Piper Sandler currently trades at $350.19 and has been a dream stock for shareholders. It’s returned 246% since December 2020, nearly tripling the S&P 500’s 84.9% gain. The company has also beaten the index over the past six months as its stock price is up 27.7% thanks to its solid quarterly results.

Is it too late to buy PIPR? Find out in our full research report, it’s free for active Edge members.

Why Are We Positive On Piper Sandler?

Tracing its roots back to 1895 and rebranded from Piper Jaffray in 2020, Piper Sandler (NYSE:PIPR) is an investment bank that provides advisory services, capital raising, institutional brokerage, and research for corporations, governments, and institutional investors.

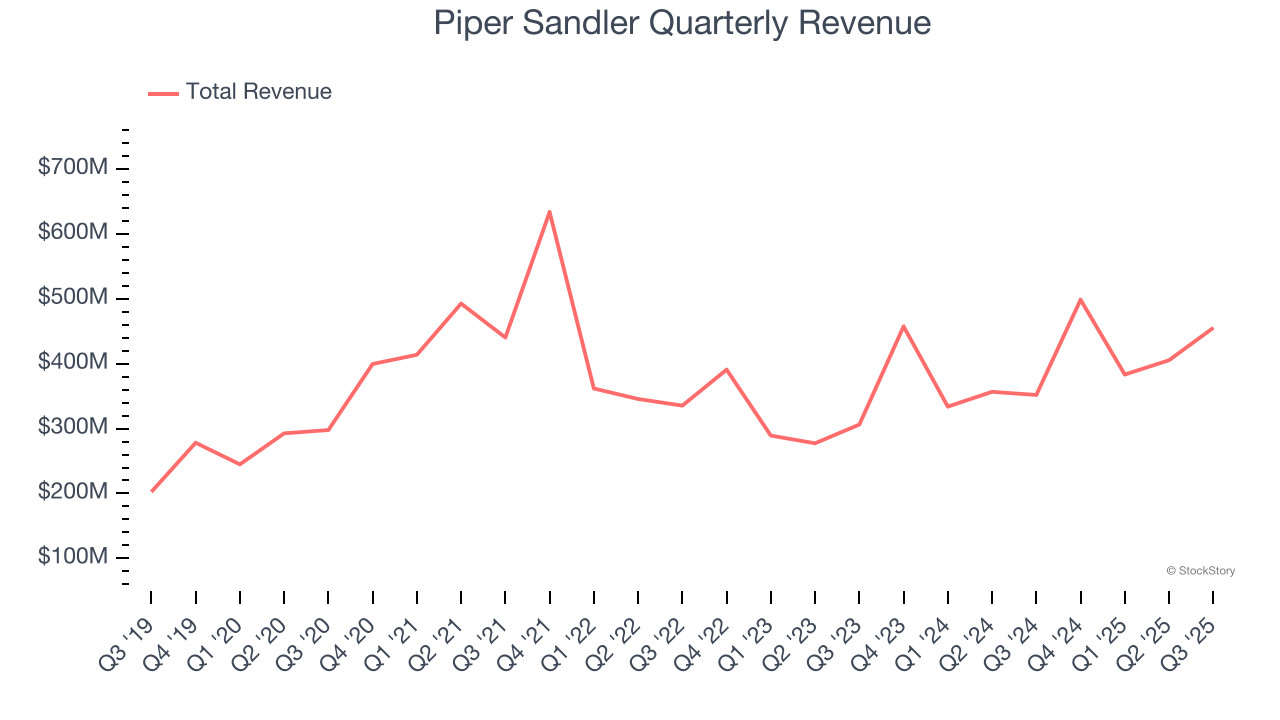

1. Long-Term Revenue Growth Shows Momentum

A company’s long-term performance is an indicator of its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul.

Thankfully, Piper Sandler’s 9.4% annualized revenue growth over the last five years was decent. Its growth was slightly above the average financials company and shows its offerings resonate with customers.

