APi currently trades at $44.79 and has been a dream stock for shareholders. It’s returned 275% since February 2021, blowing past the S&P 500’s 77% gain. The company has also beaten the index over the past six months as its stock price is up 28.1% thanks to its solid quarterly results.

Is now the time to buy APi, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free.

Why Is APi Not Exciting?

Despite the momentum, we don't have much confidence in APi. Here are three reasons there are better opportunities than APG and a stock we'd rather own.

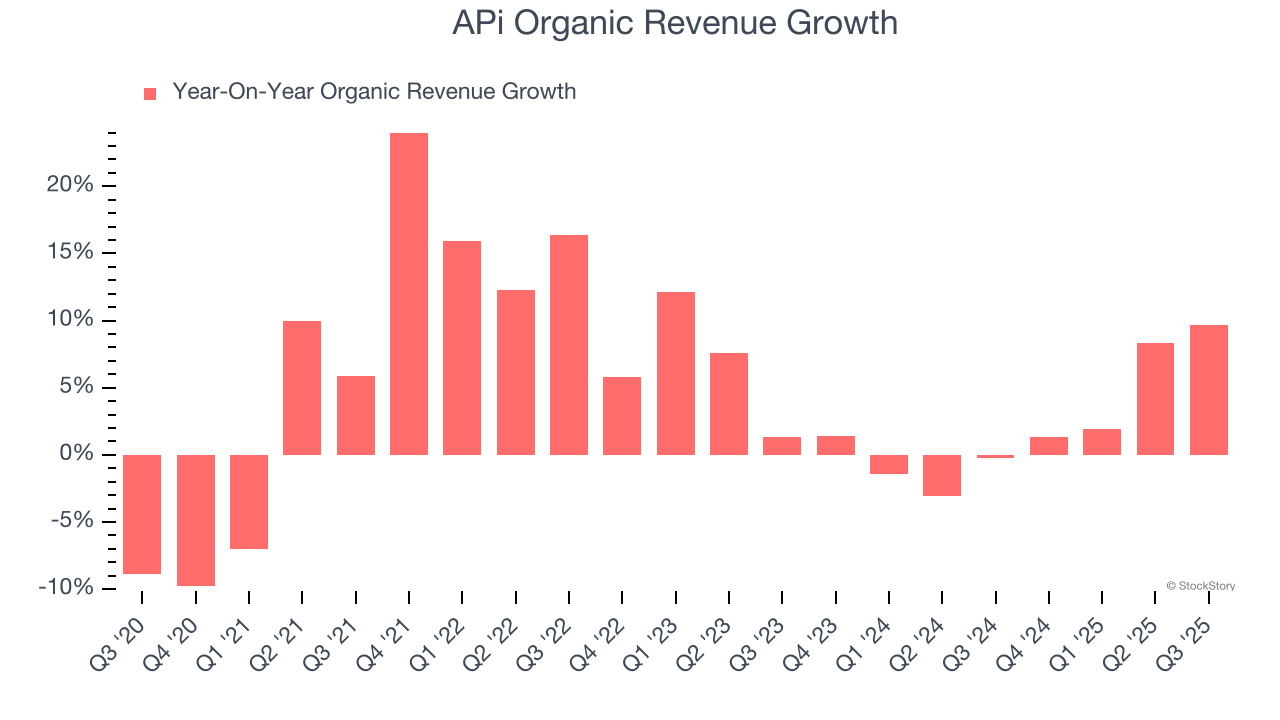

1. Slow Organic Growth Suggests Waning Demand In Core Business

Investors interested in Construction and Maintenance Services companies should track organic revenue in addition to reported revenue. This metric gives visibility into APi’s core business because it excludes one-time events such as mergers, acquisitions, and divestitures along with foreign currency fluctuations - non-fundamental factors that can manipulate the income statement.

Over the last two years, APi’s organic revenue averaged 2.2% year-on-year growth. This performance was underwhelming and suggests it may need to improve its products, pricing, or go-to-market strategy, which can add an extra layer of complexity to its operations.

