, MGP Ingredients’s operating margin decreased by 18.3 percentage points over the last year. Even though its historical margin was healthy, shareholders will want to see MGP Ingredients become more profitable in the future. Its operating margin for the trailing 12 months was 1.8%.

Final Judgment

We see the value of companies helping consumers, but in the case of MGP Ingredients, we’re out. Following the recent decline, the stock trades at 11.5× forward P/E (or $25.87 per share). While this valuation is reasonable, we don’t see a big opportunity at the moment. There are superior stocks to buy right now. We’d recommend looking at a dominant Aerospace business that has perfected its M&A strategy.

High-Quality Stocks for All Market Conditions

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.