Even though First Commonwealth Financial (currently trading at $17.20 per share) has gained 8.2% over the last six months, it has lagged the S&P 500’s 13.9% return during that period. This was partly due to its softer quarterly results and may have investors wondering how to approach the situation.

Is now the time to buy First Commonwealth Financial, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free for active Edge members.

Why Is First Commonwealth Financial Not Exciting?

We don't have much confidence in First Commonwealth Financial. Here are three reasons there are better opportunities than FCF and a stock we'd rather own.

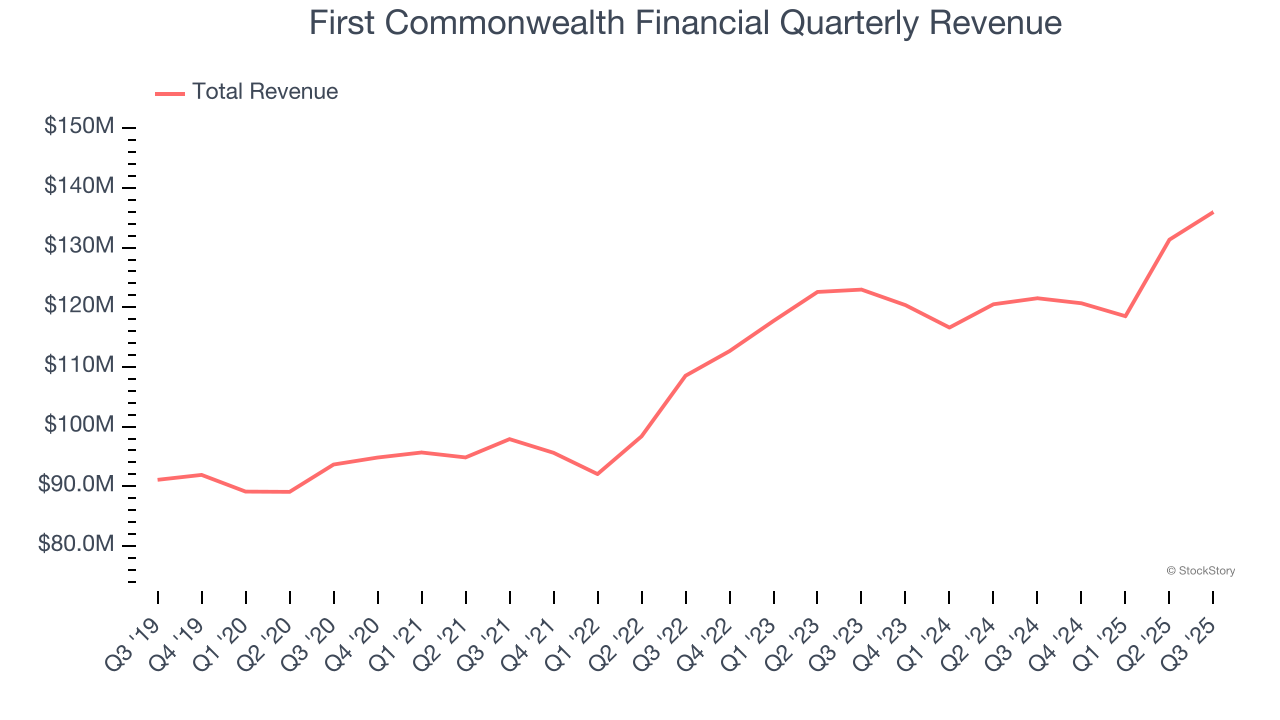

1. Long-Term Revenue Growth Disappoints

From lending activities to service fees, most banks build their revenue model around two income sources. Interest rate spreads between loans and deposits create the first stream, with the second coming from charges on everything from basic bank accounts to complex investment banking transactions.

Over the last five years, First Commonwealth Financial grew its revenue at a tepid 6.8% compounded annual growth rate. This was below our standard for the banking sector.