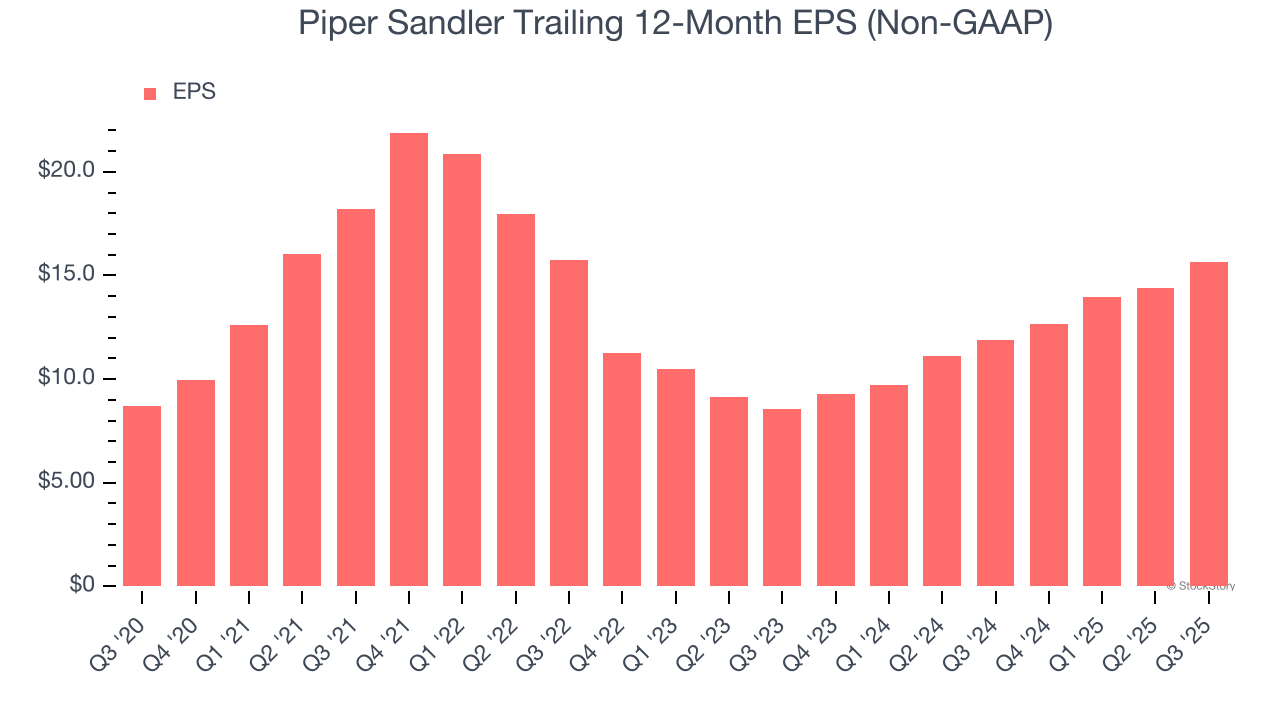

2. EPS Moving Up Steadily

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

Piper Sandler’s EPS grew at a decent 12.5% compounded annual growth rate over the last five years, higher than its 9.4% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

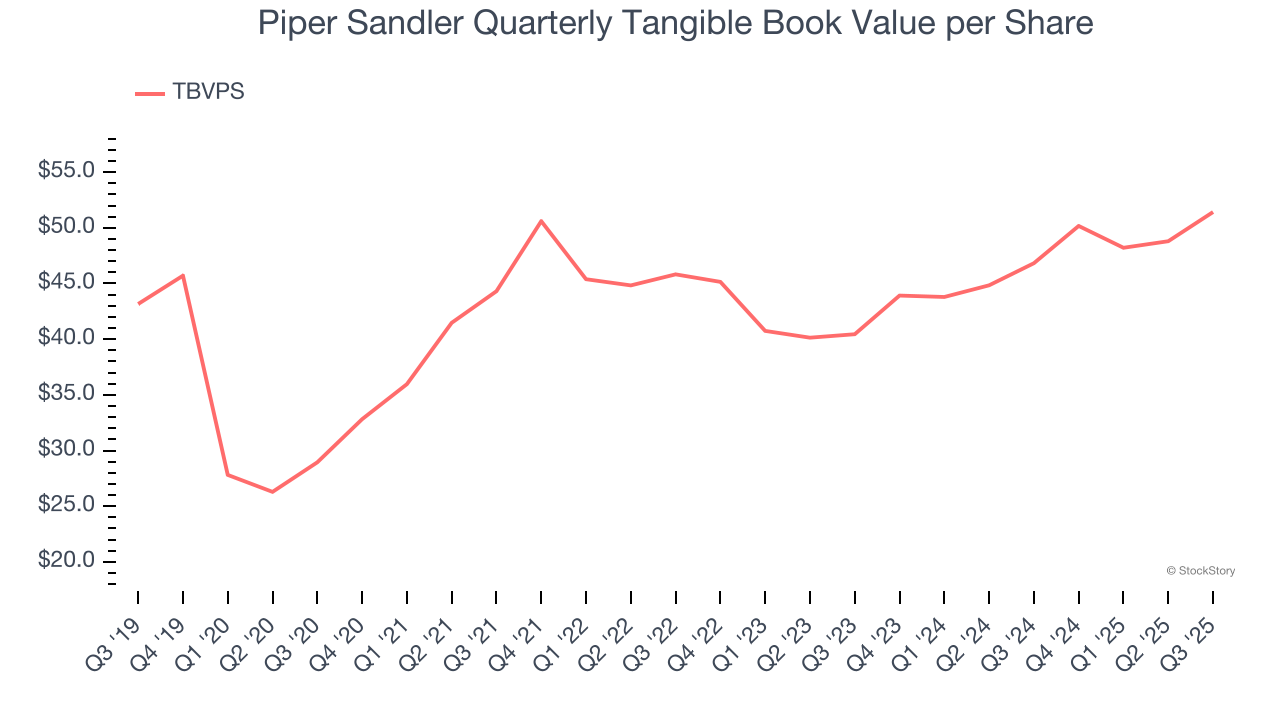

3. Growing TBVPS Reflects Strong Asset Base

Tangible book value per share (TBVPS) is a crucial metric that measures the actual value of shareholders’ equity, stripping out goodwill and other intangible assets that may not be recoverable in a worst-case scenario.

Piper Sandler’s TBVPS increased by 12.2% annually over the last five years, and the past two years show a similar trajectory as TBVPS grew at an impressive 12.8% annual clip (from $40.45 to $51.42 per share).

Final Judgment

These are just a few reasons why we think Piper Sandler is a high-quality business, and with its shares beating the market recently, the stock trades at 20.1× forward P/E (or $350.19 per share). Is now the time to initiate a position? See for yourself in our full research report, it’s free for active Edge members.

Stocks We Like Even More Than Piper Sandler

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.