WesBanco’s 17.3% return over the past six months has outpaced the S&P 500 by 11.3%, and its stock price has climbed to $36.65 per share. This run-up might have investors contemplating their next move.

Is now the time to buy WesBanco, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Is WesBanco Not Exciting?

We’re happy investors have made money, but we're swiping left on WesBanco for now. Here are three reasons why WSBC doesn't excite us and a stock we'd rather own.

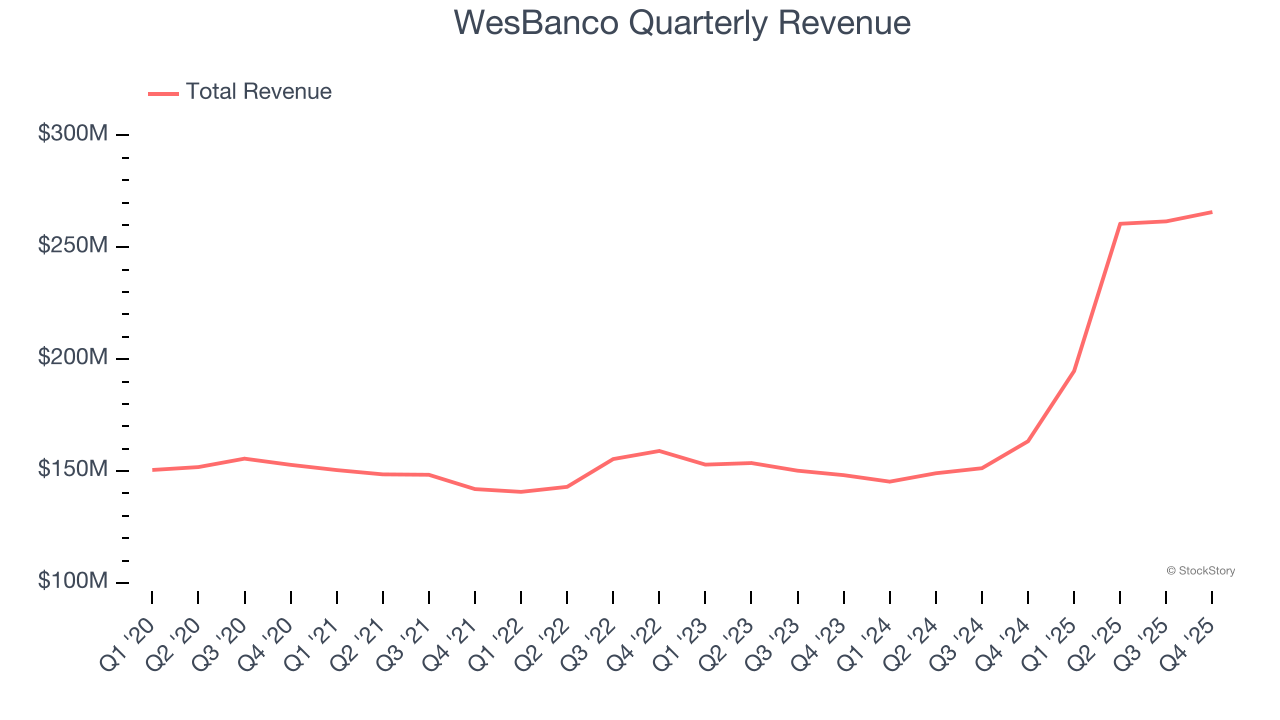

1. Long-Term Revenue Growth Disappoints

In general, banks make money from two primary sources. The first is net interest income, which is interest earned on loans, mortgages, and investments in securities minus interest paid out on deposits. The second source is non-interest income, which can come from bank account, credit card, wealth management, investing banking, and trading fees.

Unfortunately, WesBanco’s 10% annualized revenue growth over the last five years was mediocre. This fell short of our benchmark for the banking sector.

