What a time it’s been for Tesla. In the past six months alone, the company’s stock price has increased by a massive 48%, reaching $434.94 per share. This was partly thanks to its solid quarterly results, and the run-up might have investors contemplating their next move.

Is now the time to buy Tesla, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free for active Edge members.

Why Do We Think Tesla Will Underperform?

Despite the momentum, we're swiping left on Tesla for now. Here are three reasons you should be careful with TSLA and a stock we'd rather own.

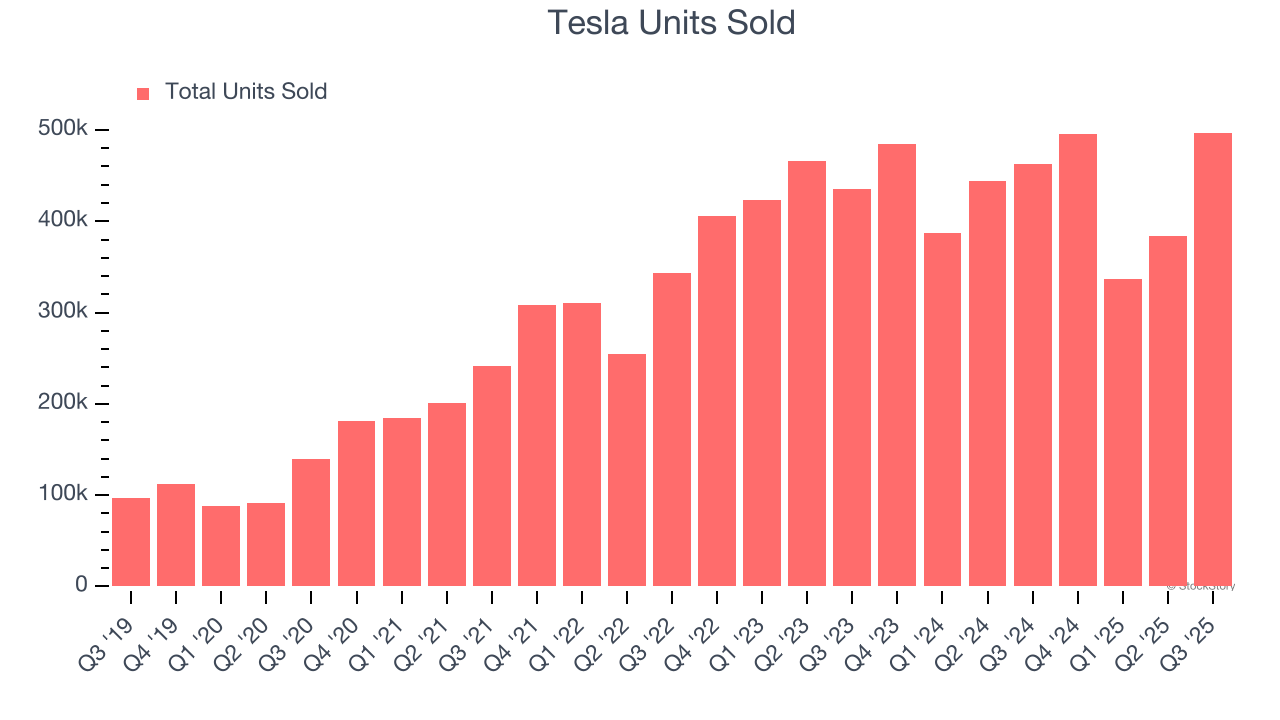

1. Sales Volumes Stall, Demand Waning

Revenue growth can be broken down into changes in price and volume (the number of units sold). While both are important, volume is the lifeblood of a successful Automobile Manufacturing company because there’s a ceiling to what customers will pay.

Over the last two years, Tesla failed to grow its units sold, which came in at 497,099 in the latest quarter. This performance was underwhelming and implies there may be increasing competition or market saturation. It also suggests Tesla might have to lower prices or invest in product improvements to accelerate growth, factors that can hinder near-term profitability.

