As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the research tools & consumables industry, including Agilent (NYSE:A) and its peers.

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

The 10 research tools & consumables stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 1.3% below.

In light of this news, share prices of the companies have held steady. On average, they are relatively unchanged since the latest earnings results.

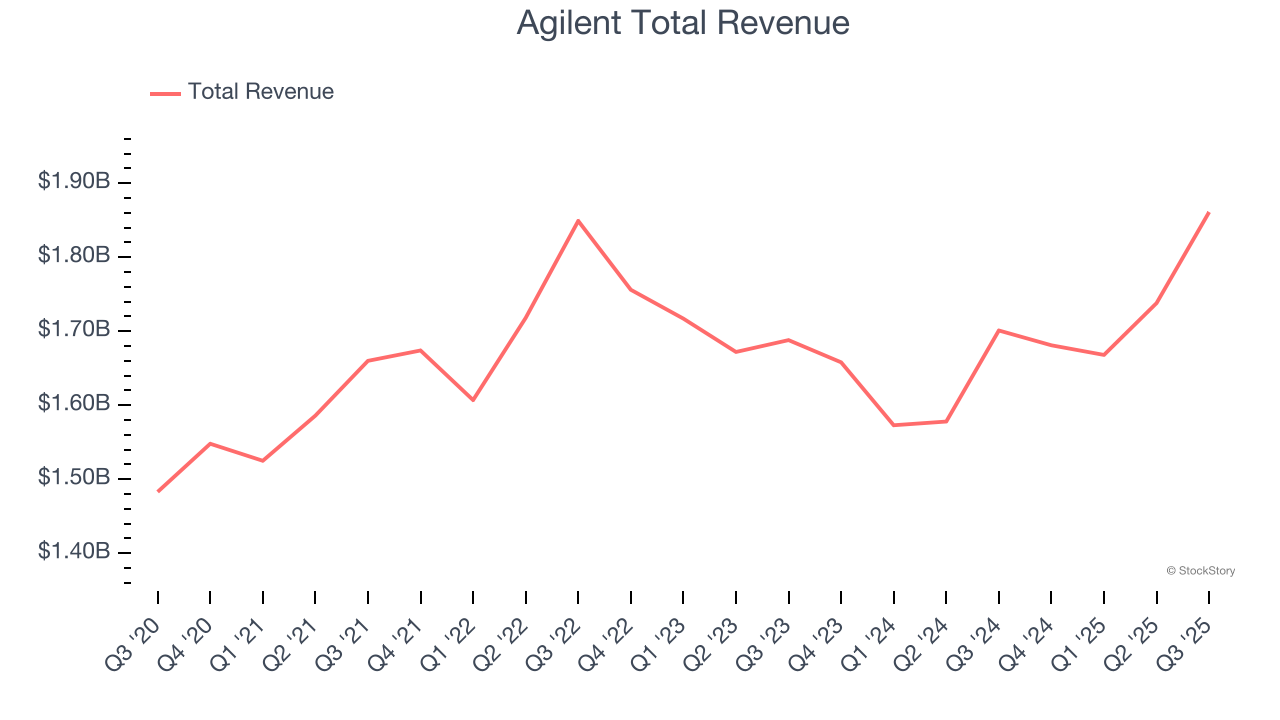

Agilent (NYSE:A)

Originally spun off from Hewlett-Packard in 1999 as its measurement and analytical division, Agilent Technologies (NYSE:A) provides analytical instruments, software, services, and consumables for laboratory workflows in life sciences, diagnostics, and applied chemical markets.

Agilent reported revenues of $1.86 billion, up 9.4% year on year. This print exceeded analysts’ expectations by 1.5%. Overall, it was a strong quarter for the company with a solid beat of analysts’ organic revenue estimates and a narrow beat of analysts’ revenue estimates.

Agilent scored the fastest revenue growth of the whole group. Investor expectations, however, were likely higher than Wall Street’s published projections, leaving some wishing for even better results (analysts’ consensus estimates are those published by big banks and advisory firms, not the investors who make buy and sell decisions). The stock is down 8.5% since reporting and currently trades at $140.84.

Is now the time to buy Agilent? Access our full analysis of the earnings results here, it’s free for active Edge members.

