The Hanover Insurance Group has been treading water for the past six months, recording a small return of 4.5% while holding steady at $170.68. The stock also fell short of the S&P 500’s 11.5% gain during that period.

Is there a buying opportunity in The Hanover Insurance Group, or does it present a risk to your portfolio? Dive into our full research report to see our analyst team’s opinion, it’s free.

Why Is The Hanover Insurance Group Not Exciting?

We don't have much confidence in The Hanover Insurance Group. Here are three reasons we avoid THG and a stock we'd rather own.

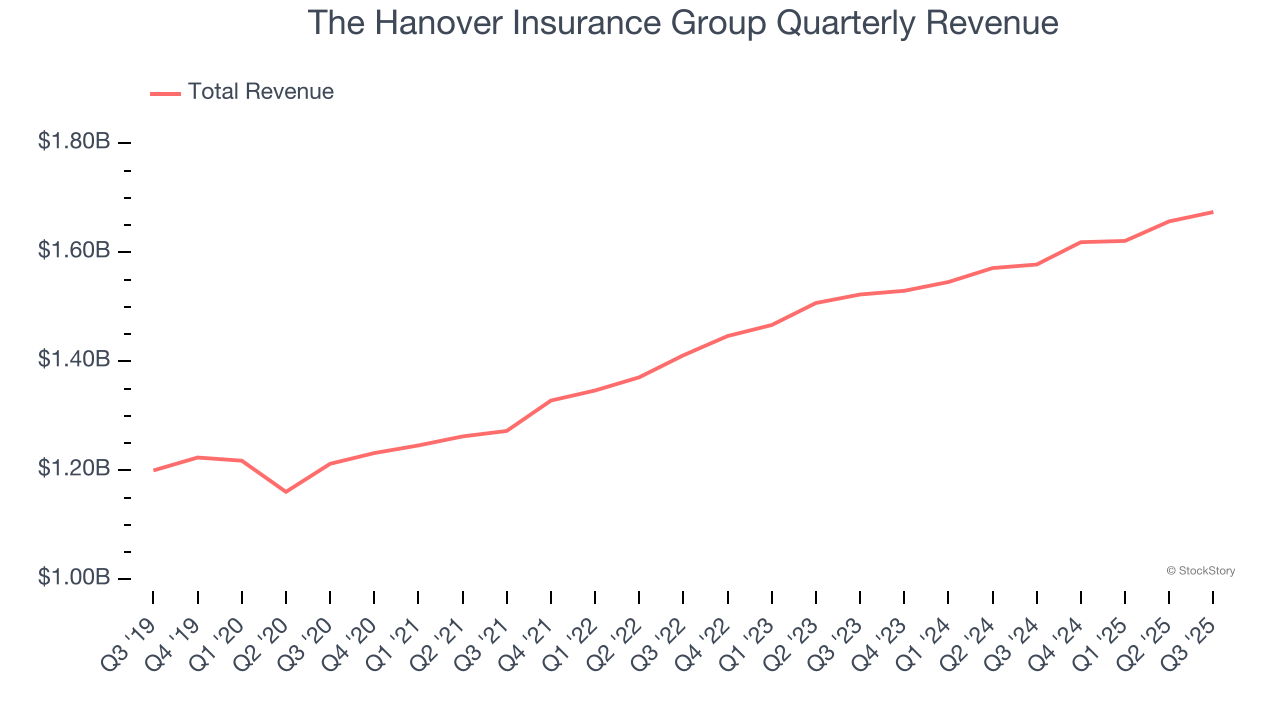

1. Long-Term Revenue Growth Disappoints

In general, insurance companies earn revenue from three primary sources. The first is the core insurance business itself, often called underwriting and represented in the income statement as premiums earned. The second source is investment income from investing the “float” (premiums collected upfront not yet paid out as claims) in assets such as fixed-income assets and equities. The third is fees from various sources such as policy administration, annuities, or other value-added services.

Over the last five years, The Hanover Insurance Group grew its revenue at a mediocre 6.4% compounded annual growth rate. This fell short of our benchmark for the insurance sector.

