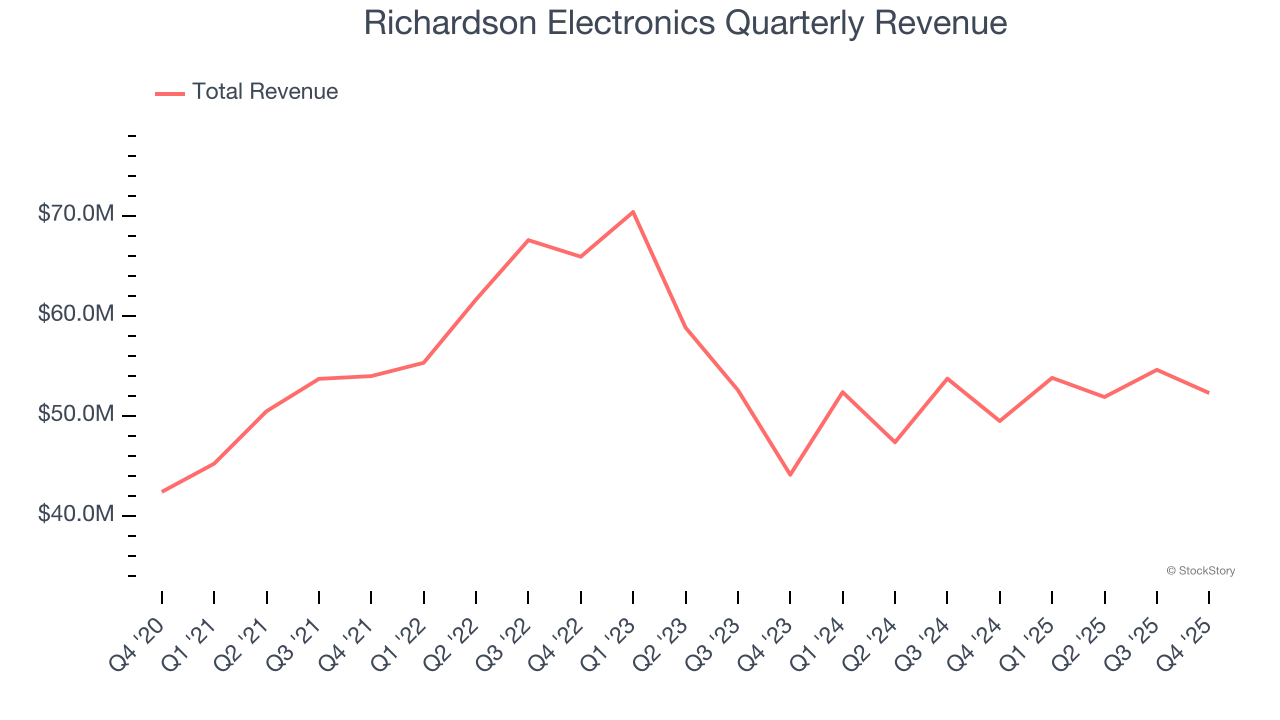

Electronics distributor Richardson Electronics (NASDAQ:RELL) reported Q4 CY2025 results topping the market’s revenue expectations, with sales up 5.7% year on year to $52.29 million. Its GAAP loss of $0.01 per share was in line with analysts’ consensus estimates.

Is now the time to buy Richardson Electronics? Find out by accessing our full research report, it’s free for active Edge members.

