Over the past six months, KBR’s shares (currently trading at $43.33) have posted a disappointing 12.2% loss, well below the S&P 500’s 6.6% gain. This might have investors contemplating their next move.

Following the drawdown, is this a buying opportunity for KBR? Find out in our full research report, it’s free.

Why Does KBR Spark Debate?

Known for projects like the construction of Guantanamo Bay, KBR provides professional services and technologies, specializing in engineering, construction, and government services sectors.

Two Things to Like:

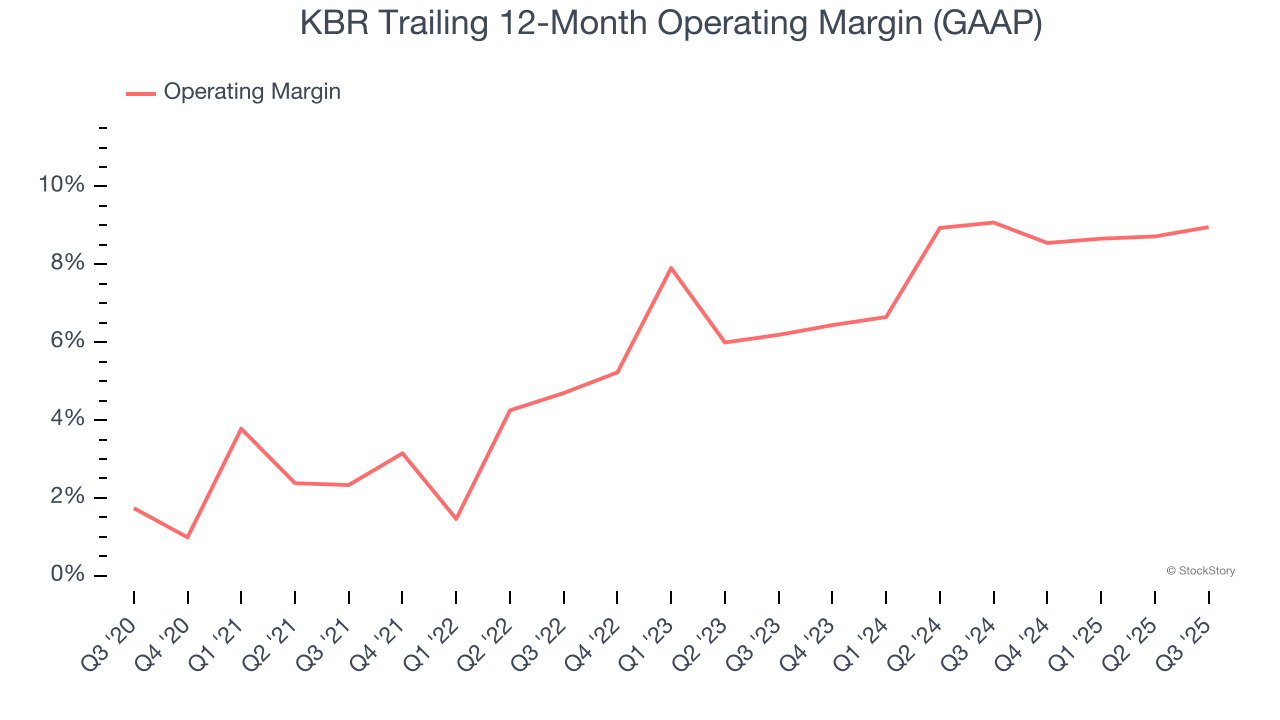

1. Operating Margin Rising, Profits Up

Operating margin is a key measure of profitability. Think of it as net income - the bottom line - excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

KBR’s operating margin rose by 6.6 percentage points over the last five years, as its sales growth gave it operating leverage. Its operating margin for the trailing 12 months was 9%.

