Over the last six months, WSFS Financial’s shares have sunk to $54.97, producing a disappointing 5.6% loss - a stark contrast to the S&P 500’s 9.9% gain. This might have investors contemplating their next move.

Is there a buying opportunity in WSFS Financial, or does it present a risk to your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Is WSFS Financial Not Exciting?

Even with the cheaper entry price, we're cautious about WSFS Financial. Here are three reasons there are better opportunities than WSFS and a stock we'd rather own.

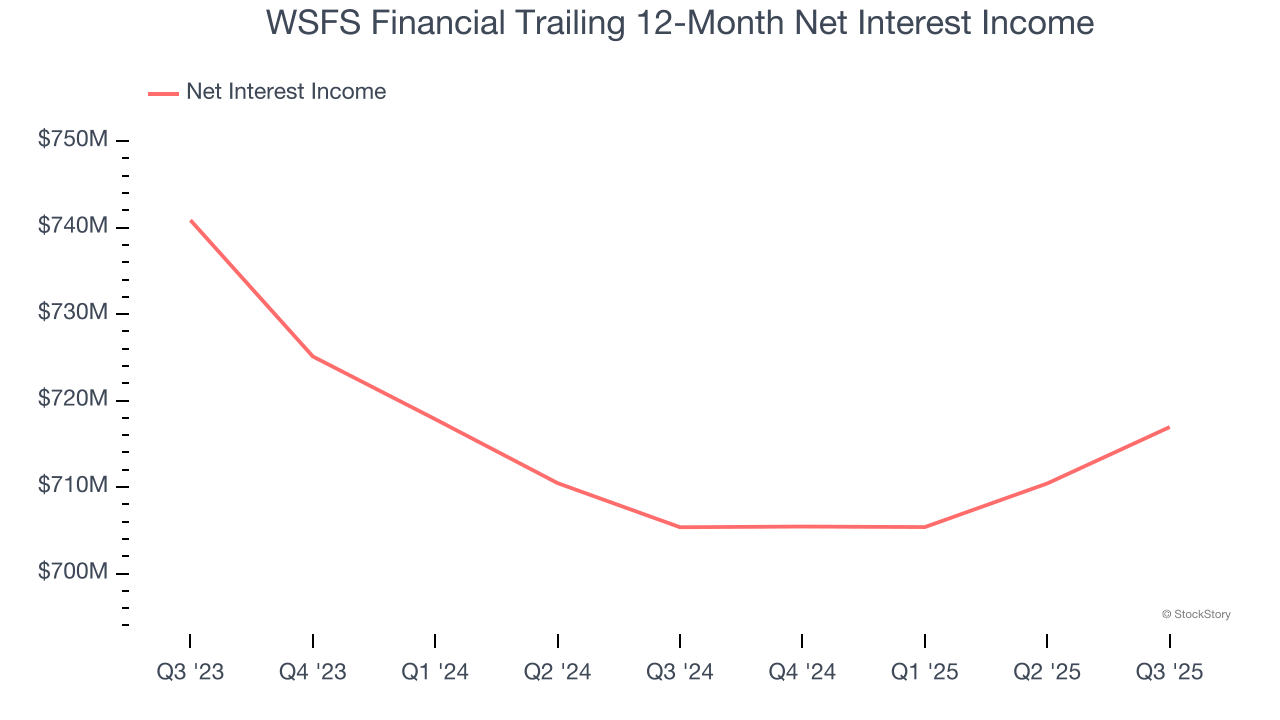

1. Net Interest Income Points to Soft Demand

Our experience and research show the market cares primarily about a bank’s net interest income growth as one-time fees are considered a lower-quality and non-recurring revenue source.

WSFS Financial’s net interest income has grown at a 9.3% annualized rate over the last five years, slightly worse than the broader banking industry and slower than its total revenue.

2. Projected Net Interest Income Growth Is Slim

Forecasted net interest income by Wall Street analysts signals a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect WSFS Financial’s net interest income to stall.

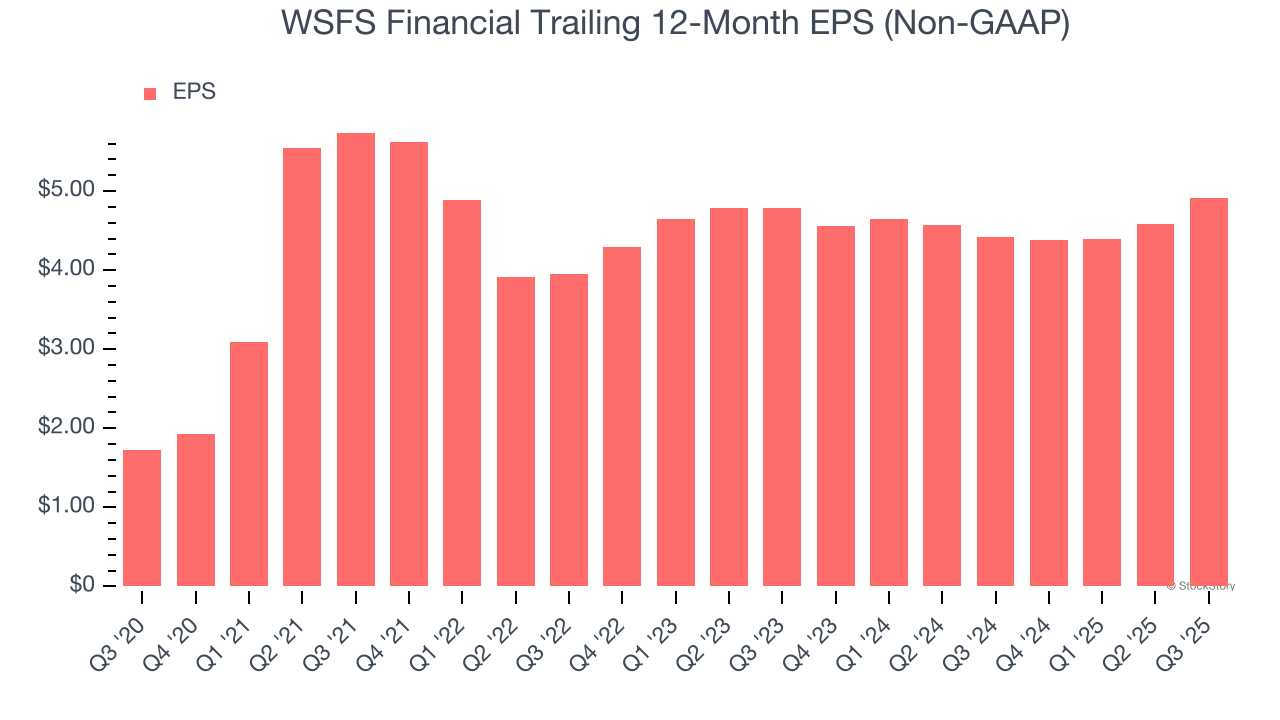

3. Recent EPS Growth Below Our Standards

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

WSFS Financial’s weak 1.2% annual EPS growth over the last two years aligns with its revenue trend. On the bright side, this tells us its incremental sales were profitable.

Final Judgment

WSFS Financial isn’t a terrible business, but it doesn’t pass our bar. After the recent drawdown, the stock trades at 1.1× forward P/B (or $54.97 per share). While this valuation is fair, the upside isn’t great compared to the potential downside. We're fairly confident there are better stocks to buy right now. Let us point you toward one of our top digital advertising picks.

Stocks We Like More Than WSFS Financial

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.