As the Q3 earnings season comes to a close, it’s time to take stock of this quarter’s best and worst performers in the research tools & consumables industry, including Waters Corporation (NYSE:WAT) and its peers.

The life sciences subsector specializing in research tools and consumables enables scientific discoveries across academia, biotechnology, and pharmaceuticals. These firms supply a wide range of essential laboratory products, ensuring a recurring revenue stream through repeat purchases and replenishment. Their business models benefit from strong customer loyalty, a diversified product portfolio, and exposure to both the research and clinical markets. However, challenges include high R&D investment to maintain technological leadership, pricing pressures from budget-conscious institutions, and vulnerability to fluctuations in research funding cycles. Looking ahead, this subsector stands to benefit from tailwinds such as growing demand for tools supporting emerging fields like synthetic biology and personalized medicine. There is also a rise in automation and AI-driven solutions in laboratories that could create new opportunities to sell tools and consumables. Nevertheless, headwinds exist. These companies tend to be at the mercy of supply chain disruptions and sensitivity to macroeconomic conditions that impact funding for research initiatives.

The 10 research tools & consumables stocks we track reported a mixed Q3. As a group, revenues beat analysts’ consensus estimates by 1.1% while next quarter’s revenue guidance was 1.3% below.

While some research tools & consumables stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 1.5% since the latest earnings results.

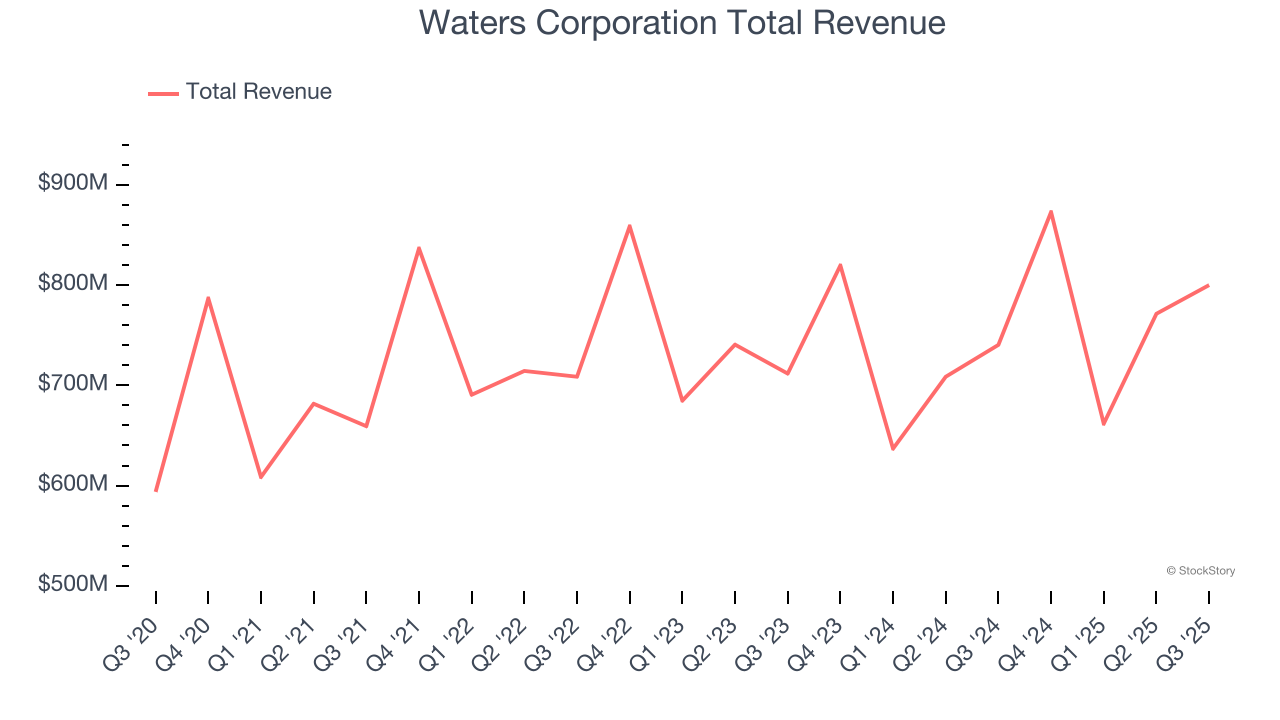

Waters Corporation (NYSE:WAT)

Founded in 1958 and pioneering innovations in laboratory analysis for over six decades, Waters (NYSE:WAT) develops and manufactures analytical instruments, software, and consumables for liquid chromatography, mass spectrometry, and thermal analysis used in scientific research and quality testing.

