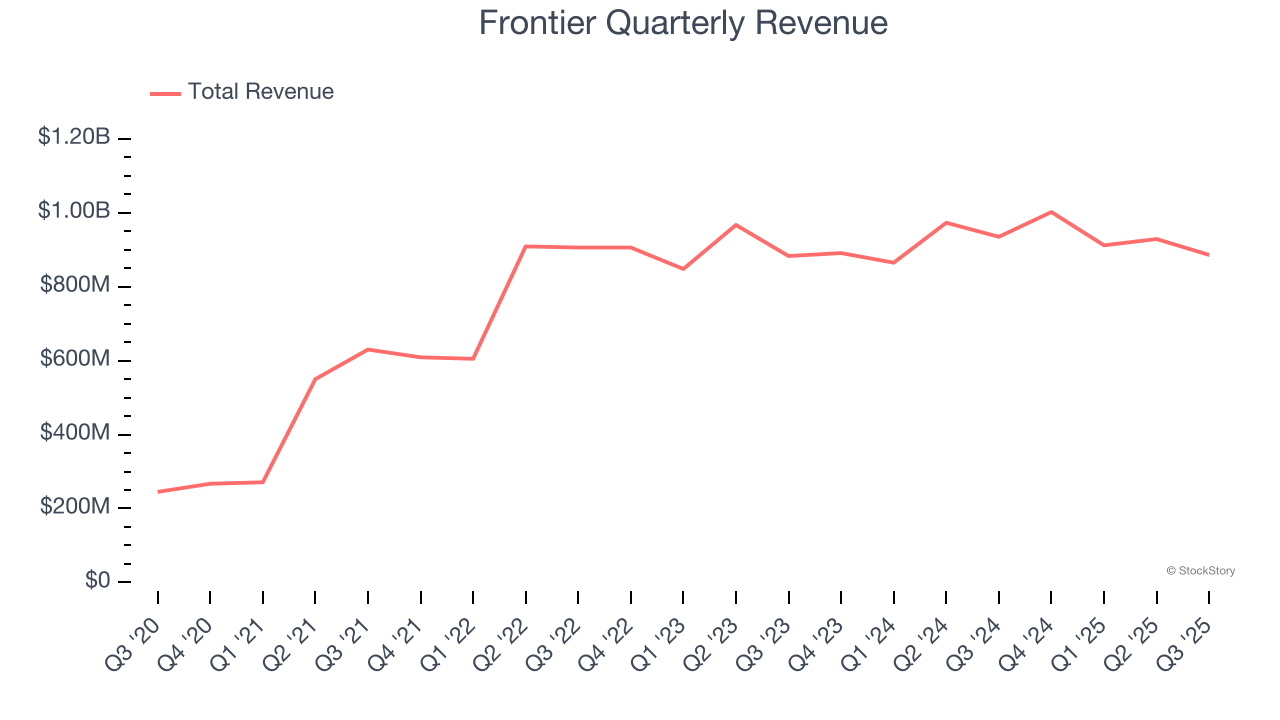

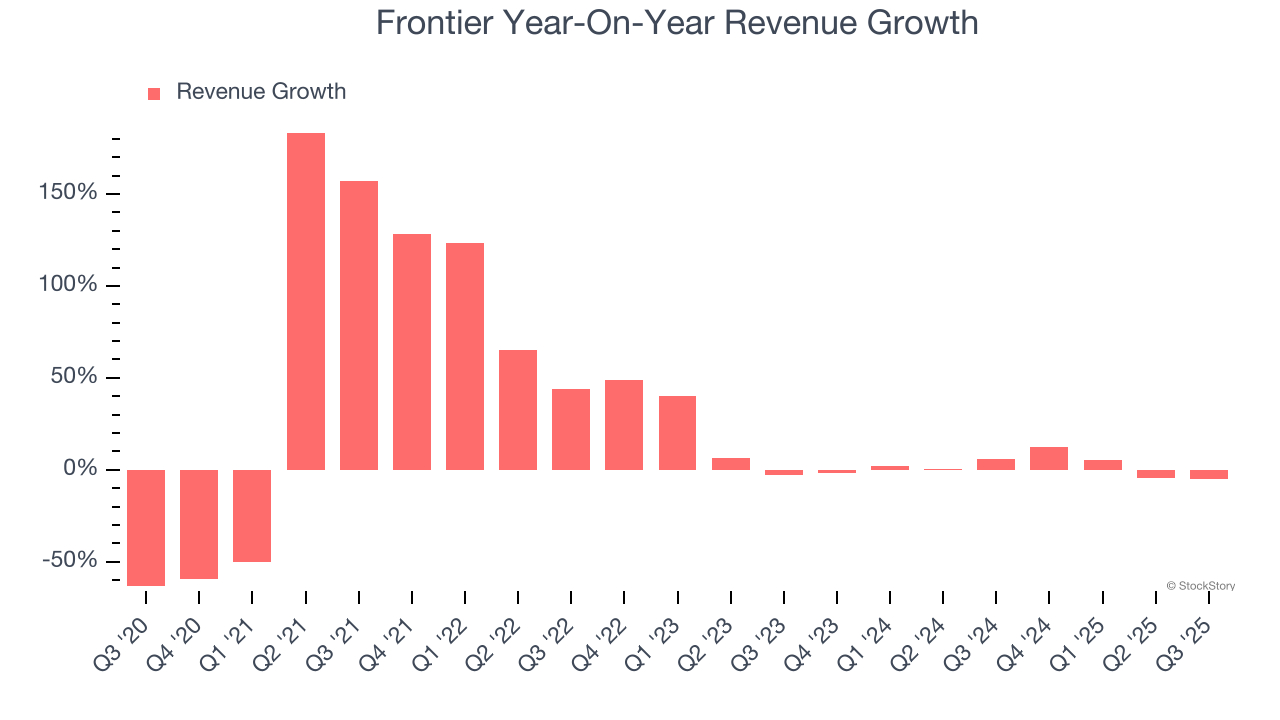

Ultra low-cost airline Frontier Group Holdings (NASDAQ:ULCC) fell short of the markets revenue expectations in Q3 CY2025, with sales falling 5.2% year on year to $886 million. Its non-GAAP loss of $0.34 per share was 7.7% above analysts’ consensus estimates.

Is now the time to buy Frontier? Find out by accessing our full research report, it’s free for active Edge members.

Frontier (ULCC) Q3 CY2025 Highlights:

- Revenue: $886 million vs analyst estimates of $901.8 million (5.2% year-on-year decline, 1.7% miss)

- Adjusted EPS: -$0.34 vs analyst estimates of -$0.37 (7.7% beat)

- Adjusted EBITDA: -$53 million vs analyst estimates of $132.7 million (-6% margin, significant miss)

- Adjusted EPS guidance for Q4 CY2025 is $0.12 at the midpoint, above analyst estimates of $0.10