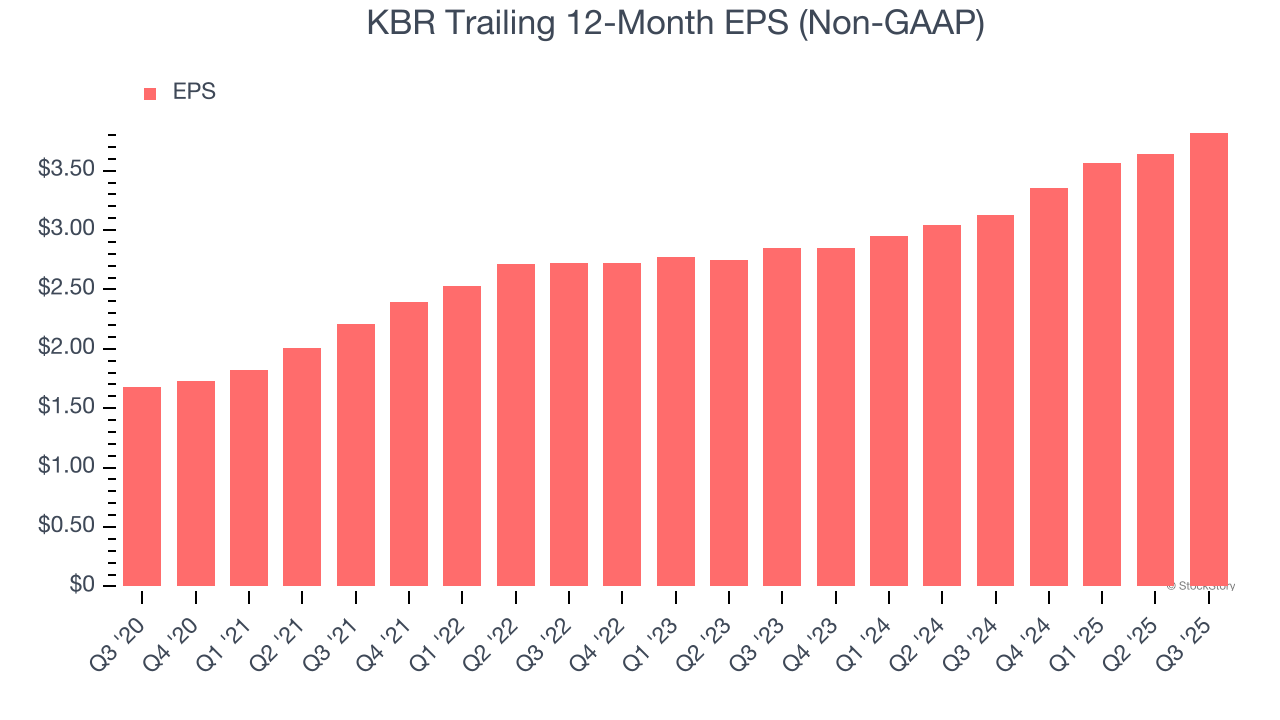

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

KBR’s EPS grew at an astounding 17.9% compounded annual growth rate over the last five years, higher than its 7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

One Reason to be Careful:

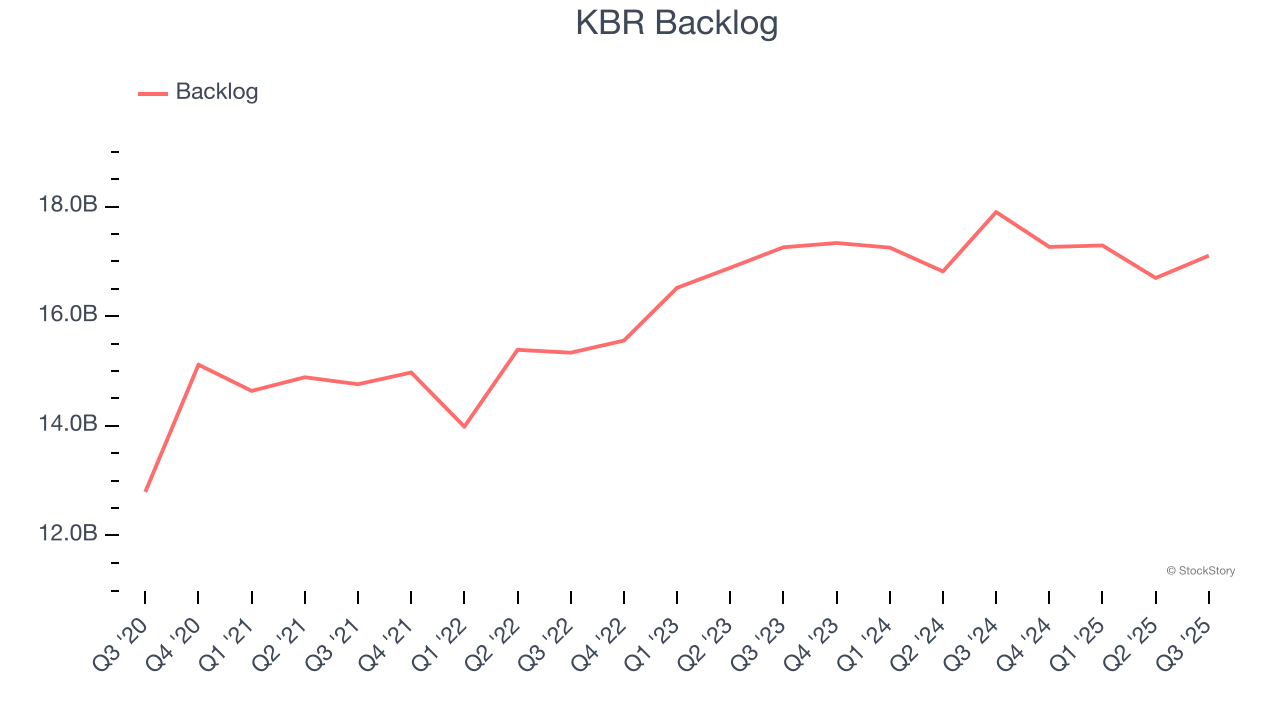

Weak Backlog Growth Points to Soft Demand

We can better understand Defense Contractors companies by analyzing their backlog. This metric shows the value of outstanding orders that have not yet been executed or delivered, giving visibility into KBR’s future revenue streams.

KBR’s backlog came in at $17.1 billion in the latest quarter, and over the last two years, its year-on-year growth averaged 1.7%. This performance was underwhelming and suggests that increasing competition is causing challenges in winning new orders.

Final Judgment

KBR’s positive characteristics outweigh the negatives. With the recent decline, the stock trades at 10.7× forward P/E (or $43.33 per share). Is now a good time to initiate a position? See for yourself in our comprehensive research report, it’s free.

High-Quality Stocks for All Market Conditions

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 5 Growth Stocks for this month. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.