What a brutal six months it’s been for Wiley. The stock has dropped 23.3% and now trades at $29.07, rattling many shareholders. This might have investors contemplating their next move.

Is now the time to buy Wiley, or should you be careful about including it in your portfolio? Get the full stock story straight from our expert analysts, it’s free.

Why Do We Think Wiley Will Underperform?

Even with the cheaper entry price, we're swiping left on Wiley for now. Here are three reasons we avoid WLY and a stock we'd rather own.

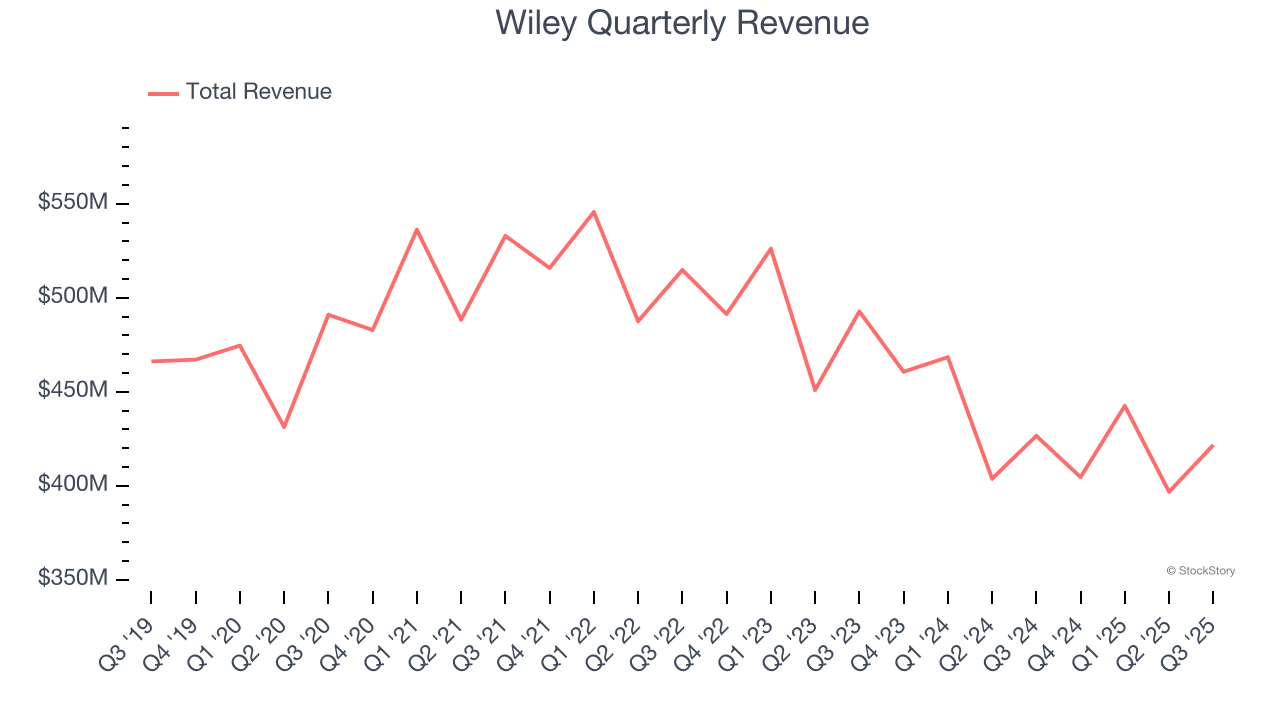

1. Revenue Spiraling Downwards

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Wiley’s demand was weak over the last five years as its sales fell at a 2.2% annual rate. This was below our standards and is a sign of poor business quality.

2. Projected Revenue Growth Shows Limited Upside

Forecasted revenues by Wall Street analysts signal a company’s potential. Predictions may not always be accurate, but accelerating growth typically boosts valuation multiples and stock prices while slowing growth does the opposite.

Over the next 12 months, sell-side analysts expect Wiley’s revenue to stall. Although this projection implies its newer products and services will catalyze better top-line performance, it is still below average for the sector.

