What a brutal six months it’s been for ThredUp. The stock has dropped 48.6% and now trades at $4.98, rattling many shareholders. This may have investors wondering how to approach the situation.

Is now the time to buy ThredUp, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think ThredUp Will Underperform?

Even with the cheaper entry price, we're cautious about ThredUp. Here are three reasons there are better opportunities than TDUP and a stock we'd rather own.

1. Weak Growth in Orders Points to Soft Demand

Revenue growth can be broken down into changes in price and volume (for companies like ThredUp, our preferred volume metric is orders). While both are important, the latter is the most critical to analyze because prices have a ceiling.

ThredUp’s orders came in at 1.61 million in the latest quarter, and over the last two years, averaged 6.4% year-on-year growth. This performance was underwhelming and suggests it might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

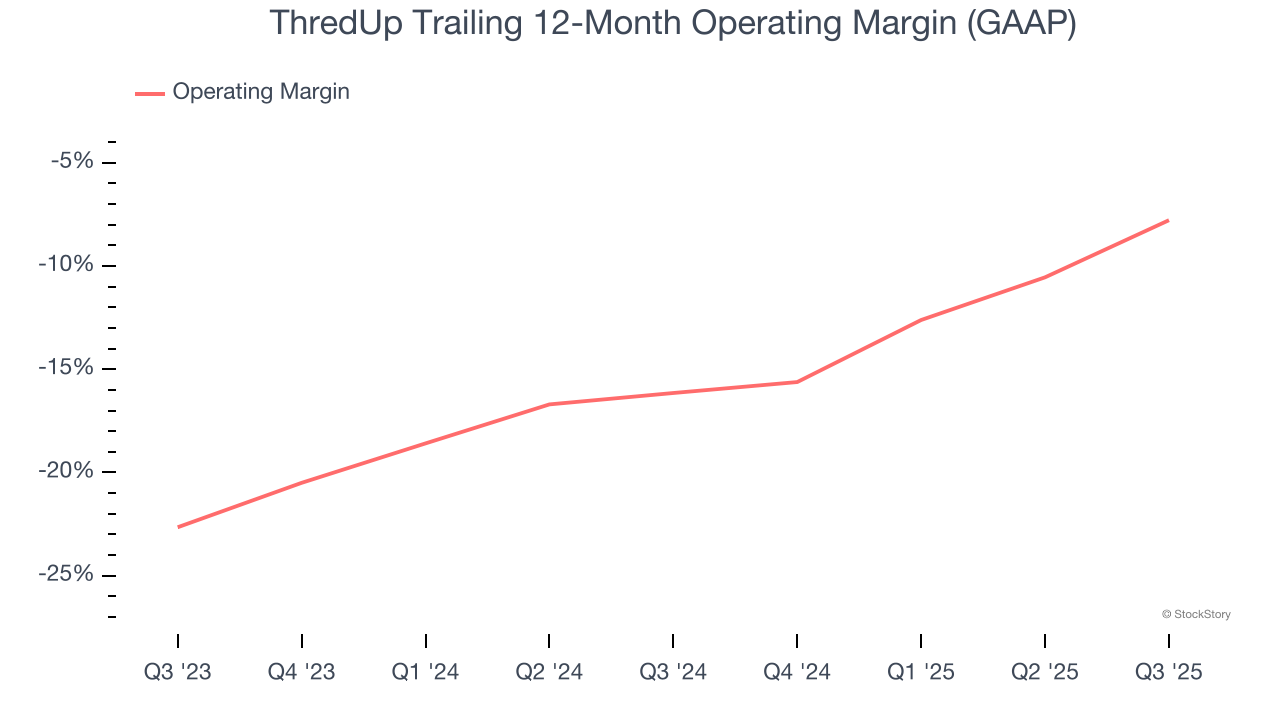

2. Operating Losses Sound the Alarms

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses – everything from the cost of goods sold to advertising and wages. It’s also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

ThredUp’s operating margin has risen over the last 12 months, but it still averaged negative 11.6% over the last two years. This is due to its large expense base and inefficient cost structure.

