Let’s dig into the relative performance of Genesco (NYSE:GCO) and its peers as we unravel the now-completed Q3 footwear earnings season.

Before the advent of the internet, styles changed, but consumers mainly bought shoes by visiting local brick-and-mortar shoe, department, and specialty stores. Today, not only do styles change more frequently as fads travel through social media and the internet but consumers are also shifting the way they buy their goods, favoring omnichannel and e-commerce experiences. Some footwear companies have made concerted efforts to adapt while those who are slower to move may fall behind.

The 7 footwear stocks we track reported a satisfactory Q3. As a group, revenues beat analysts’ consensus estimates by 1.5% while next quarter’s revenue guidance was 7.9% above.

While some footwear stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 3.4% since the latest earnings results.

Genesco (NYSE:GCO)

Spanning a broad range of styles, brands, and prices, Genesco (NYSE:GCO) sells footwear, apparel, and accessories through multiple brands and banners.

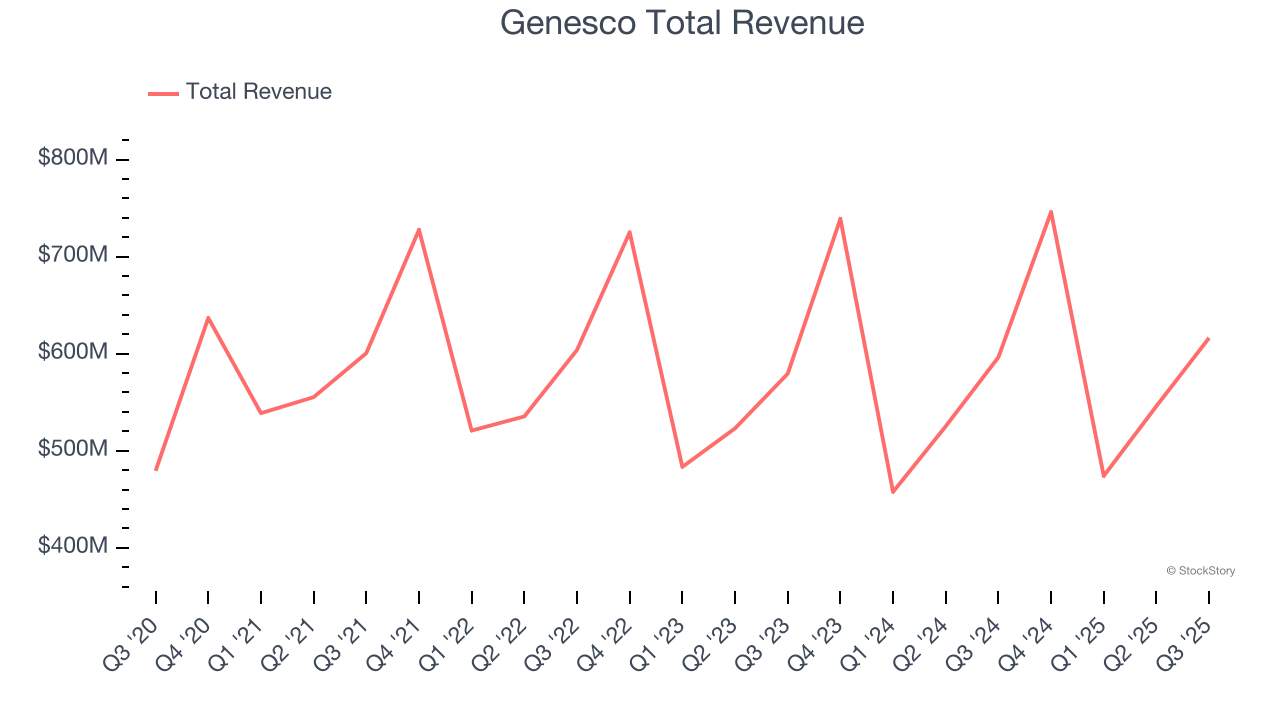

Genesco reported revenues of $616.2 million, up 3.3% year on year. This print was in line with analysts’ expectations, but overall, it was a softer quarter for the company with full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ EPS estimates.

Mimi E. Vaughn, Genesco's Board Chair, President and Chief Executive Officer, said, “We delivered another quarter of top and bottom-line growth, marking our fifth consecutive quarter of positive comparable sales increases. The third quarter demonstrated the power of our strategic initiatives, with Journeys delivering strong double-digit comp growth during back-to-school on top of double-digit growth last year. This performance reinforces that when consumers shop for footwear, they are increasingly choosing Journeys, underscoring the momentum of our product elevation and diversification strategy as we continue to gain market share and establish ourselves as the destination for the style-led teen.”

Unsurprisingly, the stock is down 31.7% since reporting and currently trades at $24.01.

Read our full report on Genesco here, it’s free for active Edge members.

Best Q3: Nike (NYSE:NKE)

Originally selling Japanese Onitsuka Tiger sneakers as Blue Ribbon Sports, Nike (NYSE:NKE) is a global titan in athletic footwear, apparel, equipment, and accessories.

