Since July 2025, ResMed has been in a holding pattern, floating around $254.41. The stock also fell short of the S&P 500’s 11.3% gain during that period.

Is now the time to buy RMD? Find out in our full research report, it’s free.

Why Do Investors Watch RMD Stock?

Founded in 1989 to address the then-underdiagnosed condition of sleep apnea, ResMed (NYSE:RMD) develops cloud-connected medical devices and software solutions that treat sleep apnea, COPD, and other respiratory disorders for home and clinical use.

Three Things to Like:

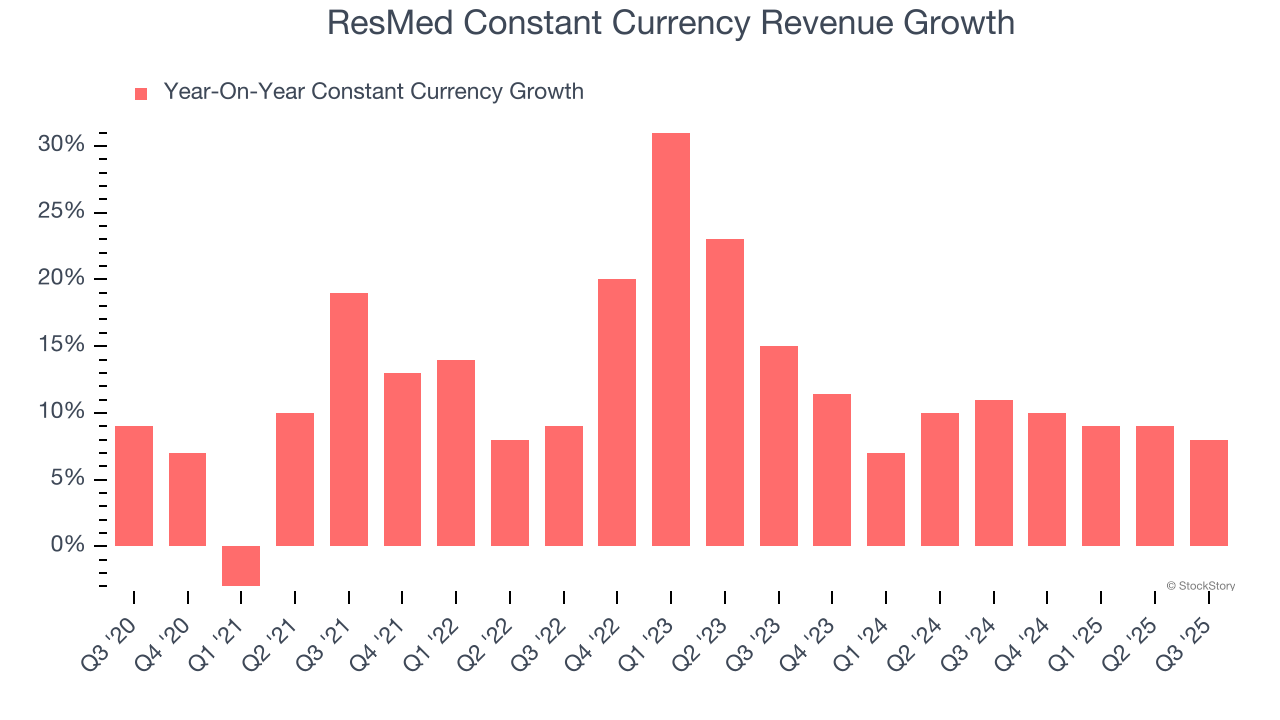

1. Constant Currency Revenue Drives Growth

In addition to reported revenue, constant currency revenue is a useful data point for analyzing Patient Monitoring companies. This metric excludes currency movements, which are outside of ResMed’s control and are not indicative of underlying demand.

Over the last two years, ResMed’s constant currency revenue averaged 9.4% year-on-year growth. This performance was solid and shows it can expand steadily on a global scale regardless of the macroeconomic environment.