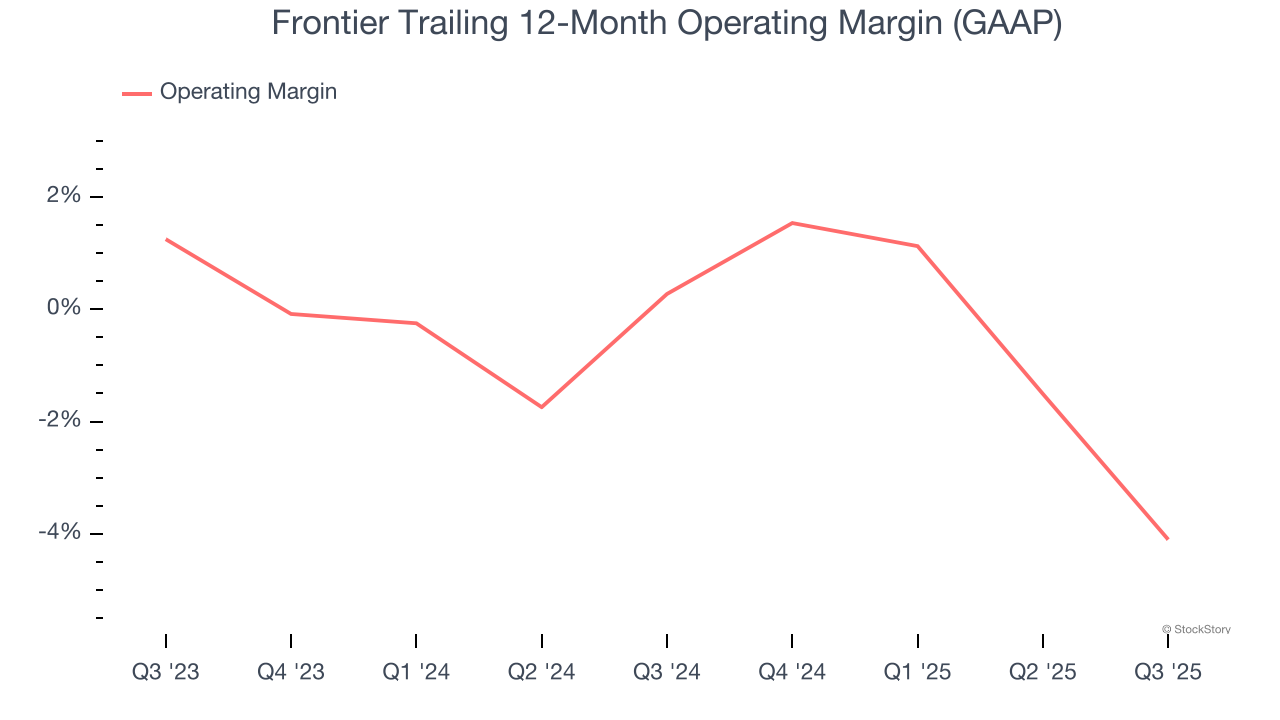

- Operating Margin: -8.7%, down from 2% in the same quarter last year

- Free Cash Flow was -$217 million compared to -$170 million in the same quarter last year

- Market Capitalization: $1.05 billion

Company Overview

Recognizable for the colorful animals adorning each aircraft tail, Frontier Group Holdings (NASDAQ:ULCC) is an ultra low-cost airline that provides budget-friendly flights throughout the United States and select international destinations in the Americas.

Revenue Growth

A company’s long-term sales performance is one signal of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Over the last five years, Frontier grew its sales at a 17.9% compounded annual growth rate. Although this growth is acceptable on an absolute basis, it fell slightly short of our standards for the consumer discretionary sector, which enjoys a number of secular tailwinds.

We at StockStory place the most emphasis on long-term growth, but within consumer discretionary, a stretched historical view may miss a company riding a successful new property or trend. Frontier’s recent performance shows its demand has slowed as its annualized revenue growth of 1.7% over the last two years was below its five-year trend.

This quarter, Frontier missed Wall Street’s estimates and reported a rather uninspiring 5.2% year-on-year revenue decline, generating $886 million of revenue.

Looking ahead, sell-side analysts expect revenue to grow 10.6% over the next 12 months. While this projection indicates its newer products and services will fuel better top-line performance, it is still below average for the sector.

The 1999 book Gorilla Game predicted Microsoft and Apple would dominate tech before it happened. Its thesis? Identify the platform winners early. Today, enterprise software companies embedding generative AI are becoming the new gorillas. a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Frontier’s operating margin has been trending down over the last 12 months and averaged negative 1.9% over the last two years. Unprofitable consumer discretionary companies with falling margins deserve extra scrutiny because they’re spending loads of money to stay relevant, an unsustainable practice.

This quarter, Frontier generated a negative 8.7% operating margin. The company's consistent lack of profits raise a flag.

