Over the past six months, Texas Instruments has been a great trade, beating the S&P 500 by 9.4%. Its stock price has climbed to $226.03, representing a healthy 17.1% increase. This run-up might have investors contemplating their next move.

Is now the time to buy Texas Instruments, or should you be careful about including it in your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is Texas Instruments Not Exciting?

We’re happy investors have made money, but we're swiping left on Texas Instruments for now. Here are three reasons why TXN doesn't excite us and a stock we'd rather own.

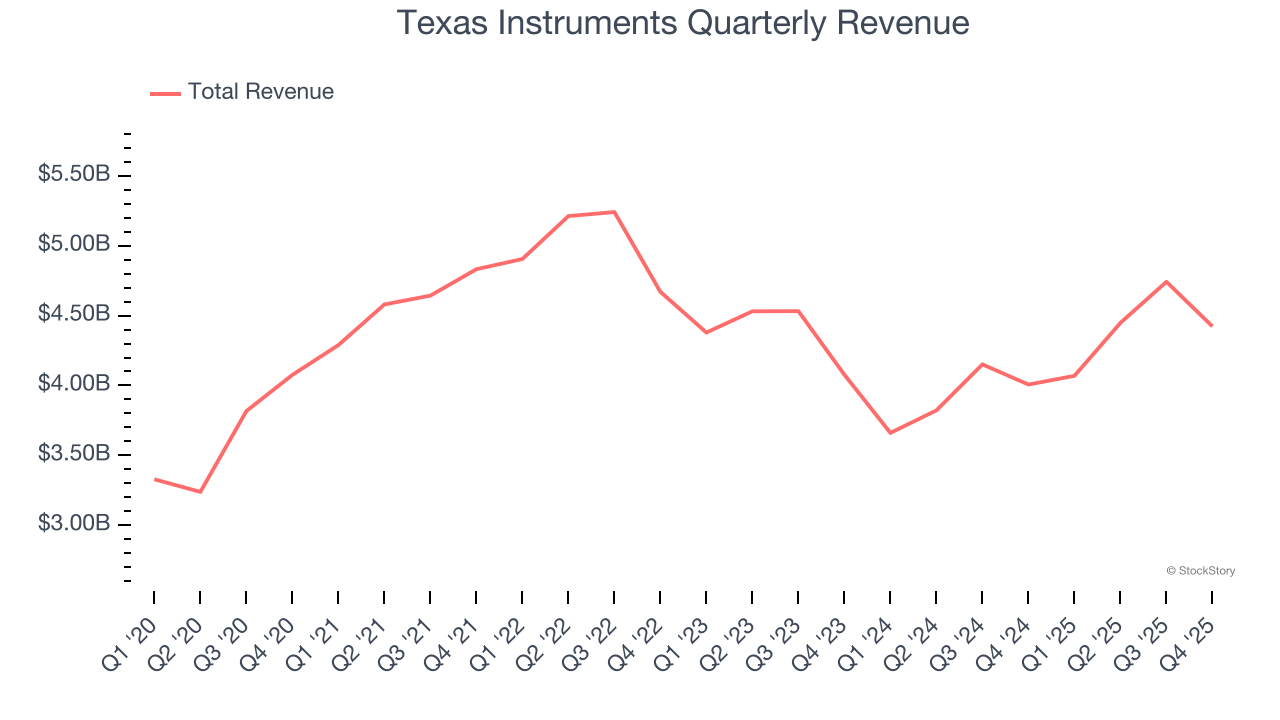

1. Long-Term Revenue Growth Disappoints

A company’s long-term sales performance can indicate its overall quality. Any business can have short-term success, but a top-tier one grows for years. Regrettably, Texas Instruments’s sales grew at a mediocre 4.1% compounded annual growth rate over the last five years. This fell short of our benchmark for the semiconductor sector. Semiconductors are a cyclical industry, and long-term investors should be prepared for periods of high growth followed by periods of revenue contractions.