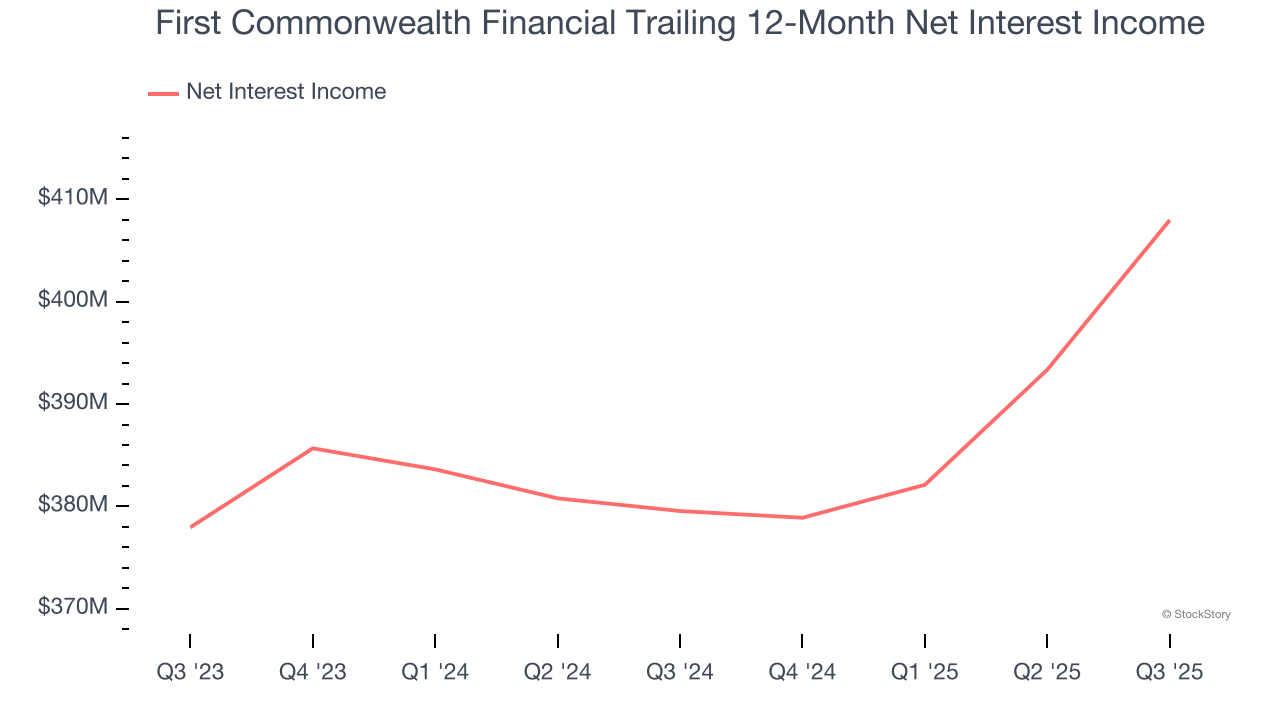

2. Net Interest Income Points to Soft Demand

While bank generate revenue from multiple sources, investors view net interest income as a cornerstone - its predictable, recurring characteristics stand in sharp contrast to the volatility of one-time fees.

First Commonwealth Financial’s net interest income has grown at a 8.6% annualized rate over the last five years, slightly worse than the broader banking industry.

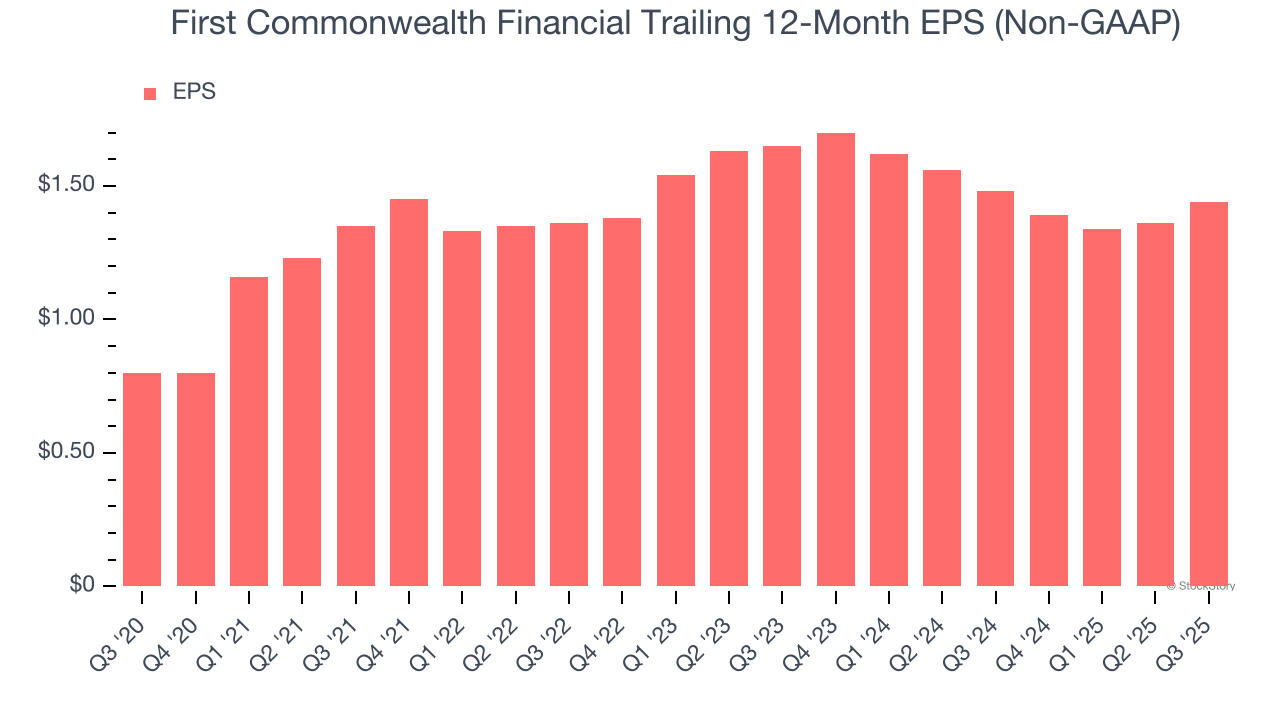

3. EPS Took a Dip Over the Last Two Years

Although long-term earnings trends give us the big picture, we like to analyze EPS over a shorter period to see if we are missing a change in the business.

Sadly for First Commonwealth Financial, its EPS declined by 6.6% annually over the last two years while its revenue grew by 3.2%. This tells us the company became less profitable on a per-share basis as it expanded.

Final Judgment

First Commonwealth Financial isn’t a terrible business, but it isn’t one of our picks. With its shares underperforming the market lately, the stock trades at 1.1× forward P/B (or $17.20 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are more exciting stocks to buy at the moment. Let us point you toward a safe-and-steady industrials business benefiting from an upgrade cycle.

Stocks We Like More Than First Commonwealth Financial

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.