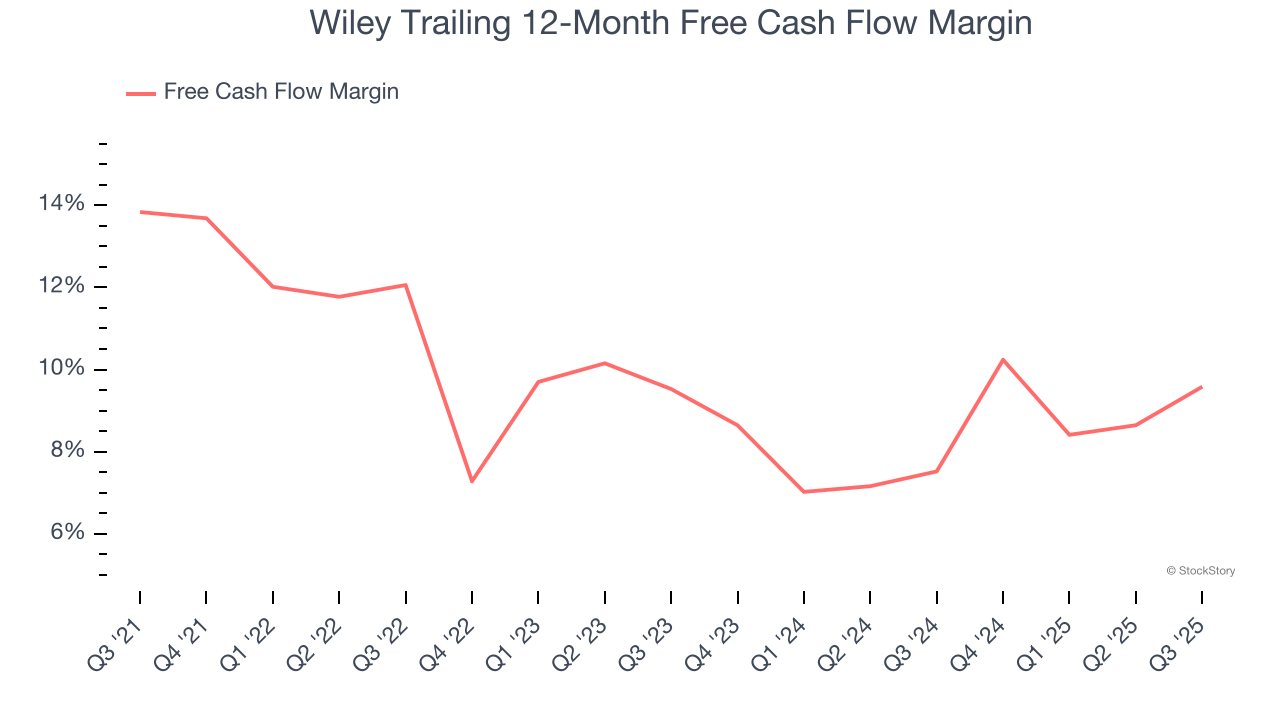

3. Free Cash Flow Margin Dropping

If you’ve followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can’t use accounting profits to pay the bills.

As you can see below, Wiley’s margin dropped by 4.3 percentage points over the last five years. It may have ticked higher more recently, but shareholders are likely hoping for its margin to at least revert to its historical level. If the longer-term trend returns, it could signal increasing investment needs and capital intensity. Wiley’s free cash flow margin for the trailing 12 months was 9.6%.

Final Judgment

Wiley falls short of our quality standards. After the recent drawdown, the stock trades at $29.07 per share (or a trailing 12-month price-to-sales ratio of 1×). The market typically values companies like Wiley based on their anticipated profits for the next 12 months, but there aren’t enough published estimates to arrive at a reliable number. You should avoid this stock for now - better opportunities lie elsewhere. We’d recommend looking at our favorite semiconductor picks and shovels play.

Stocks We Would Buy Instead of Wiley

Your portfolio can’t afford to be based on yesterday’s story. The risk in a handful of heavily crowded stocks is rising daily.

The names generating the next wave of massive growth are right here in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-small-cap company Exlservice (+354% five-year return). Find your next big winner with StockStory today.