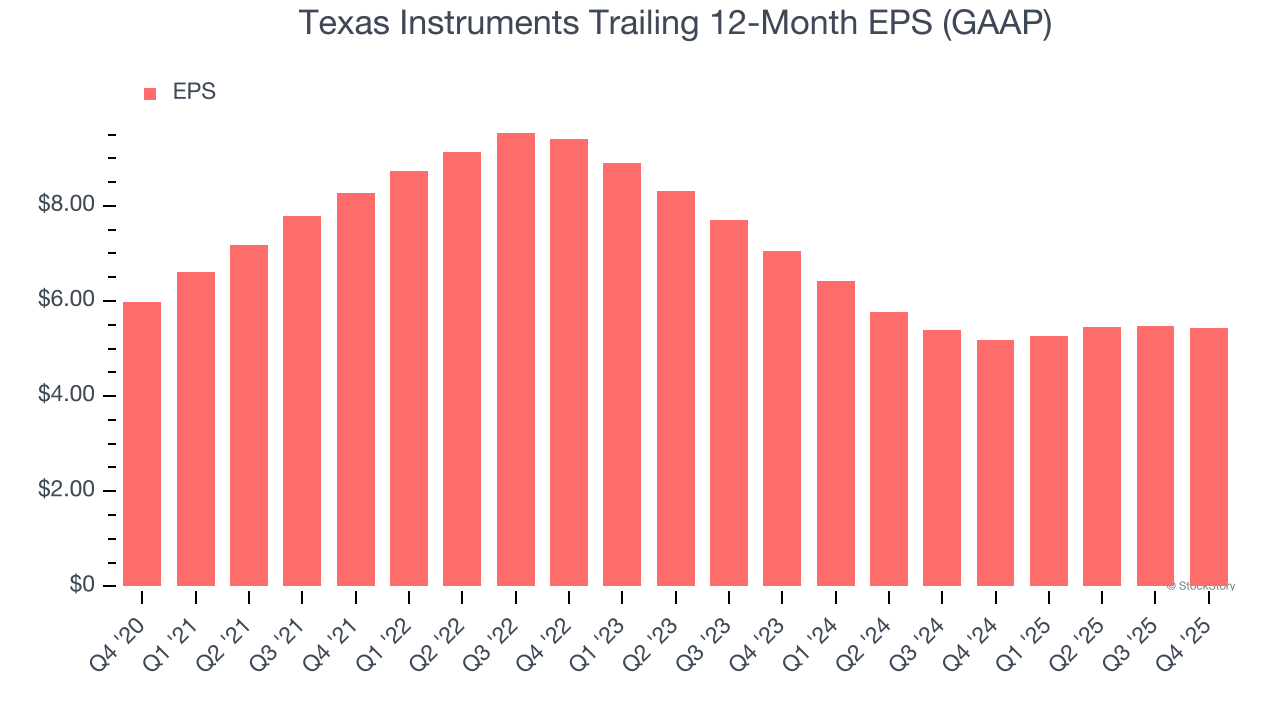

2. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Texas Instruments, its EPS declined by 1.8% annually over the last five years while its revenue grew by 4.1%. This tells us the company became less profitable on a per-share basis as it expanded.

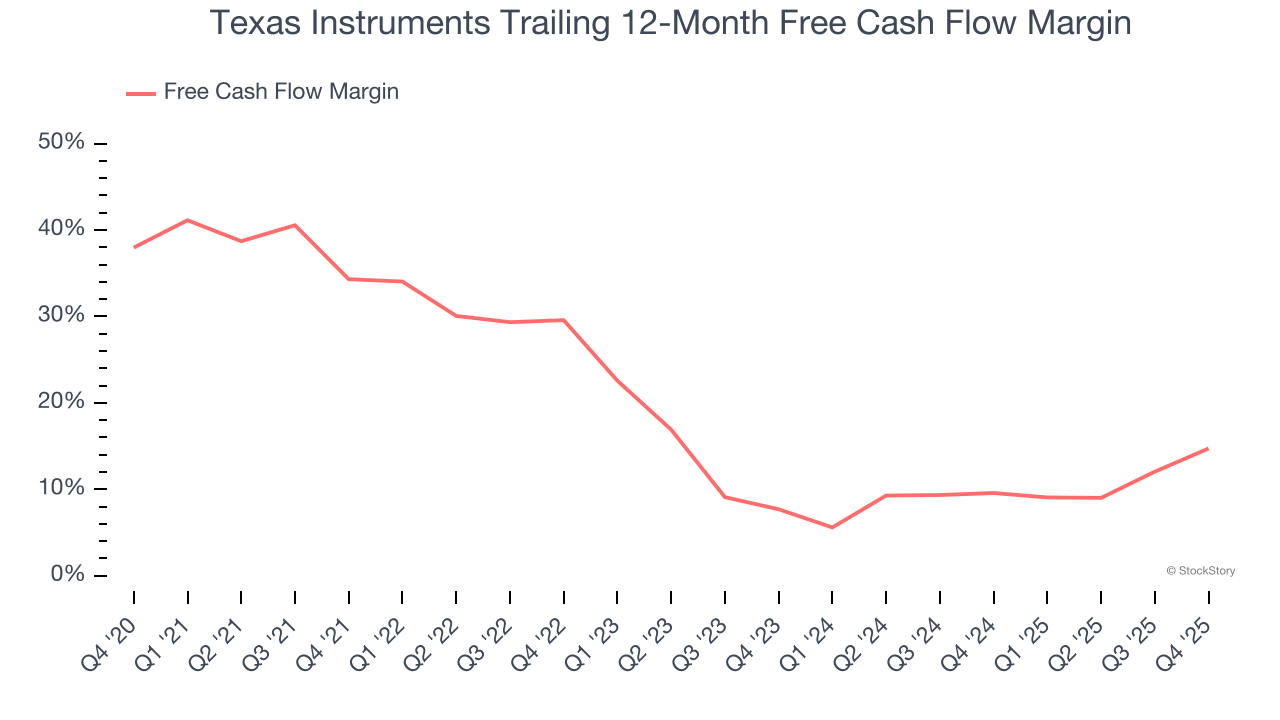

3. Free Cash Flow Margin Dropping

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, Texas Instruments’s margin dropped by 19.6 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. Almost any movement in the wrong direction is undesirable because of its relatively low cash conversion. If the longer-term trend returns, it could signal it’s becoming a more capital-intensive business. Texas Instruments’s free cash flow margin for the trailing 12 months was 14.7%.

Final Judgment

Texas Instruments isn’t a terrible business, but it doesn’t pass our bar. With its shares outperforming the market lately, the stock trades at 34.5× forward P/E (or $226.03 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of our all-time favorite software stocks.

Stocks We Would Buy Instead of Texas Instruments

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.