Richardson Electronics (RELL) Q4 CY2025 Highlights:

- Revenue: $52.29 million vs analyst estimates of $49.9 million (5.7% year-on-year growth, 4.8% beat)

- EPS (GAAP): -$0.01 vs analyst estimates of -$0.01 (in line)

- Adjusted EBITDA: $741,000 vs analyst estimates of $720,000 (1.4% margin, relatively in line)

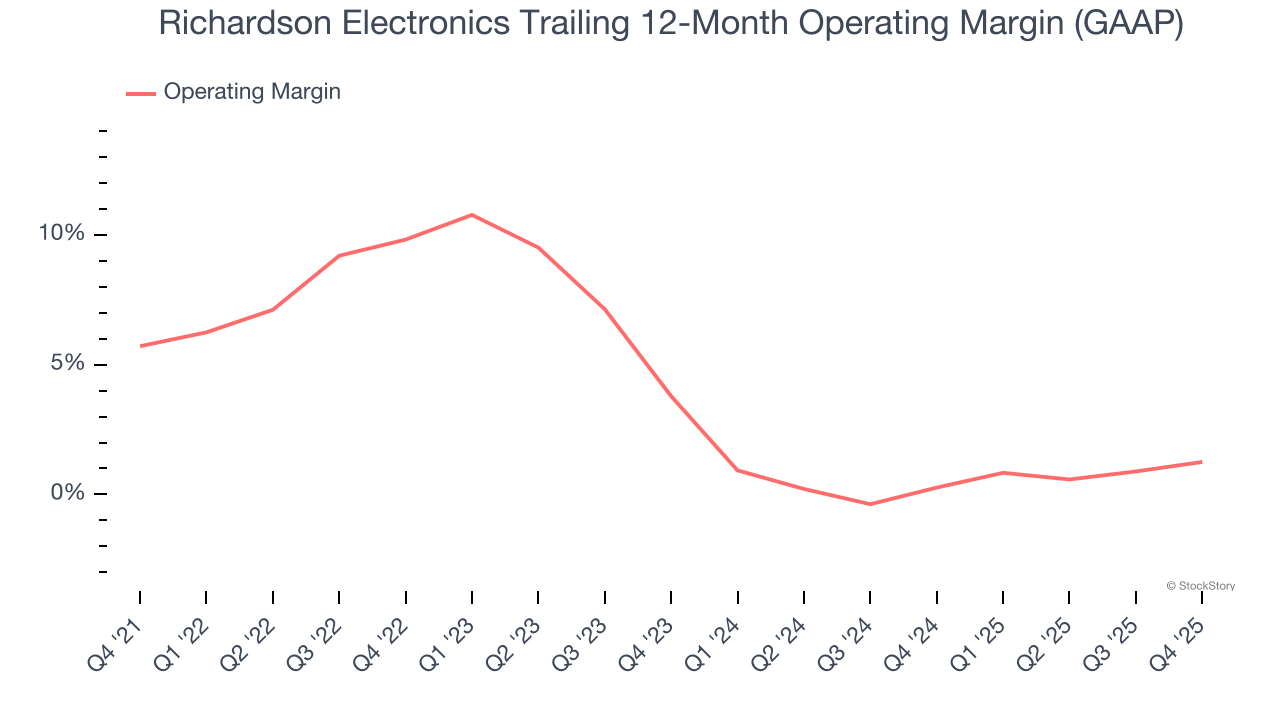

- Operating Margin: 0.3%, up from -1.4% in the same quarter last year

- Free Cash Flow was -$1.71 million, down from $4.95 million in the same quarter last year