Waters Corporation reported revenues of $799.9 million, up 8% year on year. This print exceeded analysts’ expectations by 2.4%. Overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ organic revenue estimates but a miss of analysts’ EPS guidance for next quarter estimates.

"Our team yet again delivered outstanding results, driven by strong execution and our differentiated product portfolio. Pharma grew double digits as the instrument replacement cycle entered its second year, and new LC-MS and chemistry products captured opportunities from the growing share of biologics and novel modalities in the pharma pipeline," said Dr. Udit Batra, President & CEO of Waters Corporation.

Interestingly, the stock is up 8.9% since reporting and currently trades at $376.31.

Is now the time to buy Waters Corporation? Access our full analysis of the earnings results here, it’s free for active Edge members.

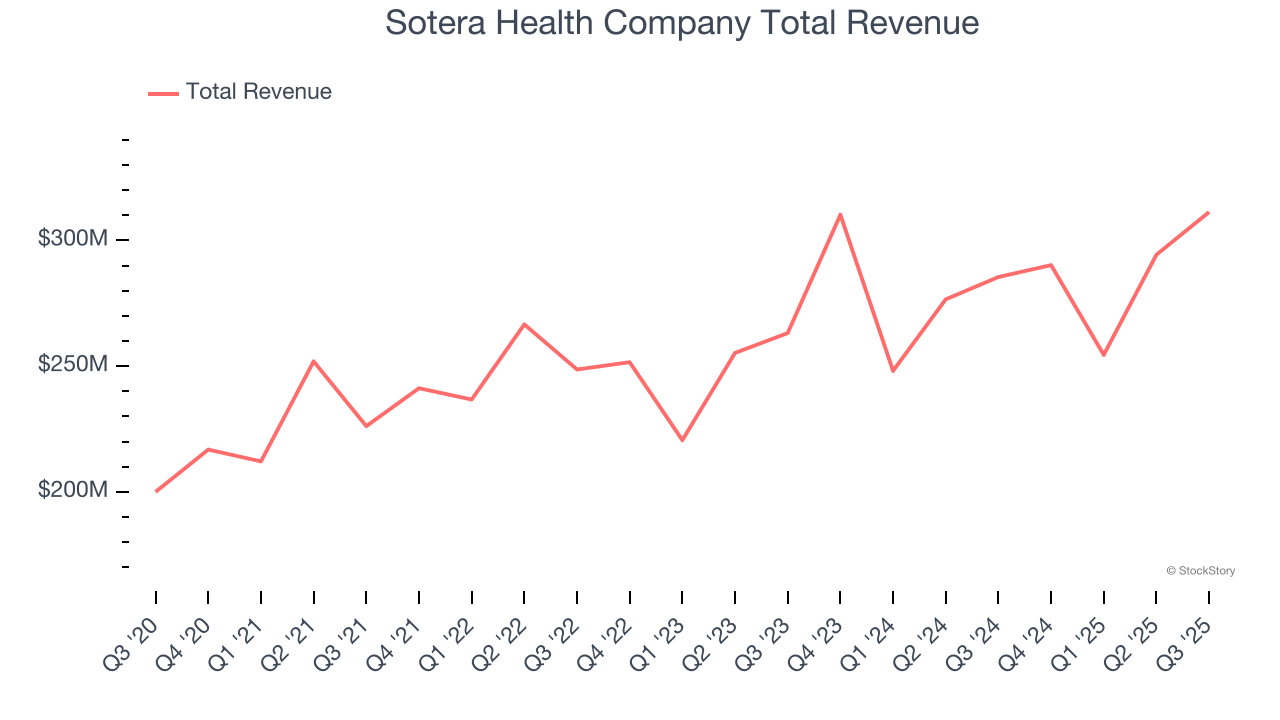

Best Q3: Sotera Health Company (NASDAQ:SHC)

With a critical role in ensuring the safety of millions of patients worldwide, Sotera Health (NASDAQGS:SHC) provides sterilization services, lab testing, and advisory services to ensure medical devices, pharmaceuticals, and food products are safe for use.