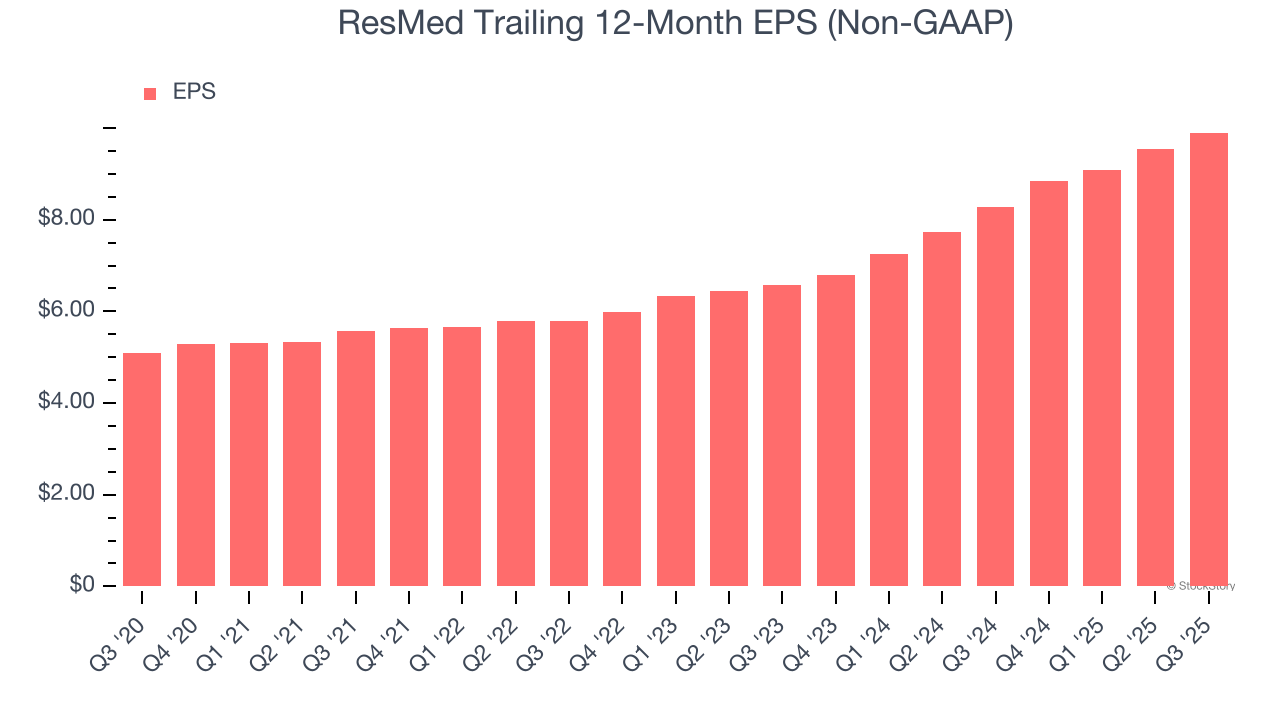

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

ResMed’s EPS grew at a spectacular 14.2% compounded annual growth rate over the last five years, higher than its 11.7% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

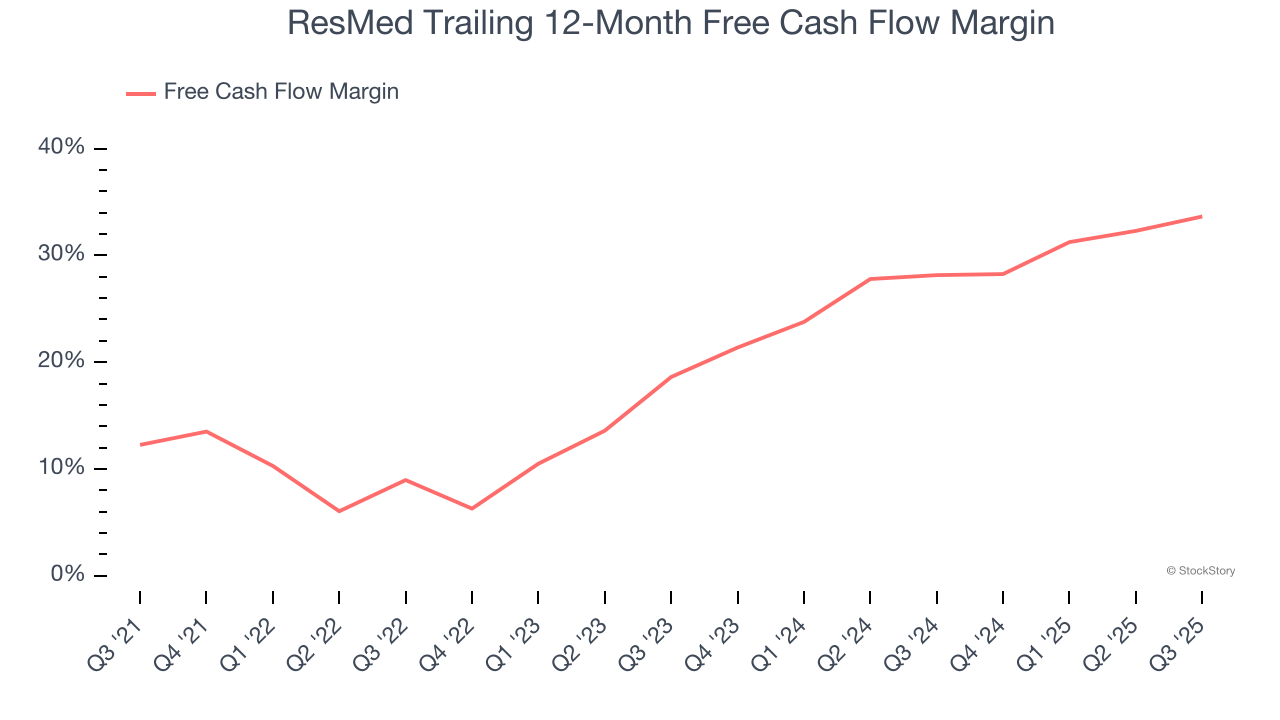

3. Increasing Free Cash Flow Margin Juices Financials

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

As you can see below, ResMed’s margin expanded by 21.4 percentage points over the last five years. This is encouraging, and we can see it became a less capital-intensive business because its free cash flow profitability rose more than its operating profitability. ResMed’s free cash flow margin for the trailing 12 months was 33.6%.

Final Judgment

There are definitely things to like about ResMed. With its shares underperforming the market lately, the stock trades at 23× forward P/E (or $254.41 per share). Is now a good time to buy? See for yourself in our in-depth research report, it’s free.

Stocks We Like Even More Than ResMed

If your portfolio success hinges on just 4 stocks, your wealth is built on fragile ground. You have a small window to secure high-quality assets before the market widens and these prices disappear.

Don’t wait for the next volatility shock. Check out our Top 5 Strong Momentum Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Tecnoglass (+1,754% five-year return). Find your next big winner with StockStory today.