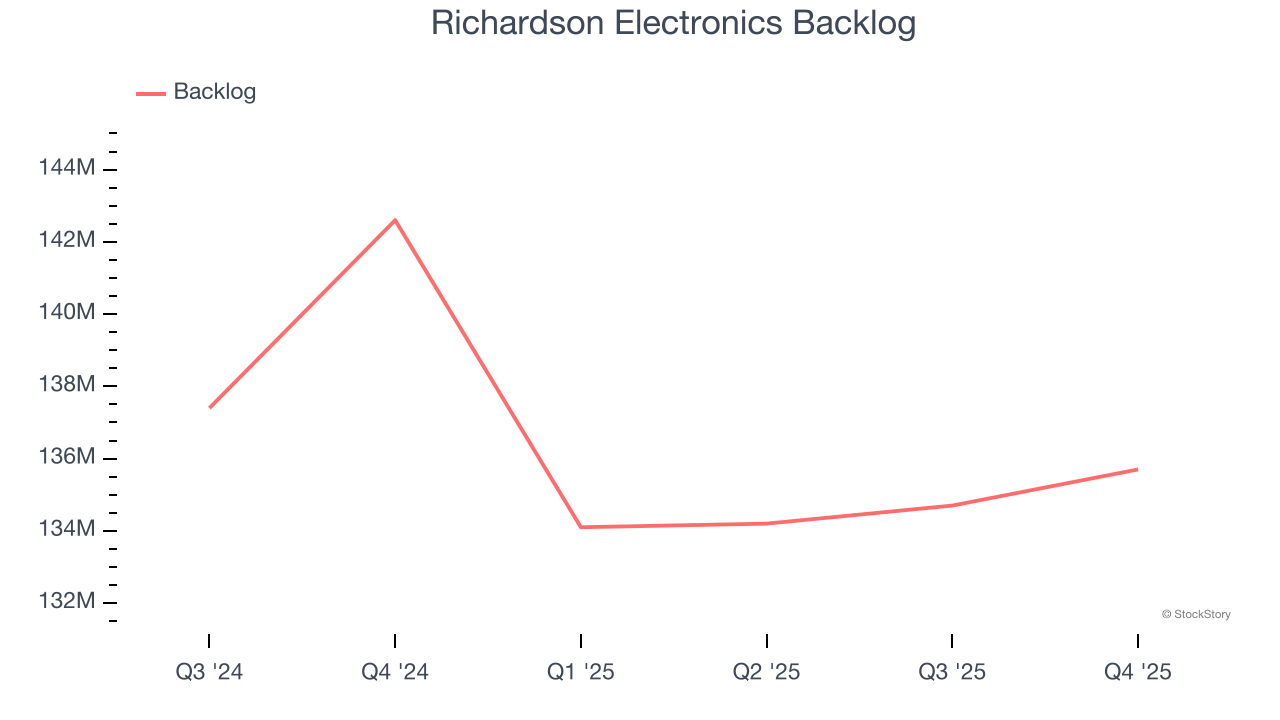

- Backlog: $135.7 million at quarter end, down 4.8% year on year

- Market Capitalization: $167.2 million

“We delivered solid second-quarter fiscal 2026 revenue growth of 5.7%, led by strong year-over-year performance in our Green Energy Solutions (GES) business,” said Edward J. Richardson, Chairman, CEO, and President.

Company Overview

Founded in 1947, Richardson Electronics (NASDAQ:RELL) is a distributor of power grid and microwave tubes as well as consumables related to those products.

