Since July 2025, W. R. Berkley has been in a holding pattern, posting a small loss of 1.6% while floating around $69.60. The stock also fell short of the S&P 500’s 9.9% gain during that period.

Is now the time to buy WRB? Find out in our full research report, it’s free for active Edge members.

Why Are We Positive On W. R. Berkley?

Founded in 1967 and operating through more than 50 specialized insurance units across the globe, W. R. Berkley (NYSE:WRB) underwrites commercial insurance and reinsurance through specialized subsidiaries serving industries from healthcare to construction to transportation.

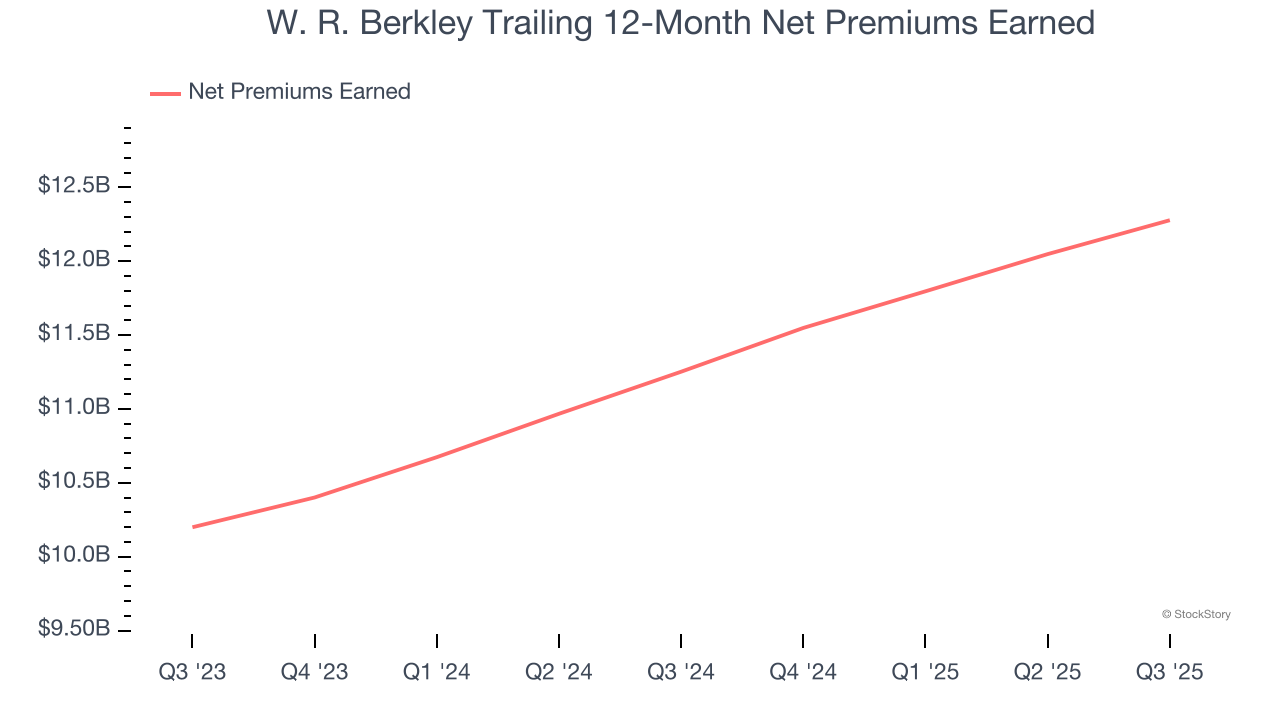

1. Net Premiums Earned Skyrocket, Fueling Growth Opportunities

Insurers sell policies then use reinsurance (insurance for insurance companies) to protect themselves from large losses. Net premiums earned are therefore what's collected from selling policies less what’s paid to reinsurers as a risk mitigation tool.

W. R. Berkley’s net premiums earned has grown at a 12.4% annualized rate over the last five years, better than the broader insurance industry.