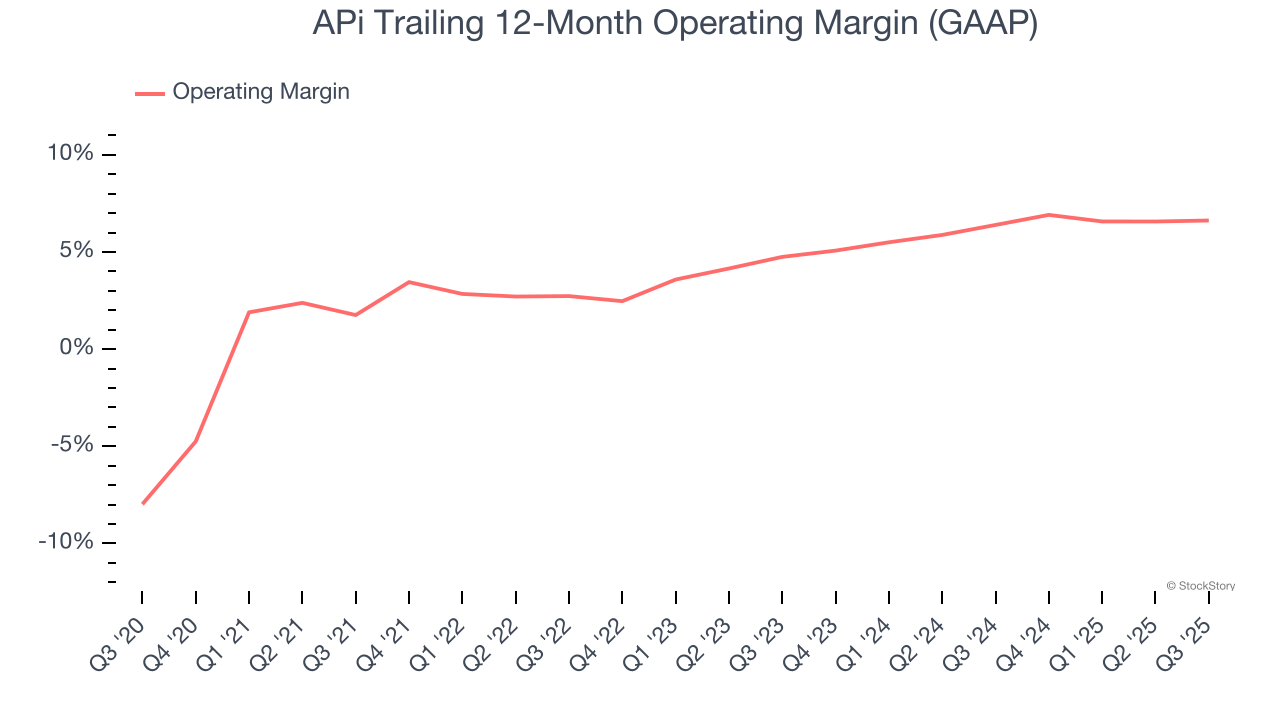

2. Weak Operating Margin Could Cause Trouble

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling those products, and most importantly, keeping them relevant through research and development.

APi was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.8% was weak for an industrials business. This result isn’t too surprising given its low gross margin as a starting point.

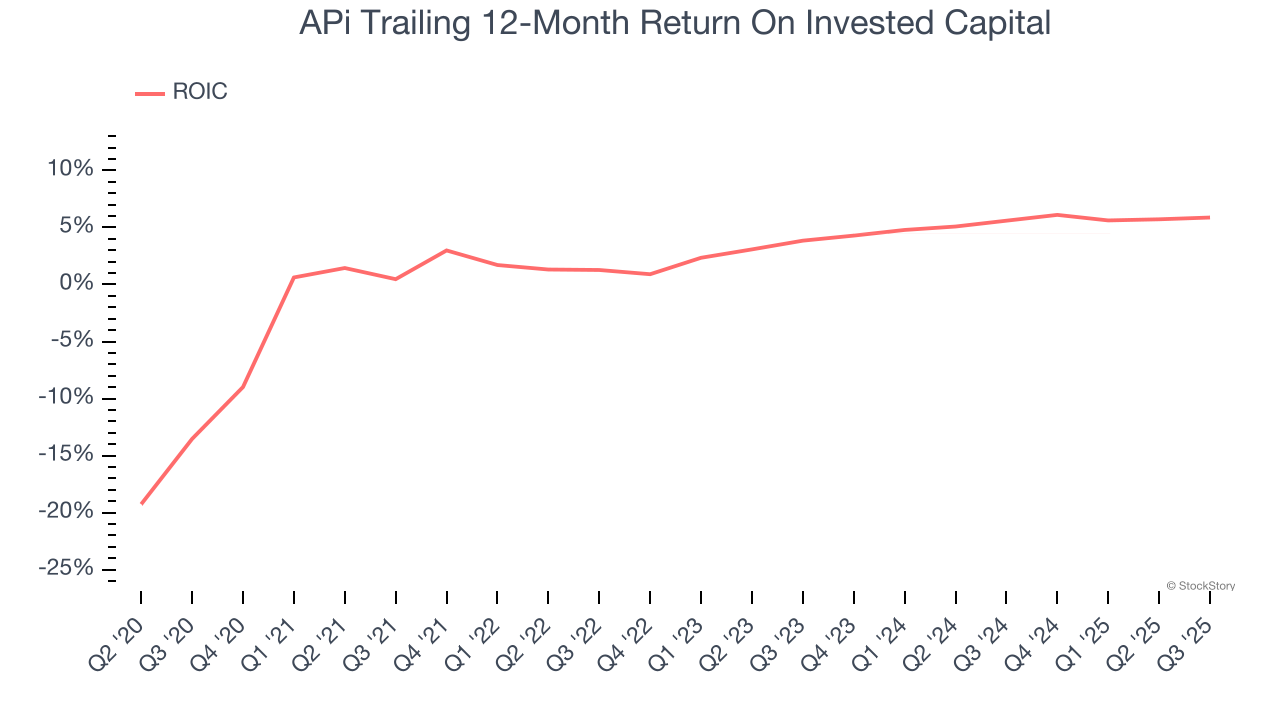

3. Previous Growth Initiatives Haven’t Impressed

Growth gives us insight into a company’s long-term potential, but how capital-efficient was that growth? A company’s ROIC explains this by showing how much operating profit it makes compared to the money it has raised (debt and equity).

APi historically did a mediocre job investing in profitable growth initiatives. Its five-year average ROIC was 3.4%, lower than the typical cost of capital (how much it costs to raise money) for industrials companies.

Final Judgment

APi isn’t a terrible business, but it doesn’t pass our quality test. With its shares beating the market recently, the stock trades at 27.6× forward P/E (or $44.79 per share). Investors with a higher risk tolerance might like the company, but we think the potential downside is too great. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.