Revenue Growth

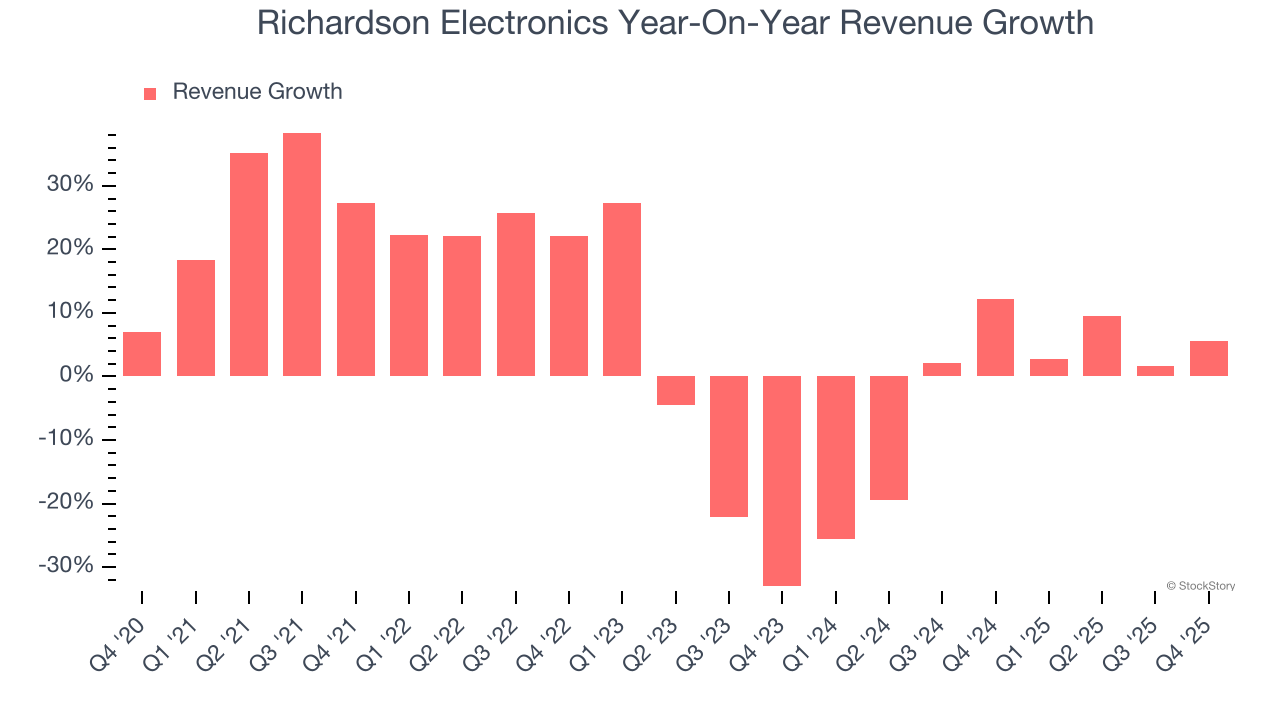

Examining a company’s long-term performance can provide clues about its quality. Any business can experience short-term success, but top-performing ones enjoy sustained growth for years. Over the last five years, Richardson Electronics grew its sales at a mediocre 6.3% compounded annual growth rate. This fell short of our benchmark for the industrials sector and is a tough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Richardson Electronics’s performance shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 3% annually.

We can better understand the company’s revenue dynamics by analyzing its backlog, or the value of its outstanding orders that have not yet been executed or delivered. Richardson Electronics’s backlog reached $135.7 million in the latest quarter and averaged 3.4% year-on-year declines over the last two years. Because this number is in line with its revenue growth, we can see the company effectively balanced its new order intake and fulfillment processes.

This quarter, Richardson Electronics reported year-on-year revenue growth of 5.7%, and its $52.29 million of revenue exceeded Wall Street’s estimates by 4.8%.

Looking ahead, sell-side analysts expect revenue to grow 8.2% over the next 12 months, an improvement versus the last two years. This projection is above average for the sector and implies its newer products and services will fuel better top-line performance.

Software is eating the world and there is virtually no industry left that has been untouched by it. That drives increasing demand for tools helping software developers do their jobs, whether it be monitoring critical cloud infrastructure, integrating audio and video functionality, or ensuring smooth content streaming. Click here to access a free report on our 3 favorite stocks to play this generational megatrend.

Operating Margin

Richardson Electronics was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.4% was weak for an industrials business.

Looking at the trend in its profitability, Richardson Electronics’s operating margin decreased by 4.5 percentage points over the last five years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Richardson Electronics’s performance was poor no matter how you look at it - it shows that costs were rising and it couldn’t pass them onto its customers.

This quarter, Richardson Electronics’s breakeven margin was up 1.6 percentage points year on year. The increase was encouraging, and because its operating margin rose more than its gross margin, we can infer it was more efficient with expenses such as marketing, R&D, and administrative overhead.