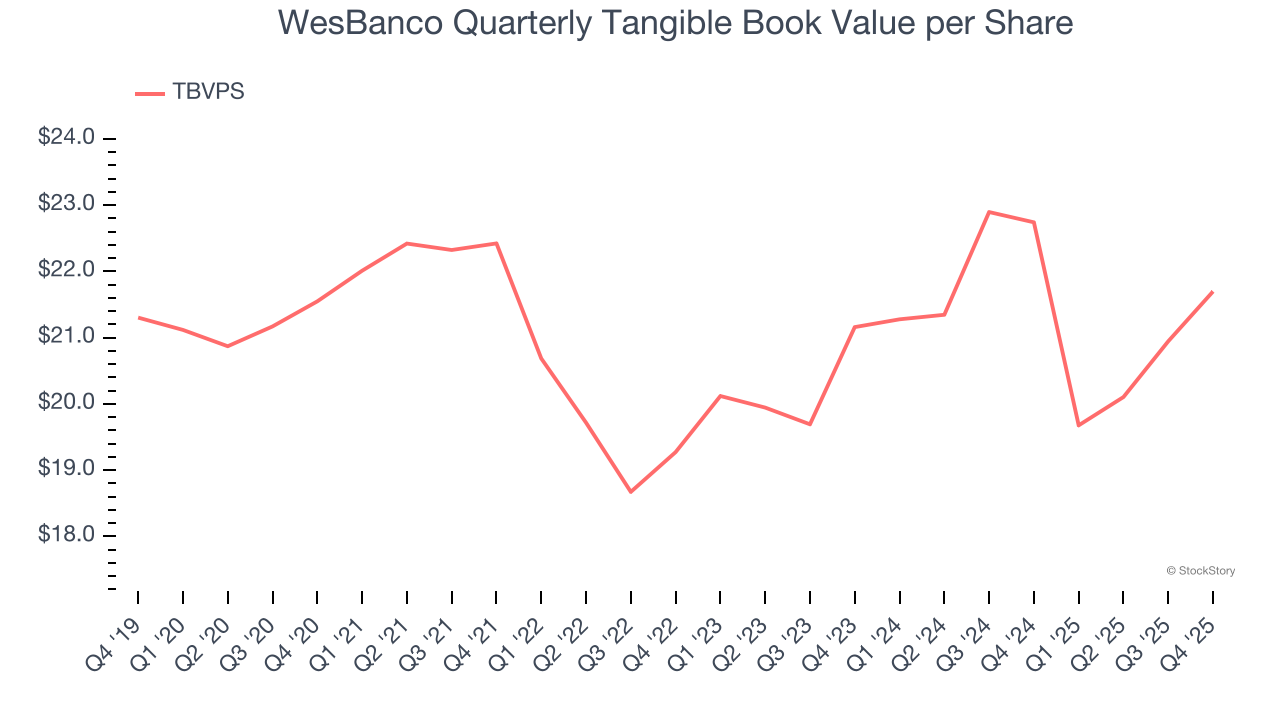

2. Substandard TBVPS Growth Indicates Limited Asset Expansion

In the banking industry, tangible book value per share (TBVPS) provides the clearest picture of shareholder value, as it focuses on concrete assets while excluding intangible items that may not hold value during challenging times.

Disappointingly for investors, WesBanco’s TBVPS grew at a weak 1.3% annual clip over the last two years.

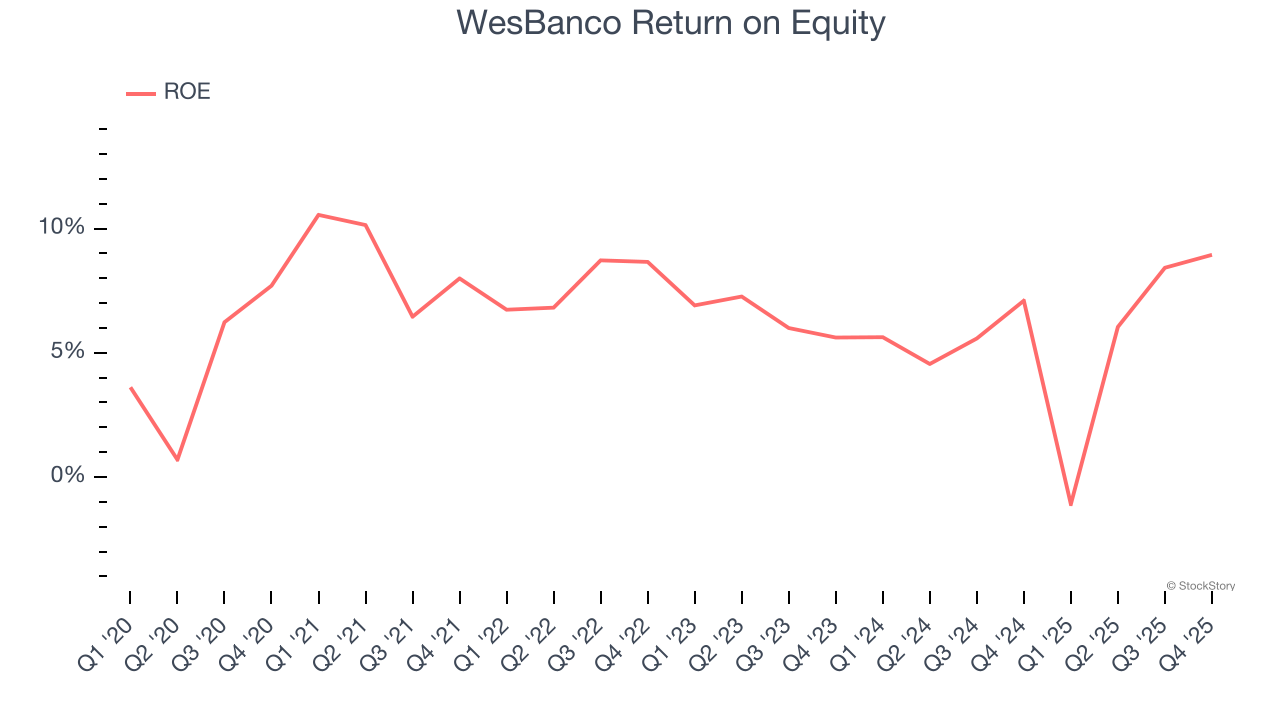

3. Previous Growth Initiatives Haven’t Impressed

Return on equity (ROE) reveals the profit generated per dollar of shareholder equity, which represents a key source of bank funding. Banks maintaining elevated ROE levels tend to accelerate wealth creation for shareholders via earnings retention, buybacks, and distributions.

Over the last five years, WesBanco has averaged an ROE of 6.9%, uninspiring for a company operating in a sector where the average shakes out around 7.5%.

Final Judgment

WesBanco isn’t a terrible business, but it isn’t one of our picks. With its shares outperforming the market lately, the stock trades at 0.9× forward P/B (or $36.65 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're fairly confident there are better investments elsewhere. We’d suggest looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of WesBanco

The market’s up big this year - but there’s a catch. Just 4 stocks account for half the S&P 500’s entire gain. That kind of concentration makes investors nervous, and for good reason. While everyone piles into the same crowded names, smart investors are hunting quality where no one’s looking - and paying a fraction of the price. Check out the high-quality names we’ve flagged in our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.