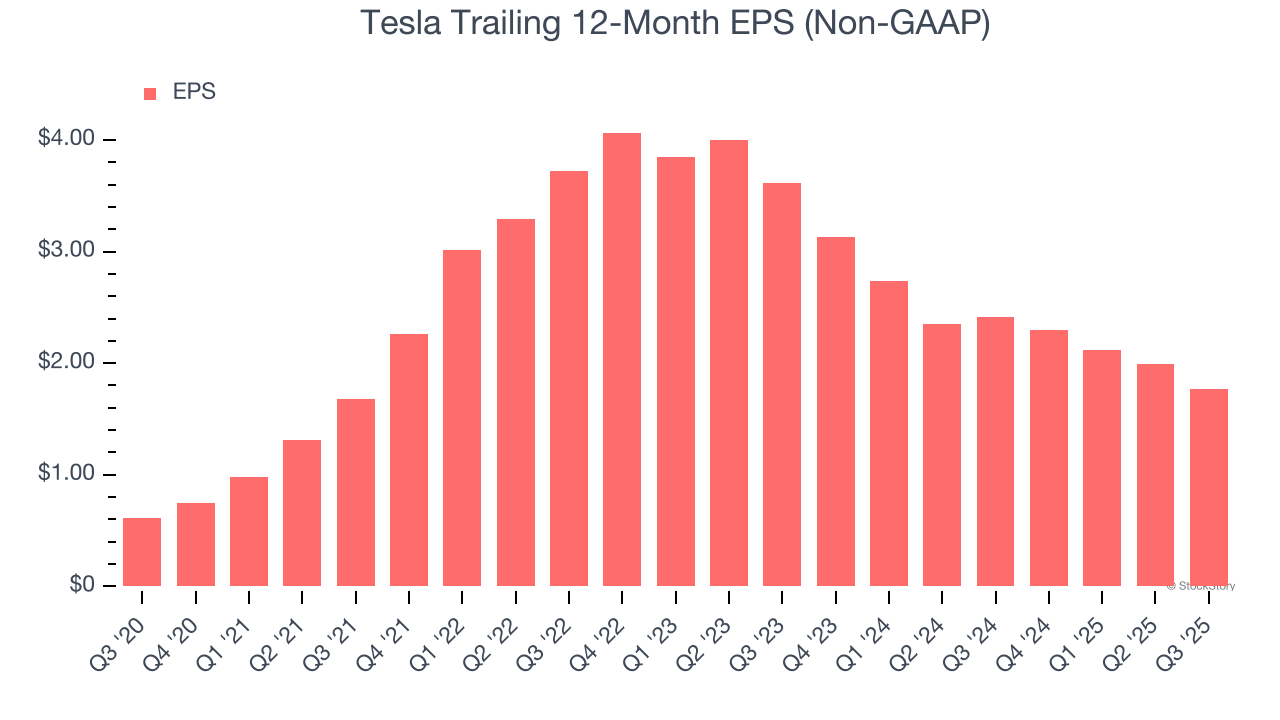

2. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for Tesla, its EPS declined by 30% annually over the last two years while its revenue was flat. This tells us the company struggled to adjust to choppy demand.

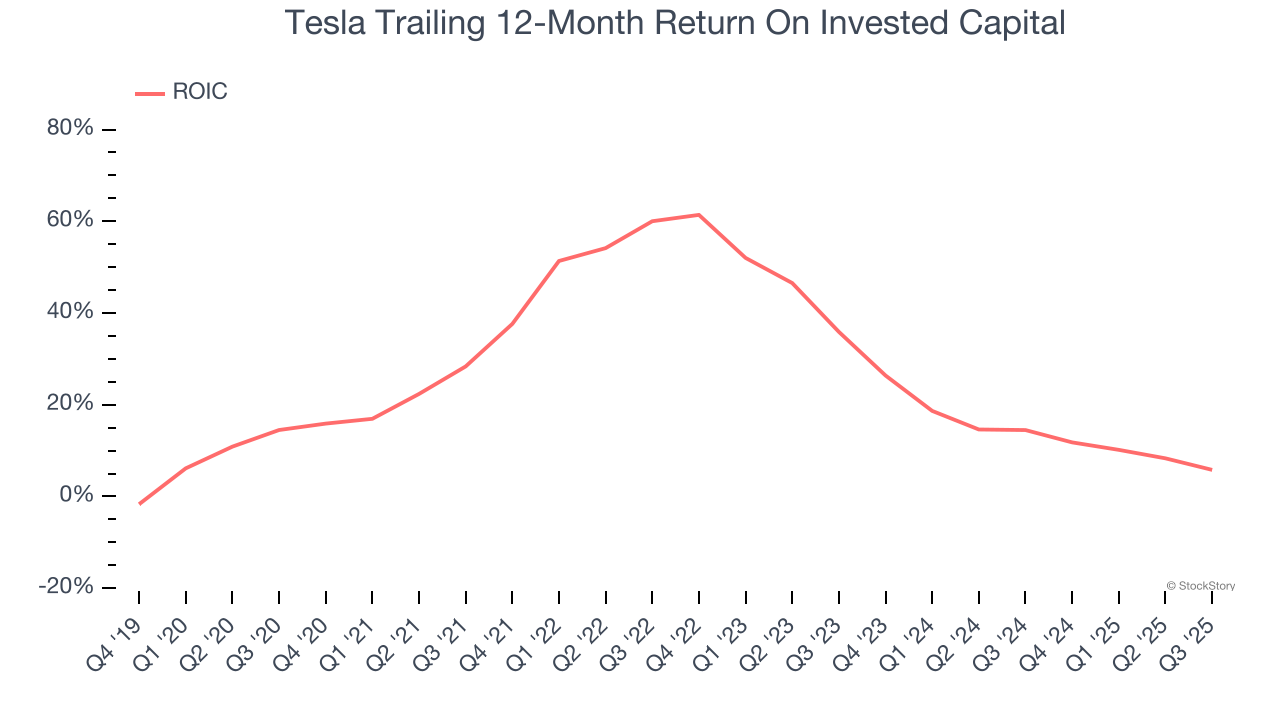

3. New Investments Fail to Bear Fruit as ROIC Declines

A company’s ROIC, or return on invested capital, shows how much operating profit it makes compared to the money it has raised (debt and equity).

We like to invest in businesses with high returns, but the trend in a company’s ROIC is what often surprises the market and moves the stock price. While Tesla’s ROIC fell recently due to its price cuts, the broader trend is still healthy as its ROIC is higher than a few years ago. This is because it’s investing aggressively to capture the AI opportunity. Only time will tell if these investments bear fruit in higher long-term ROICs.

Final Judgment

Tesla falls short of our quality standards. After the recent surge, the stock trades at 225.4× forward price-to-earnings (or $434.94 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better opportunities elsewhere. Let us point you toward one of Charlie Munger’s all-time favorite businesses.

Stocks We Like More Than Tesla

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.