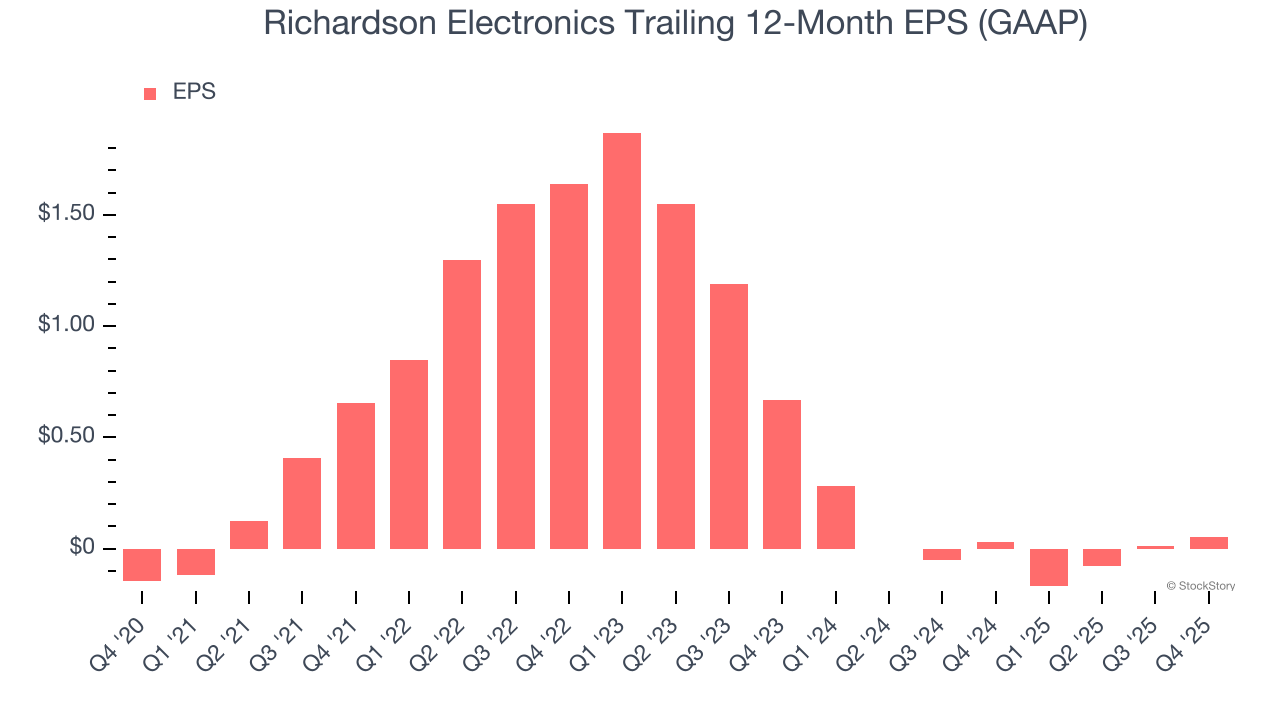

Earnings Per Share

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

Richardson Electronics’s full-year EPS flipped from negative to positive over the last five years. This is encouraging and shows it’s at a critical moment in its life.

Like with revenue, we analyze EPS over a more recent period because it can provide insight into an emerging theme or development for the business.

Sadly for Richardson Electronics, its EPS declined by more than its revenue over the last two years, dropping 72.7%. This tells us the company struggled to adjust to shrinking demand.

In Q4, Richardson Electronics reported EPS of negative $0.01, up from negative $0.05 in the same quarter last year. This print was close to analysts’ estimates. Over the next 12 months, Wall Street expects Richardson Electronics’s full-year EPS of $0.05 to grow 630%.

Key Takeaways from Richardson Electronics’s Q4 Results

We were impressed by how significantly Richardson Electronics blew past analysts’ revenue expectations this quarter. We were also happy its EBITDA outperformed Wall Street’s estimates. Overall, we think this was a decent quarter with some key metrics above expectations. The market seemed to be hoping for more, and the stock traded down 10.5% to $10.45 immediately after reporting.

Is Richardson Electronics an attractive investment opportunity right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.