Even though ESCO (currently trading at $201.90 per share) has gained 6.1% over the last six months, it has lagged the S&P 500’s 13.3% return during that period. This may have investors wondering how to approach the situation.

Taking into account the weaker price action, does ESE warrant a spot on your radar, or is it better left off your list? Find out in our full research report, it’s free for active Edge members.

Why Is ESCO a Good Business?

A developer of the communication systems used in the Batmobile of “The Dark Knight,” ESCO (NYSE:ESE) is a provider of engineered components for the aerospace, defense, and utility sectors.

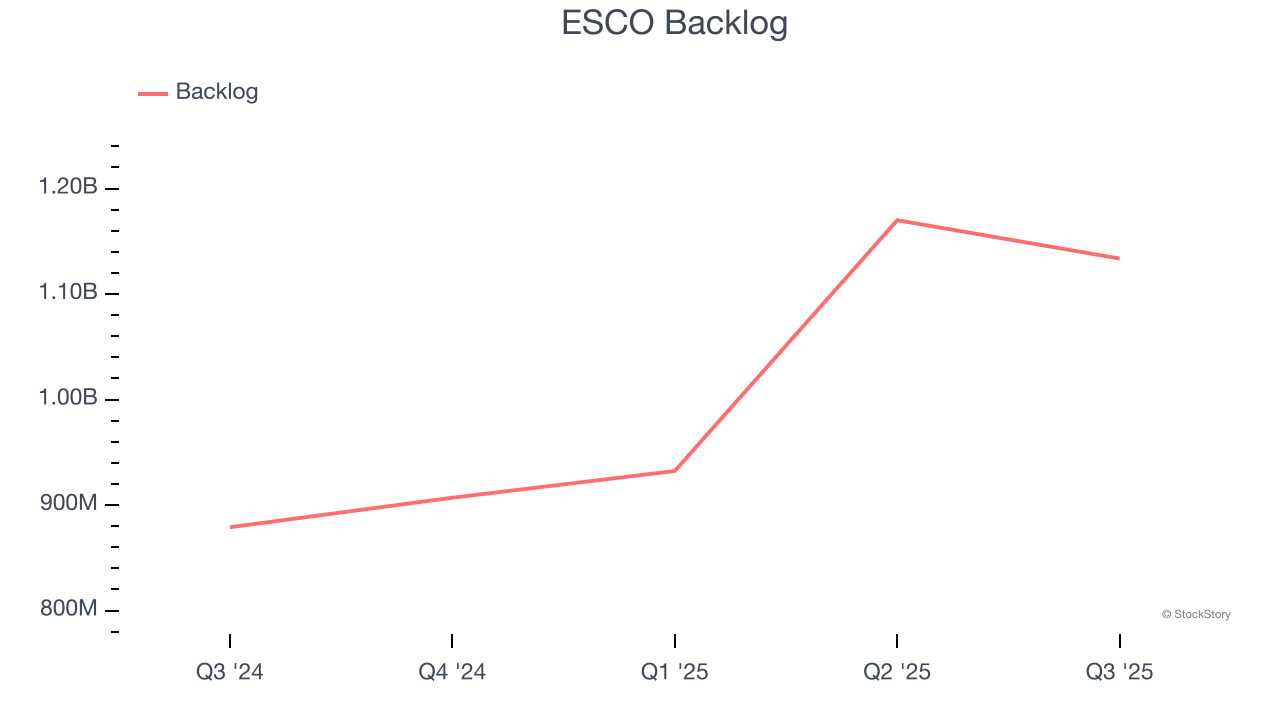

1. Surging Backlog Locks In Future Sales

In addition to reported revenue, backlog is a useful data point for analyzing Engineered Components and Systems companies. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into ESCO’s future revenue streams.

ESCO’s backlog punched in at $1.13 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 29%. This performance was fantastic and shows the company has a robust sales pipeline because it is accumulating more orders than it can fulfill. Its growth also suggests that customers are committing to ESCO for the long term, enhancing the business’s predictability.

2. Operating Margin Rising, Profits Up

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Looking at the trend in its profitability, ESCO’s operating margin rose by 4.3 percentage points over the last five years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 15.8%.

3. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

ESCO’s EPS grew at an astounding 18% compounded annual growth rate over the last five years, higher than its 9.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

Final Judgment

These are just a few reasons why we're bullish on ESCO. With its shares trailing the market in recent months, the stock trades at 26.4× forward P/E (or $201.90 per share). Is now a good time to initiate a position? See for yourself in our in-depth research report, it’s free for active Edge members.

Stocks We Like Even More Than ESCO

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.