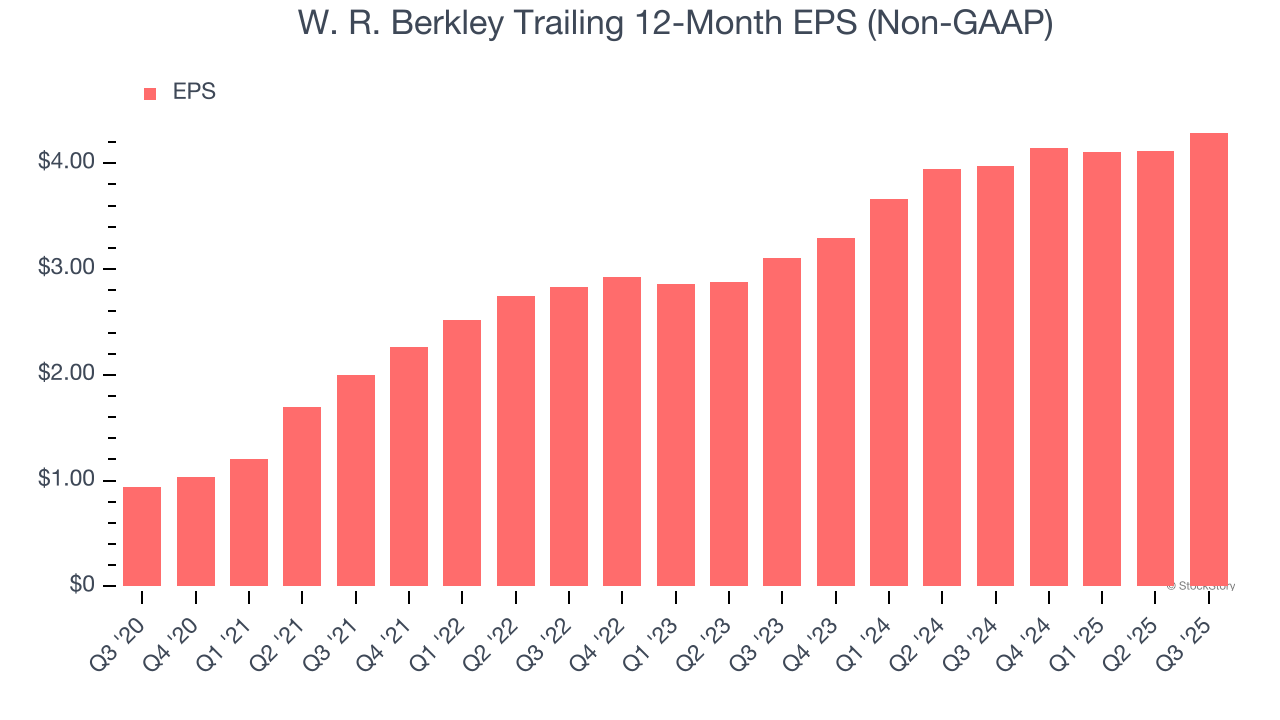

2. Outstanding Long-Term EPS Growth

We track the long-term change in earnings per share (EPS) because it highlights whether a company’s growth is profitable.

W. R. Berkley’s EPS grew at an astounding 35.5% compounded annual growth rate over the last five years, higher than its 13.6% annualized revenue growth. This tells us the company became more profitable on a per-share basis as it expanded.

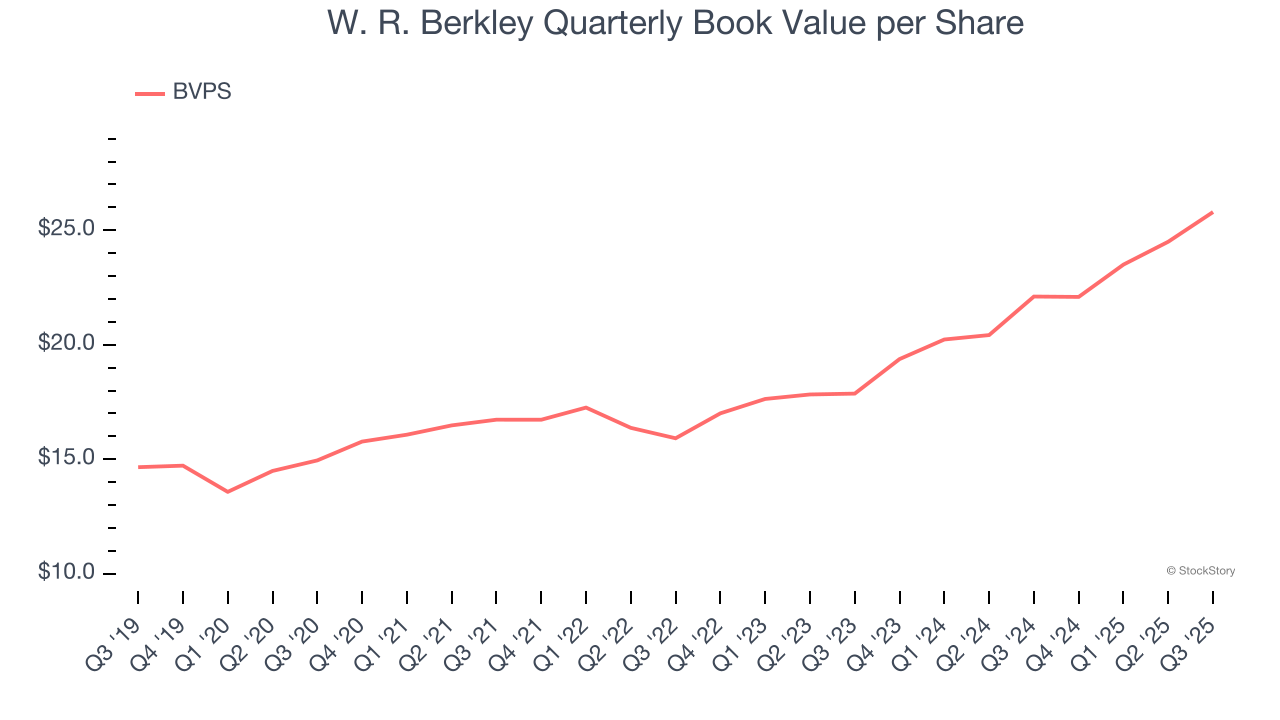

3. Projected BVPS Growth Is Remarkable

Book value per share (BVPS) growth is driven by an insurer’s ability to earn consistent underwriting profits while generating strong investment returns.

Over the next 12 months, Consensus estimates call for W. R. Berkley’s BVPS to grow by 20.3% to $27.00, elite growth rate.

Final Judgment

These are just a few reasons W. R. Berkley is a high-quality business worth owning. With its shares trailing the market in recent months, the stock trades at 2.7× forward P/B (or $69.60 per share). Is now the right time to buy? See for yourself in our full research report, it’s free for active Edge members.

Stocks We Like Even More Than W. R. Berkley

Check out the high-quality names we’ve flagged in our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 244% over the last five years (as of June 30, 2025).

Stocks that have made our list include now familiar names such as Nvidia (+1,326% between June 2020 and June 2025) as well as under-the-radar businesses like the once-micro-cap company Kadant (+351% five-year return). Find your next big winner with StockStory today.