Over the past six months, Dell’s shares (currently trading at $120.75) have posted a disappointing 12.7% loss, well below the S&P 500’s 6.6% gain. This might have investors contemplating their next move.

Is now the time to buy Dell, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Why Is Dell Not Exciting?

Even though the stock has become cheaper, we don't have much confidence in Dell. Here are three reasons we avoid DELL and a stock we'd rather own.

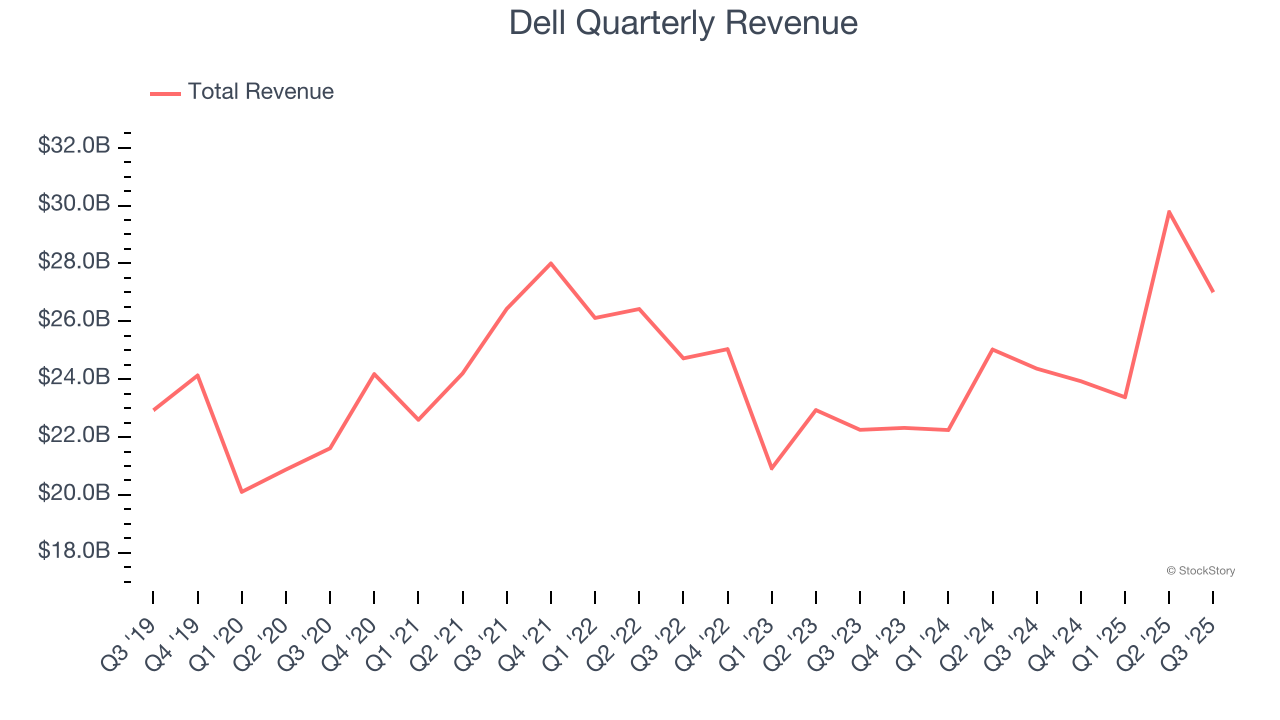

1. Long-Term Revenue Growth Disappoints

A company’s long-term performance is an indicator of its overall quality. Even a bad business can shine for one or two quarters, but a top-tier one grows for years. Unfortunately, Dell’s 3.7% annualized revenue growth over the last five years was tepid. This fell short of our benchmark for the business services sector.