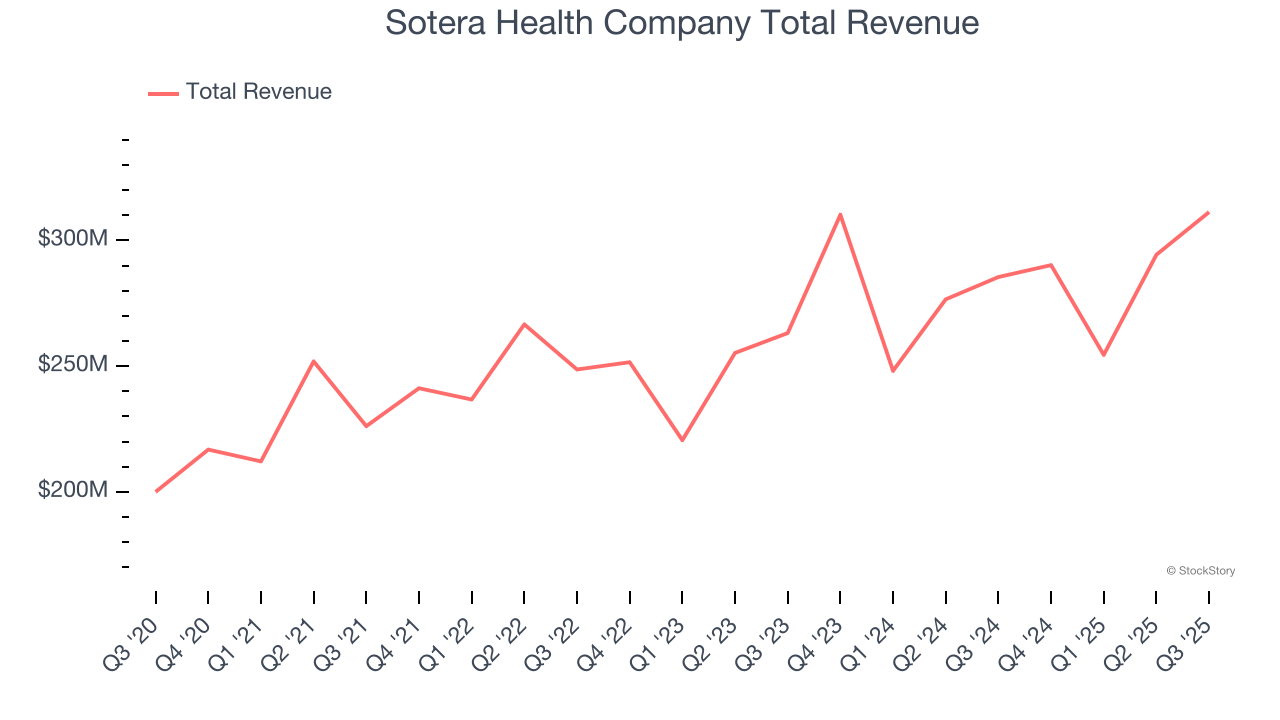

Best Q3: Sotera Health Company (NASDAQ:SHC)

With a critical role in ensuring the safety of millions of patients worldwide, Sotera Health (NASDAQGS:SHC) provides sterilization services, lab testing, and advisory services to ensure medical devices, pharmaceuticals, and food products are safe for use.

Sotera Health Company reported revenues of $311.3 million, up 9.1% year on year, outperforming analysts’ expectations by 2.6%. The business had an exceptional quarter with an impressive beat of analysts’ full-year EPS guidance estimates and an impressive beat of analysts’ organic revenue estimates.

However, the results were likely priced into the stock as it’s traded sideways since reporting. Shares currently sit at $16.71.

Is now the time to buy Sotera Health Company? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Avantor (NYSE:AVTR)

With roots dating back to 1904 and embedded in virtually every stage of scientific research and production, Avantor (NYSE:AVTR) provides mission-critical products, materials, and services to customers in biopharma, healthcare, education, and advanced technology industries.

Avantor reported revenues of $1.62 billion, down 5.3% year on year, falling short of analysts’ expectations by 1.4%. It was a softer quarter as it posted a slight miss of analysts’ revenue estimates and a miss of analysts’ organic revenue estimates.

Avantor delivered the slowest revenue growth in the group. As expected, the stock is down 26.4% since the results and currently trades at $11.11.

Read our full analysis of Avantor’s results here.

Danaher (NYSE:DHR)

Born from a real estate investment trust that transformed into a manufacturing powerhouse, Danaher (NYSE:DHR) is a global science and technology company that provides specialized equipment, software, and services for biotechnology, life sciences, and diagnostics.

Danaher reported revenues of $6.05 billion, up 4.4% year on year. This print beat analysts’ expectations by 0.6%. Aside from that, it was a mixed quarter as it also logged a beat of analysts’ EPS estimates but revenue guidance for next quarter missing analysts’ expectations significantly.

The stock is up 8.2% since reporting and currently trades at $223.94.

Read our full, actionable report on Danaher here, it’s free for active Edge members.

Bio-Techne (NASDAQ:TECH)

With a catalog of hundreds of thousands of specialized biological products used in laboratories worldwide, Bio-Techne (NASDAQ:TECH) develops and manufactures specialized reagents, instruments, and services that help researchers study biological processes and enable diagnostic testing and cell therapy development.

Bio-Techne reported revenues of $286.6 million, down 1% year on year. This result came in 1.7% below analysts' expectations. Overall, it was a softer quarter as it also produced a miss of analysts’ revenue estimates and a miss of analysts’ organic revenue estimates.

Bio-Techne had the weakest performance against analyst estimates among its peers. The stock is down 3.6% since reporting and currently trades at $58.91.

Read our full, actionable report on Bio-Techne here, it’s free for active Edge members.

Market Update

In response to the Fed’s rate hikes in 2022 and 2023, inflation has been gradually trending down from its post-pandemic peak, trending closer to the Fed’s 2% target. Despite higher borrowing costs, the economy has avoided flashing recessionary signals. This is the much-desired soft landing that many investors hoped for. The recent rate cuts (0.5% in September and 0.25% in November 2024) have bolstered the stock market, making 2024 a strong year for equities. Donald Trump’s presidential win in November sparked additional market gains, sending indices to record highs in the days following his victory. However, debates continue over possible tariffs and corporate tax adjustments, raising questions about economic stability in 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.