Over the past six months, Cadence Bank has been a great trade, beating the S&P 500 by 16.8%. Its stock price has climbed to $42.80, representing a healthy 28% increase. This run-up might have investors contemplating their next move.

Is there a buying opportunity in Cadence Bank, or does it present a risk to your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Is Cadence Bank Not Exciting?

We’re glad investors have benefited from the price increase, but we're sitting this one out for now. Here are three reasons we avoid CADE and a stock we'd rather own.

1. Lackluster Revenue Growth

We at StockStory place the most emphasis on long-term growth, but within financials, a stretched historical view may miss recent interest rate changes, market returns, and industry trends. Cadence Bank’s recent performance shows its demand has slowed as its annualized revenue growth of 4.3% over the last two years was below its five-year trend.  Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

Note: Quarters not shown were determined to be outliers, impacted by outsized investment gains/losses that are not indicative of the recurring fundamentals of the business.

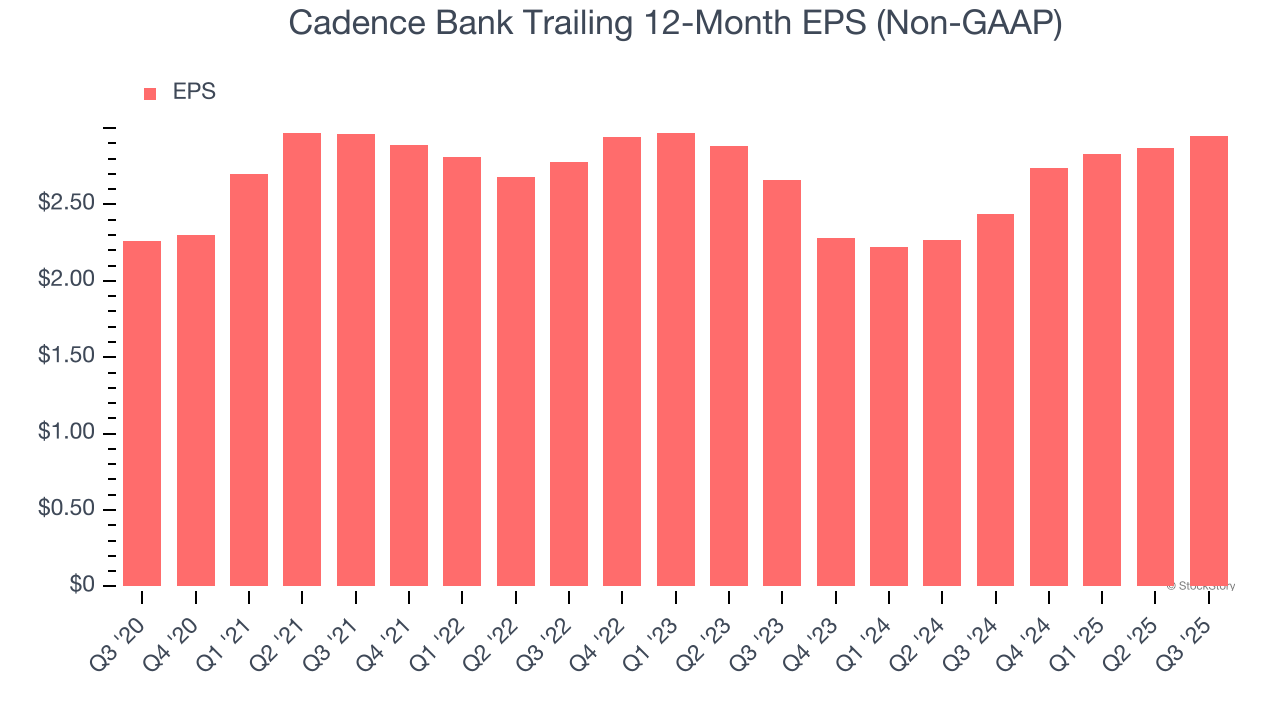

2. EPS Barely Growing

Analyzing the long-term change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Cadence Bank’s EPS grew at a weak 5.5% compounded annual growth rate over the last five years, lower than its 13.1% annualized revenue growth. This tells us the company became less profitable on a per-share basis as it expanded.

