Annaly Capital Management trades at $22.31 per share and has stayed right on track with the overall market, gaining 14.5% over the last six months. At the same time, the S&P 500 has returned 13.9%.

Is now the time to buy Annaly Capital Management, or should you be careful about including it in your portfolio? See what our analysts have to say in our full research report, it’s free for active Edge members.

Why Do We Think Annaly Capital Management Will Underperform?

We're sitting this one out for now. Here are three reasons there are better opportunities than NLY and a stock we'd rather own.

1. Net Interest Income Points to Soft Demand

Net interest income commands greater market attention due to its reliability and consistency, whereas one-time fees are often seen as lower-quality revenue that lacks the same dependable characteristics.

Annaly Capital Management’s net interest income has grown at a 4.7% annualized rate over the last five years, much worse than the broader banking industry.

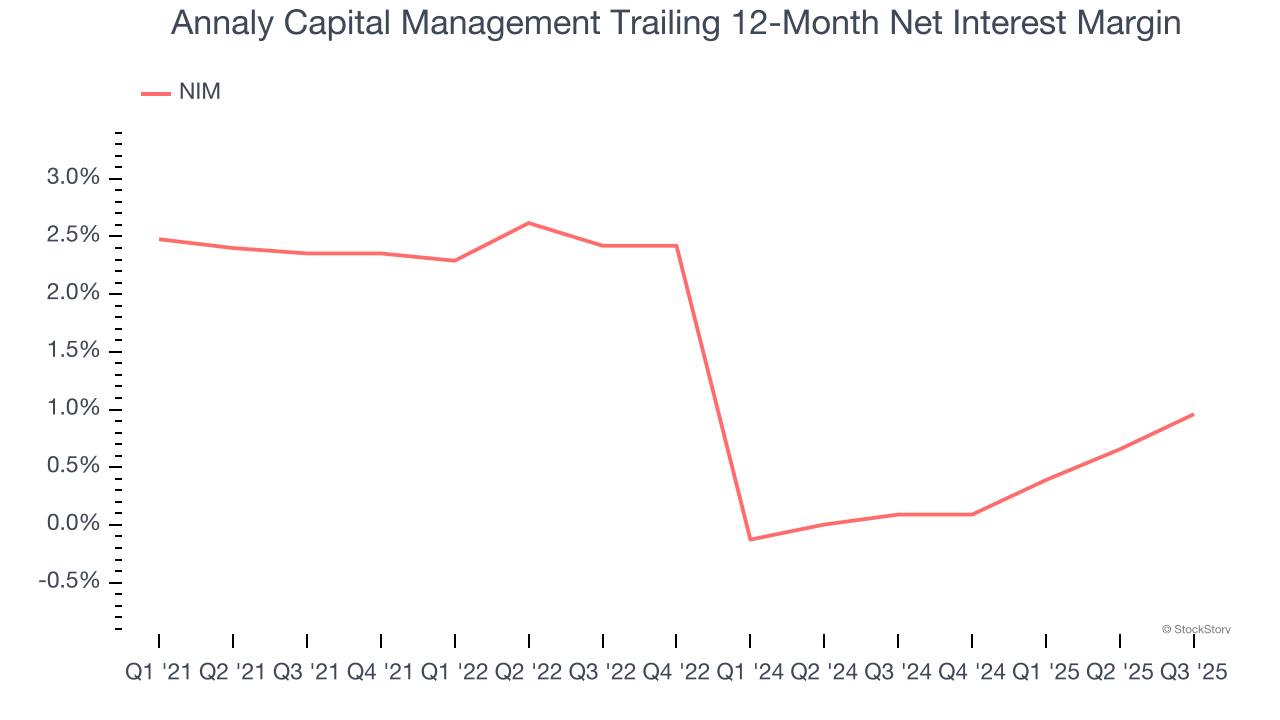

2. Low Net Interest Margin Reveals Weak Loan Book Profitability

Net interest margin (NIM) serves as a critical gauge of a bank's fundamental profitability by showing the spread between interest income and interest expenses. It's essential for understanding whether a firm can sustainably generate returns from its lending operations.