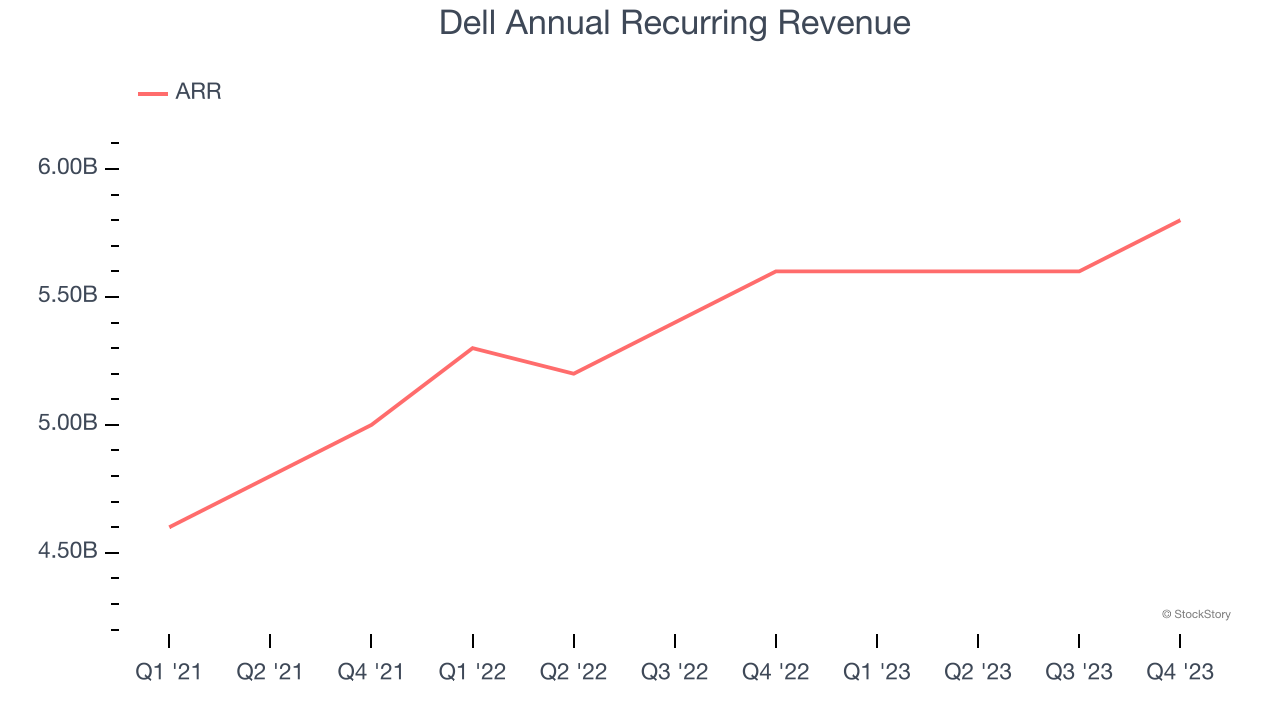

2. Weak ARR Growth Points to Soft Demand

Investors interested in Hardware & Infrastructure companies should track ARR (annual recurring revenue) in addition to reported revenue. This metric shows how much Dell expects to collect from its existing customer base in the next 12 months, giving visibility into its future revenue streams.

Over the last two years, Dell’s ARR averaged 3.6% year-on-year growth. This performance was underwhelming and suggests that increasing competition is causing challenges in securing longer-term commitments.

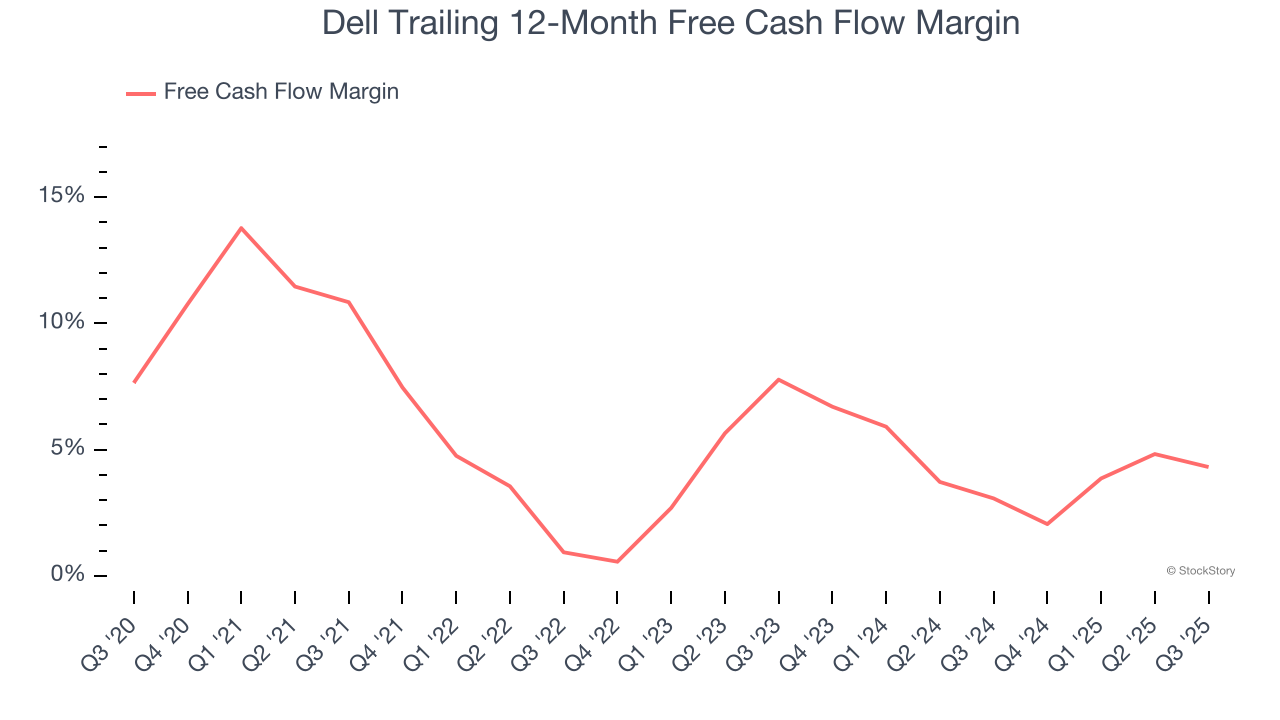

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Dell’s margin dropped by 6.5 percentage points over the last five years. If its declines continue, it could signal increasing investment needs and capital intensity. Dell’s free cash flow margin for the trailing 12 months was 4.3%.

Final Judgment

Dell’s business quality ultimately falls short of our standards. After the recent drawdown, the stock trades at 10× forward P/E (or $120.75 per share). While this valuation is reasonable, we don’t really see a big opportunity at the moment. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward one of our all-time favorite software stocks.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.