Sotera Health Company reported revenues of $311.3 million, up 9.1% year on year, outperforming analysts’ expectations by 2.6%. The business had an exceptional quarter with an impressive beat of analysts’ full-year EPS guidance estimates and an impressive beat of analysts’ organic revenue estimates.

The market seems content with the results as the stock is up 3% since reporting. It currently trades at $17.10.

Is now the time to buy Sotera Health Company? Access our full analysis of the earnings results here, it’s free for active Edge members.

Weakest Q3: Avantor (NYSE:AVTR)

With roots dating back to 1904 and embedded in virtually every stage of scientific research and production, Avantor (NYSE:AVTR) provides mission-critical products, materials, and services to customers in biopharma, healthcare, education, and advanced technology industries.

Avantor reported revenues of $1.62 billion, down 5.3% year on year, falling short of analysts’ expectations by 1.4%. It was a softer quarter as it posted a slight miss of analysts’ revenue estimates.

Avantor delivered the slowest revenue growth in the group. As expected, the stock is down 26.6% since the results and currently trades at $11.08.

Read our full analysis of Avantor’s results here.

Revvity (NYSE:RVTY)

Formerly known as PerkinElmer until its rebranding in 2023, Revvity (NYSE:RVTY) provides health science technologies and services that support the complete workflow from discovery to development and diagnosis to cure.

Revvity reported revenues of $698.9 million, up 2.2% year on year. This print met analysts’ expectations. Aside from that, it was a satisfactory quarter as it also produced a decent beat of analysts’ full-year EPS guidance estimates but organic revenue in line with analysts’ estimates.

Revvity achieved the highest full-year guidance raise among its peers. The stock is down 2.6% since reporting and currently trades at $96.35.

Read our full, actionable report on Revvity here, it’s free for active Edge members.

Mettler-Toledo (NYSE:MTD)

With roots dating back to the precision balance innovations of Swiss engineer Erhard Mettler, Mettler-Toledo (NYSE:MTD) manufactures precision weighing instruments, analytical equipment, and product inspection systems used in laboratories, industrial settings, and food retail.

Mettler-Toledo reported revenues of $1.03 billion, up 7.9% year on year. This result surpassed analysts’ expectations by 3.2%. Taking a step back, it was a mixed quarter as it also recorded a solid beat of analysts’ revenue estimates but revenue guidance for next quarter missing analysts’ expectations significantly.

Mettler-Toledo delivered the biggest analyst estimates beat among its peers. The stock is down 3.5% since reporting and currently trades at $1,390.

Read our full, actionable report on Mettler-Toledo here, it’s free for active Edge members.

Market Update

As a result of the Fed’s rate hikes in 2022 and 2023, inflation has come down from frothy levels post-pandemic. The general rise in the price of goods and services is trending towards the Fed’s 2% goal as of late, which is good news. The higher rates that fought inflation also didn't slow economic activity enough to catalyze a recession. So far, soft landing. This, combined with recent rate cuts (half a percent in September 2024 and a quarter percent in November 2024) have led to strong stock market performance in 2024. The icing on the cake for 2024 returns was Donald Trump’s victory in the U.S. Presidential Election in early November, sending major indices to all-time highs in the week following the election. Still, debates around the health of the economy and the impact of potential tariffs and corporate tax cuts remain, leaving much uncertainty around 2025.

Want to invest in winners with rock-solid fundamentals? Check out our 9 Best Market-Beating Stocks and add them to your watchlist. These companies are poised for growth regardless of the political or macroeconomic climate.

StockStory’s analyst team — all seasoned professional investors — uses quantitative analysis and automation to deliver market-beating insights faster and with higher quality.