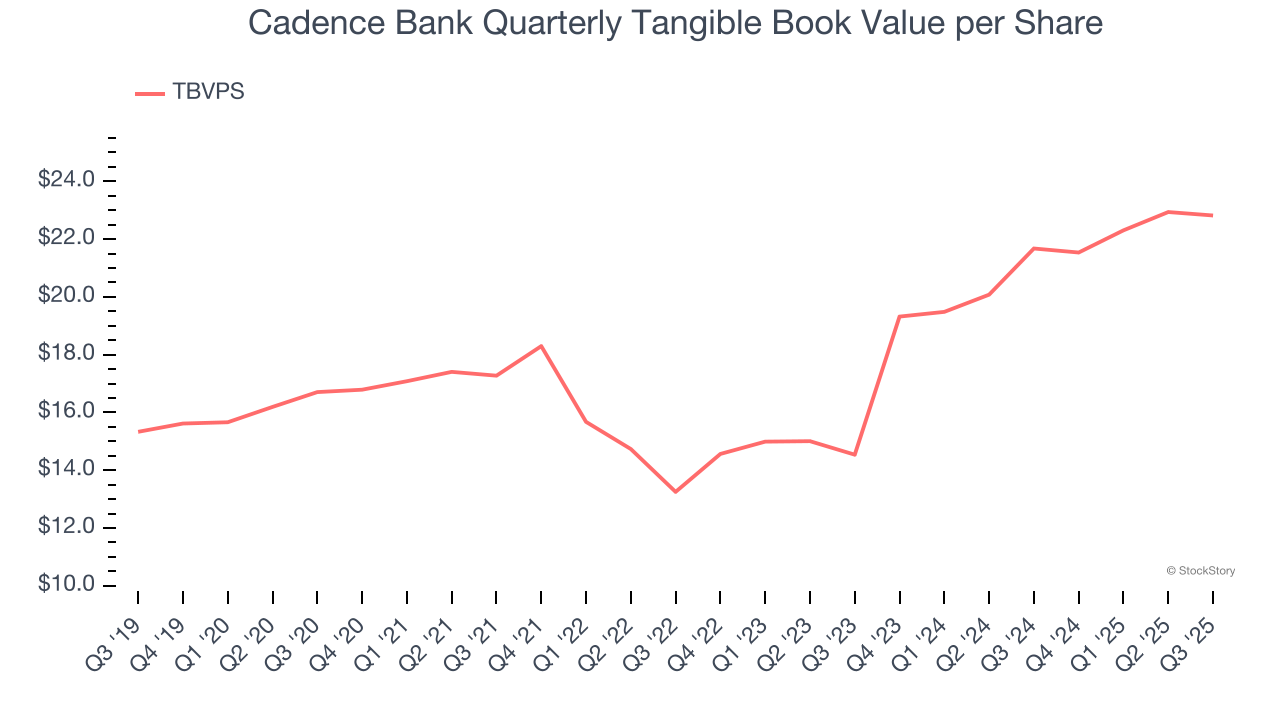

3. Projected TBVPS Growth Is Slim

Tangible book value per share (TBVPS) growth is driven by a bank’s ability to earn more than its cost of capital through lending activities while maintaining a strong balance sheet.

Over the next 12 months, Consensus estimates call for Cadence Bank’s TBVPS to grow by 10.6% to $25.23, mediocre growth rate.

Final Judgment

Cadence Bank’s business quality ultimately falls short of our standards. With its shares topping the market in recent months, the stock trades at 1.3× forward P/B (or $42.80 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're fairly confident there are better investments elsewhere. We’d recommend looking at one of Charlie Munger’s all-time favorite businesses.

Stocks We Would Buy Instead of Cadence Bank

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.