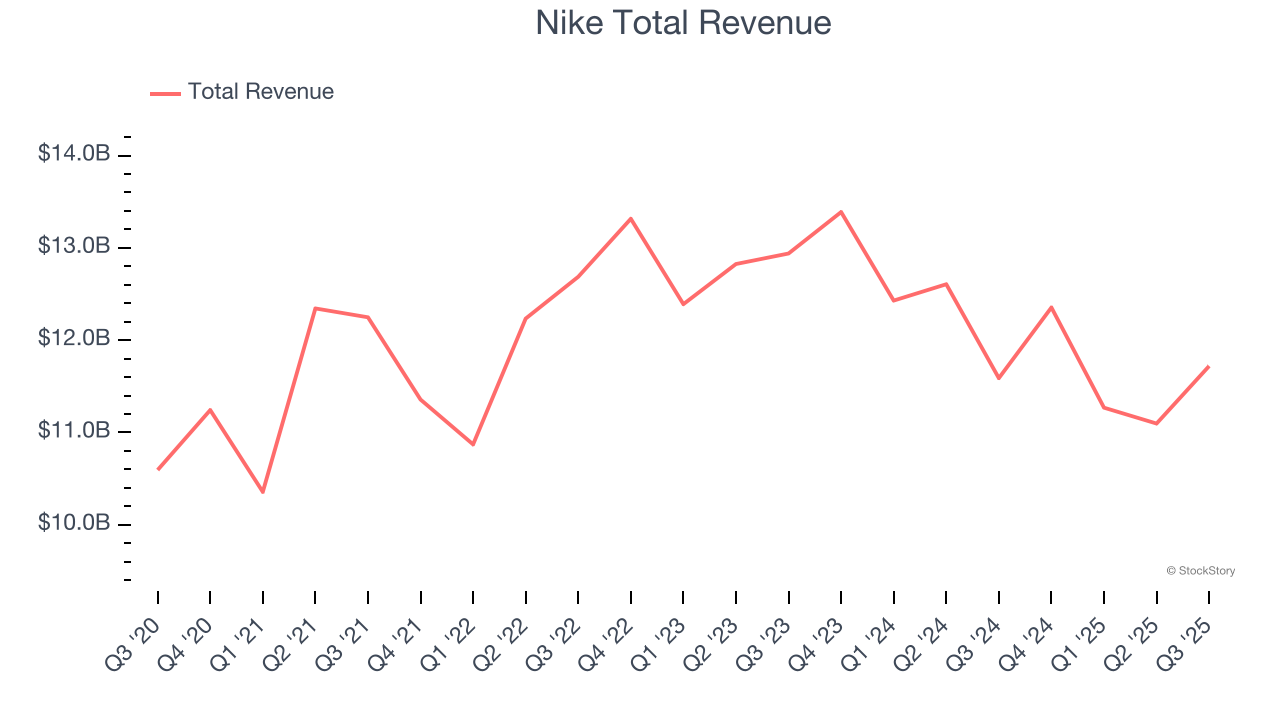

Nike reported revenues of $11.72 billion, up 1.1% year on year, outperforming analysts’ expectations by 6.5%. The business had an incredible quarter with an impressive beat of analysts’ constant currency revenue estimates and a beat of analysts’ EPS estimates.

Nike delivered the biggest analyst estimates beat among its peers. Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 5.6% since reporting. It currently trades at $65.84.

Is now the time to buy Nike? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Caleres (NYSE:CAL)

The owner of Dr. Scholl's, Caleres (NYSE:CAL) is a footwear company offering a range of styles.

Caleres reported revenues of $790.1 million, up 6.6% year on year, exceeding analysts’ expectations by 2.8%. Still, it was a disappointing quarter as it posted full-year EPS guidance missing analysts’ expectations significantly and a significant miss of analysts’ adjusted operating income estimates.

As expected, the stock is down 2.9% since the results and currently trades at $13.12.

Read our full analysis of Caleres’s results here.

Crocs (NASDAQ:CROX)

Founded in 2002, Crocs (NASDAQ:CROX) sells casual footwear and is known for its iconic clog shoe.

Crocs reported revenues of $996.3 million, down 6.2% year on year. This number topped analysts’ expectations by 3.3%. It was an exceptional quarter as it also logged an impressive beat of analysts’ constant currency revenue estimates and EPS guidance for next quarter exceeding analysts’ expectations.

Crocs had the slowest revenue growth among its peers. The stock is up 2.4% since reporting and currently trades at $86.75.

Read our full, actionable report on Crocs here, it’s free for active Edge members.

Steven Madden (NASDAQ:SHOO)

As seen in the infamous Wolf of Wall Street movie, Steven Madden (NASDAQ:SHOO) is a fashion brand famous for its trendy and innovative footwear, appealing to a young and style-conscious audience.

Steven Madden reported revenues of $667.9 million, up 6.9% year on year. This result missed analysts’ expectations by 4%. Zooming out, it was actually a strong quarter as it produced EPS guidance for next quarter exceeding analysts’ expectations and revenue guidance for next quarter exceeding analysts’ expectations.

Steven Madden had the weakest performance against analyst estimates among its peers. The stock is up 33.2% since reporting and currently trades at $43.73.

Read our full, actionable report on Steven Madden here, it’s free for active Edge members.

Market Update

Thanks to the Fed’s series of rate hikes in 2022 and 2023, inflation has cooled significantly from its post-pandemic highs, drawing closer to the 2% goal. This disinflation has occurred without severely impacting economic growth, suggesting the success of a soft landing. The stock market thrived in 2024, spurred by recent rate cuts (0.5% in September and 0.25% in November), and a notable surge followed Donald Trump’s presidential election win in November, propelling indices to historic highs. Nonetheless, the outlook for 2025 remains clouded by potential trade policy changes and corporate tax discussions, which could impact business confidence and growth. The path forward holds both optimism and caution as new policies take shape.

Want to invest in winners with rock-solid fundamentals? Check out our Hidden Gem Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.