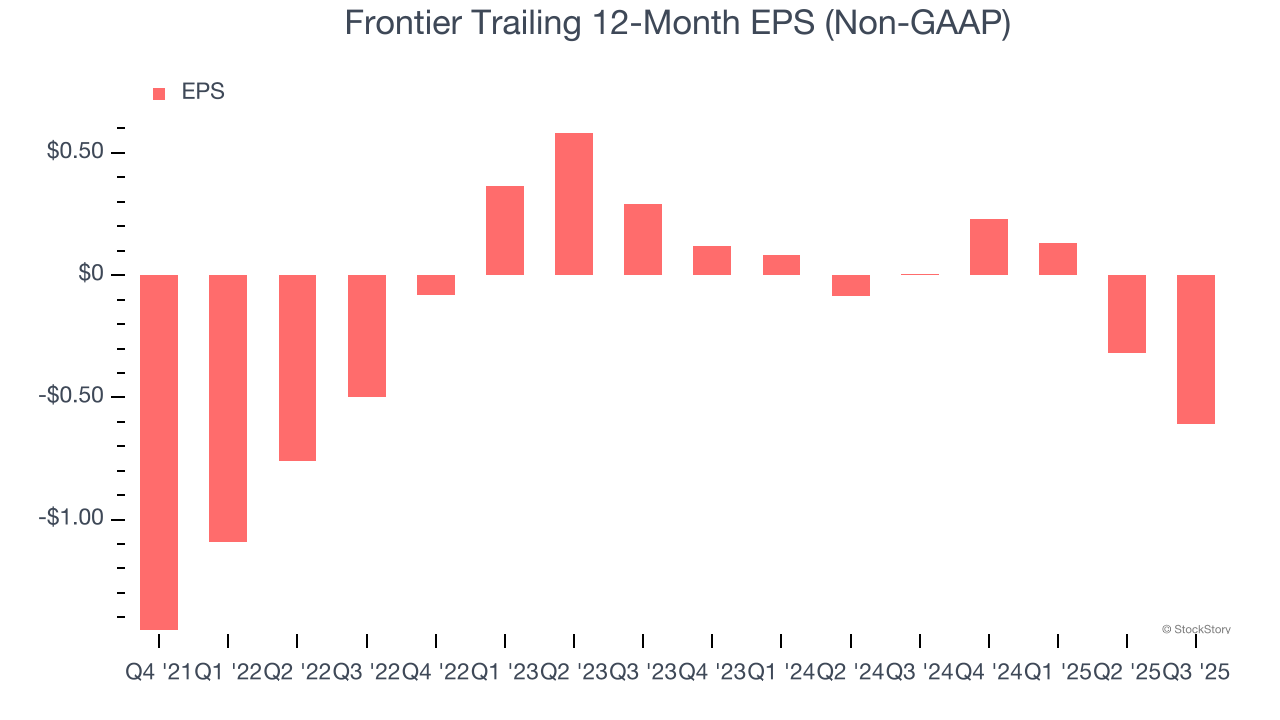

Earnings Per Share

Revenue trends explain a company’s historical growth, but the long-term change in earnings per share (EPS) points to the profitability of that growth – for example, a company could inflate its sales through excessive spending on advertising and promotions.

Although Frontier’s full-year earnings are still negative, it reduced its losses and improved its EPS by 8.7% annually over the last four years. The next few quarters will be critical for assessing its long-term profitability.

In Q3, Frontier reported adjusted EPS of negative $0.34, down from negative $0.05 in the same quarter last year. Despite falling year on year, this print beat analysts’ estimates by 7.7%. Over the next 12 months, Wall Street expects Frontier to improve its earnings losses. Analysts forecast its full-year EPS of negative $0.61 will advance to negative $0.15.

Key Takeaways from Frontier’s Q3 Results

We were impressed by Frontier’s optimistic EPS guidance for next quarter, which blew past analysts’ expectations. We were also glad its adjusted operating income outperformed Wall Street’s estimates. On the other hand, its EBITDA missed and its revenue fell short of Wall Street’s estimates. Zooming out, we think this was a mixed quarter. The stock remained flat at $4.59 immediately after reporting.

Is Frontier an attractive investment opportunity right now? The latest quarter does matter, but not nearly as much as longer-term fundamentals and valuation, when deciding if the stock is a buy. We cover that in our actionable full research report which you can read here, it’s free for active Edge members.