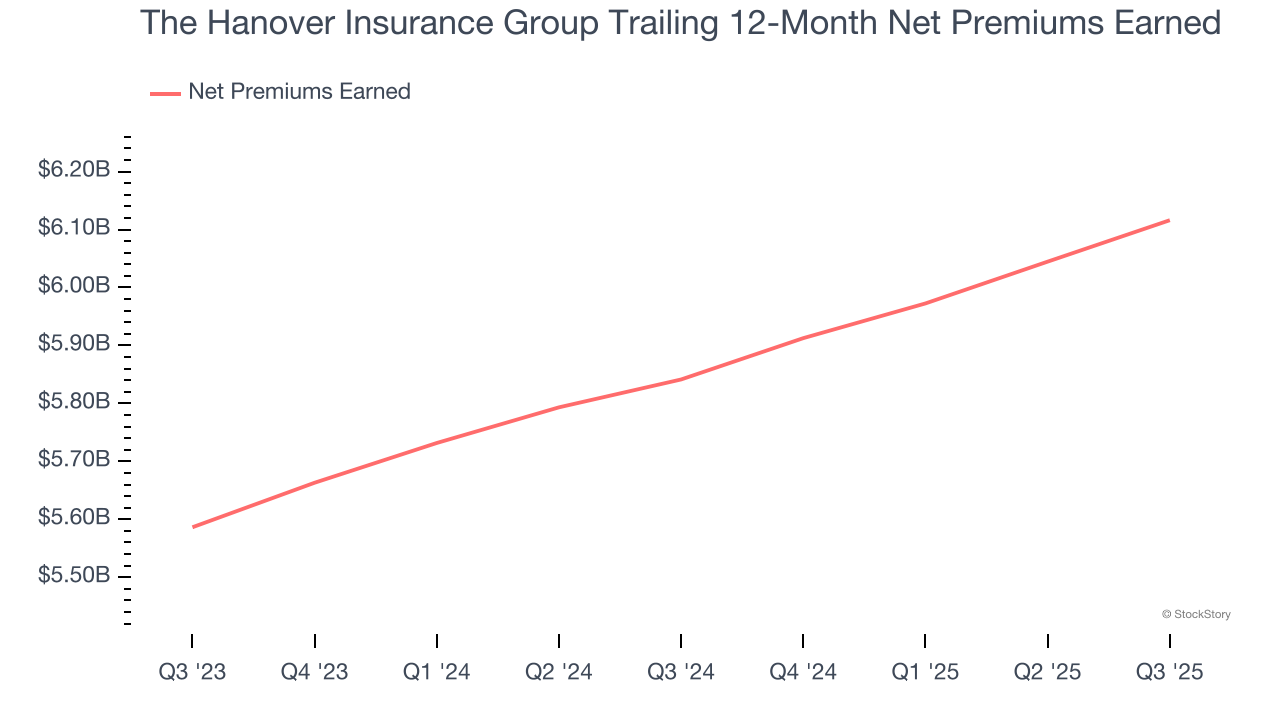

2. Net Premiums Earned Point to Soft Demand

When insurers sell policies, they protect themselves from extremely large losses or an outsized accumulation of losses with reinsurance (insurance for insurance companies). Net premiums earned are:

- Gross premiums - what’s ceded to reinsurers as a risk mitigation and transfer strategy

The Hanover Insurance Group’s net premiums earned has grown at a 4.6% annualized rate over the last two years, worse than the broader insurance industry and in line with its total revenue.

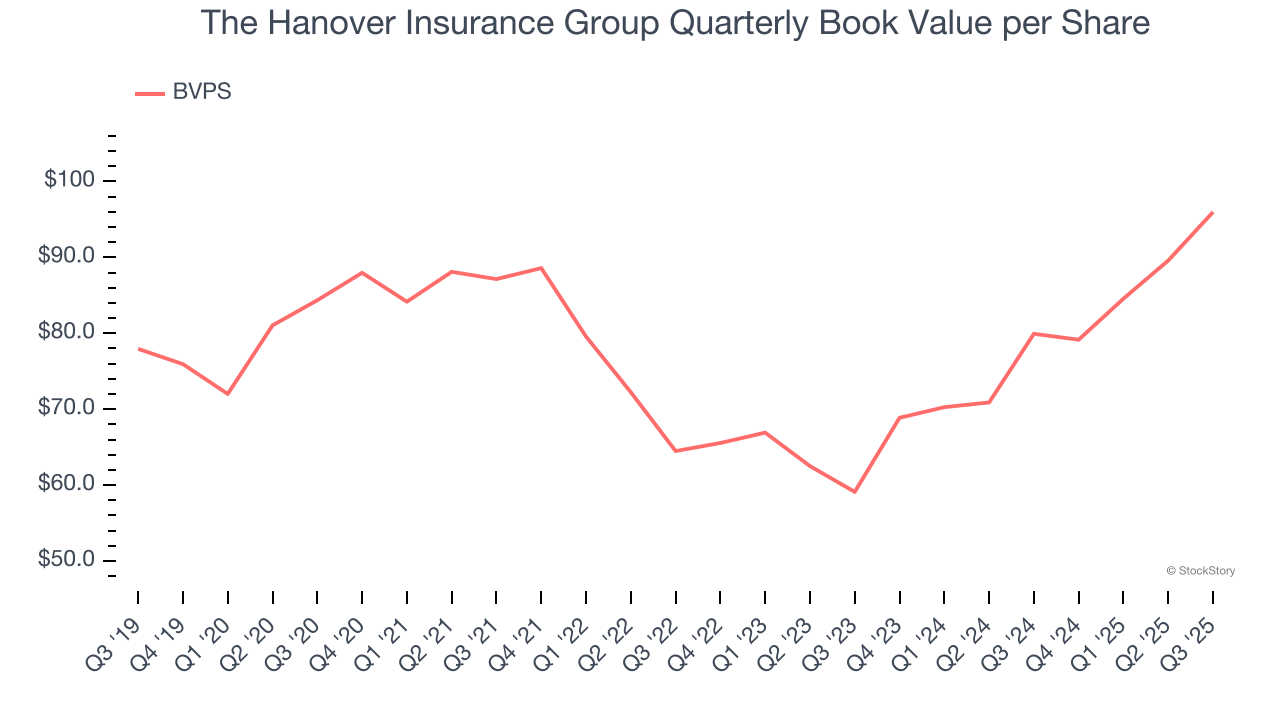

3. Growing BVPS Reflects Strong Asset Base

Book value per share (BVPS) serves as a key indicator of an insurer’s financial stability, reflecting a company’s ability to maintain adequate capital levels and meet its long-term obligations to policyholders.

Although The Hanover Insurance Group’s BVPS increased by a meager 2.6% annually over the last five years, the good news is that its growth has recently accelerated as BVPS grew at an incredible 27.4% annual clip over the past two years (from $59.11 to $95.97 per share).

Final Judgment

The Hanover Insurance Group isn’t a terrible business, but it doesn’t pass our bar. With its shares underperforming the market lately, the stock trades at 1.7× forward P/B (or $170.68 per share). This valuation is reasonable, but the company’s shakier fundamentals present too much downside risk. We're pretty confident there are superior stocks to buy right now. We’d suggest looking at the Amazon and PayPal of Latin America.

Stocks We Like More Than The Hanover Insurance Group

Check out the high-quality names we’ve flagged in our Top 6 Stocks for this week. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.