Over the past two years, we can see that Annaly Capital Management’s net interest margin averaged a poor breakeven, reflecting its high servicing and capital costs.

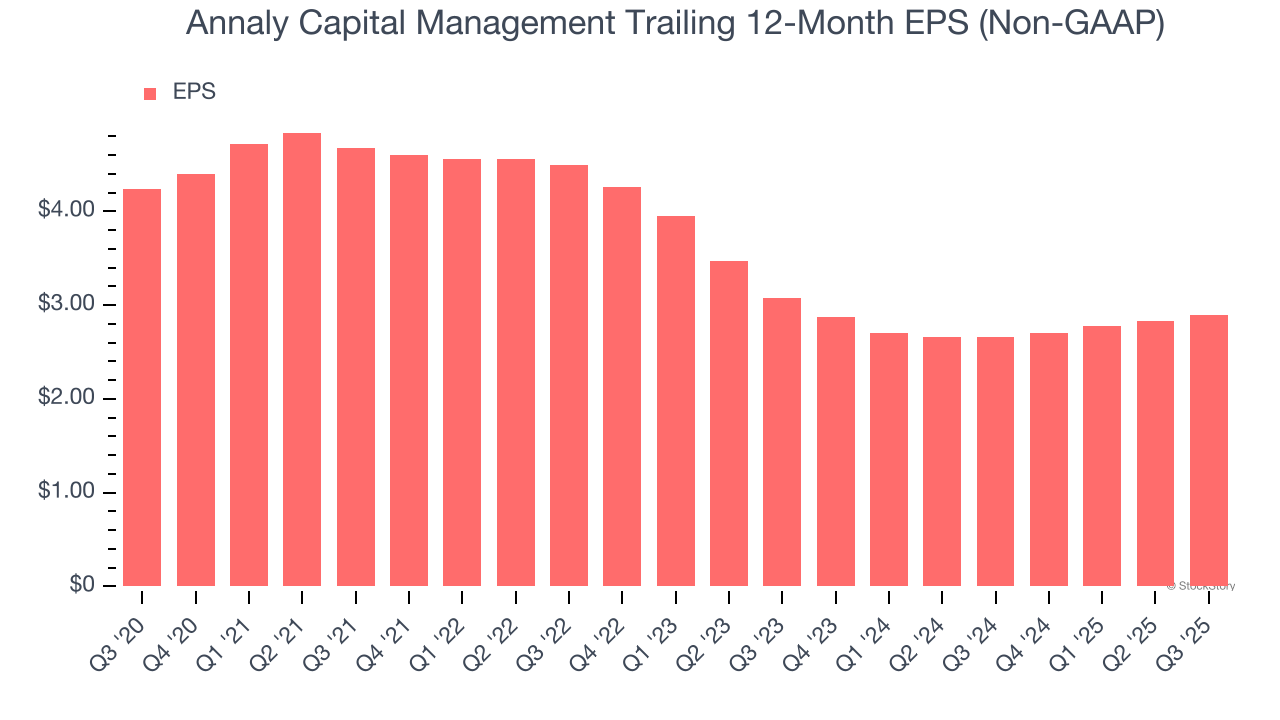

3. EPS Trending Down

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Sadly for Annaly Capital Management, its EPS and revenue declined by 7.3% and 22% annually over the last five years. We tend to steer our readers away from companies with falling revenue and EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Annaly Capital Management’s low margin of safety could leave its stock price susceptible to large downswings.

Final Judgment

We cheer for all companies supporting the economy, but in the case of Annaly Capital Management, we’ll be cheering from the sidelines. That said, the stock currently trades at 1.1× forward P/B (or $22.31 per share). This valuation tells us it’s a bit of a market darling with a lot of good news priced in - we think there are better stocks to buy right now. We’d recommend looking at one of our top digital advertising picks.

Stocks We Would Buy Instead of Annaly Capital Management

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Comfort Systems (+782% five-year return). Find your next big winner with StockStory today.

StockStory is growing and hiring equity analyst and marketing roles. Are you a 0 to 1 builder passionate about the markets and AI? See the open roles here.