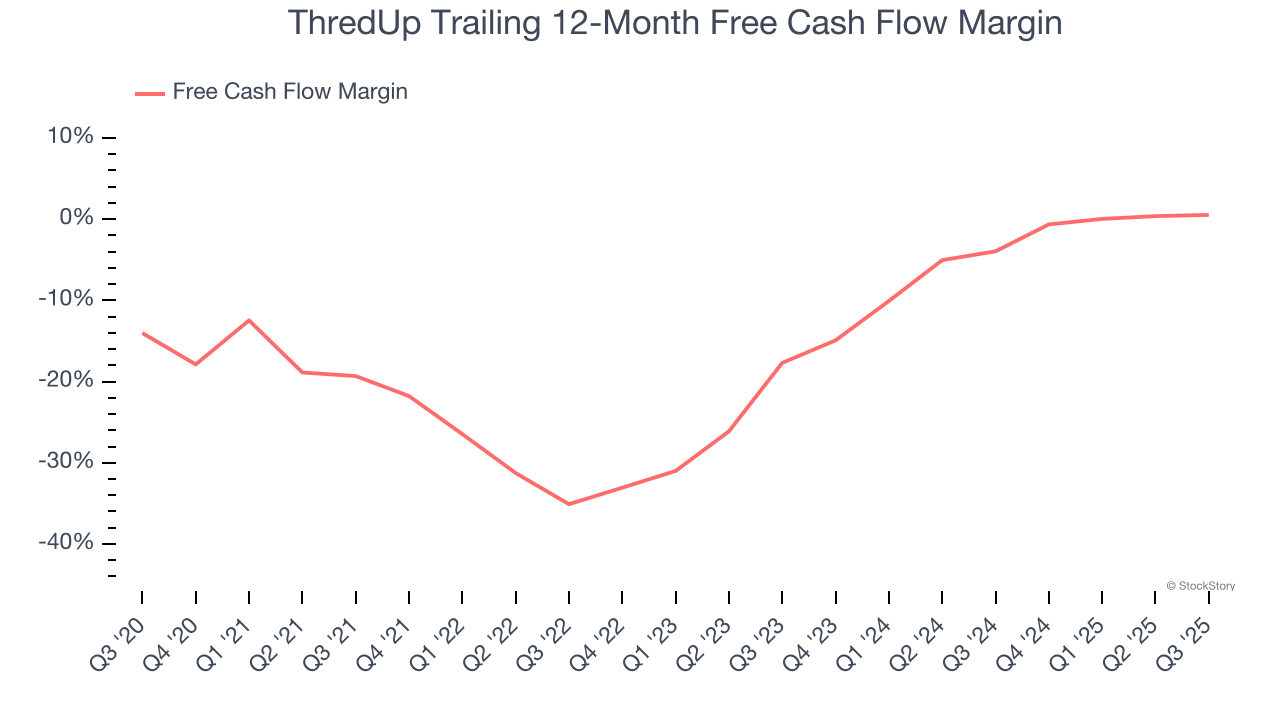

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

While ThredUp posted positive free cash flow this quarter, the broader story hasn’t been so clean. Over the last two years, ThredUp’s demanding reinvestments to stay relevant have drained its resources, putting it in a pinch and limiting its ability to return capital to investors. Its free cash flow margin averaged negative 1.5%, meaning it lit $1.54 of cash on fire for every $100 in revenue.

Final Judgment

We cheer for all companies serving everyday consumers, but in the case of ThredUp, we’ll be cheering from the sidelines. After the recent drawdown, the stock trades at 38.4× forward EV-to-EBITDA (or $4.98 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d suggest looking at one of our top software and edge computing picks.

Stocks We Like More Than ThredUp

While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.