Adobe (NASDAQ:ADBE) Q2 Sales Beat Estimates, Provides Encouraging Quarterly Guidance

Adam Hejl /

June 17, 2021

Creative software maker Adobe (NASDAQ:ADBE) reported strong growth in the Q2 FY2021 earnings announcement, with revenue up 22.6% year on year to $3.83 billion. Adobe made a GAAP profit of $1.11 billion, improving on its profit of $1.1 billion, in the same quarter last year.

What do these results signal for the future of Adobe? Get early access our full analysis here

Adobe (NASDAQ:ADBE) Q2 FY2021 Highlights:

- Revenue: $3.83 billion vs analyst estimates of $3.72 billion (2.89% beat)

- EPS (non-GAAP): $3 vs analyst estimates of $2.82 (6.49% beat)

- Revenue guidance for Q3 2021 is $3.88 billion at the midpoint, above analyst estimates of $3.83 billion

- EPS (non-GAAP) guidance for Q3 2021 is $3 at the midpoint, above analyst estimates of $2.90

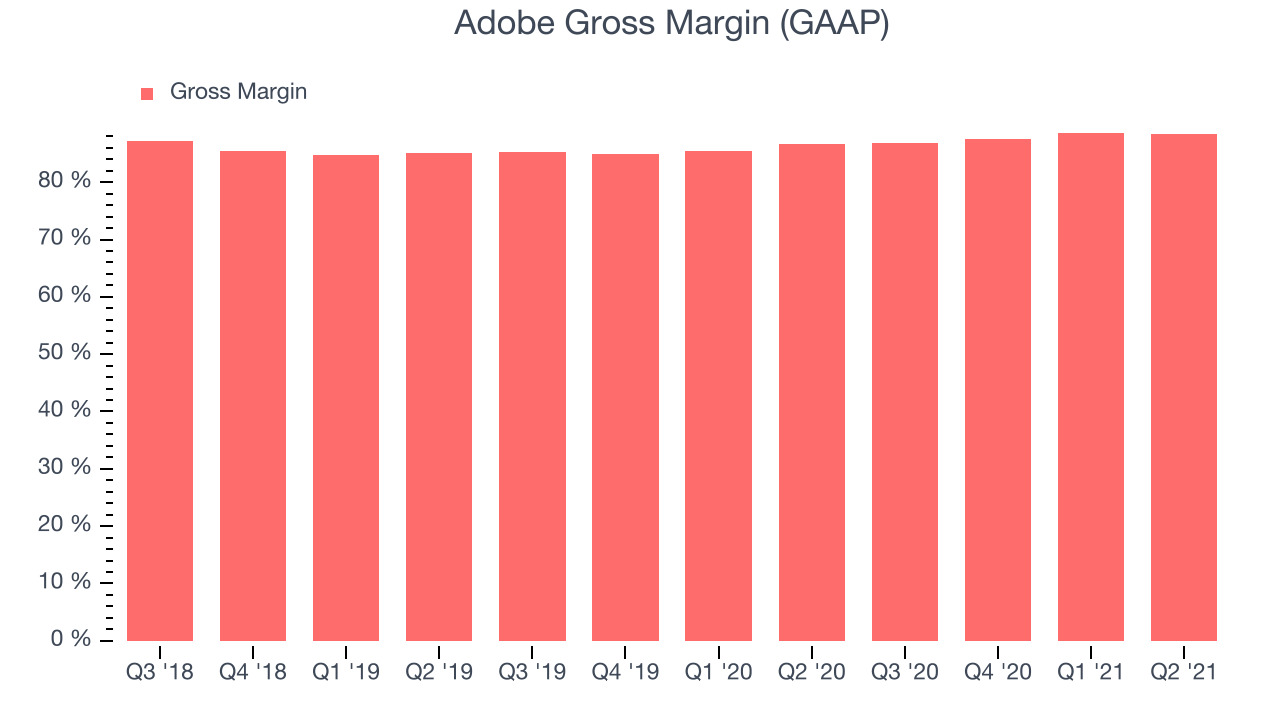

- Gross Margin (GAAP): 88.4%, in line with previous quarter

- Updated valuation: Adobe is up at $566.16 and accounting for the revenue added in Q2 it now trades at 18.4x price-to-sales (LTM), compared to 19.5x just before the results.

“Adobe had an outstanding second quarter as Creative Cloud, Document Cloud and Experience Cloud continue to transform work, learn and play in a digital-first world,” said Shantanu Narayen, president and CEO, Adobe.

Adobe: Creativity For All

One of the most well-known Silicon Valley software companies around, Adobe (ADBE) was originally founded in 1982 and famously Steve Jobs soon after attempted to acquire it for $5 million. The founders refused and instead negotiated an investment and a five year licencing deal with Apple (AAPL), which made them the first company in the history of Silicon Value to turn profit in its first year and started their impressive journey.

Adobe (ADBE) is a leading provider of software as service in the digital design and document management space. The company is famous for inventing the PDF format and its photo-editing and publishing software products like Photoshop or Illustrator which have become household names and leading industry standards. Over time Adobe leveraged the key role their products played in the lives of their customers and built a cloud ecosystem of products and services around them.

Today the company has a very strong portfolio of products, through its Creative Cloud offering it provides tools for digital design and publishing, such as Adobe Premiere that is used for professional movie production. The Document Cloud enables customers to create electronic documents and manage their lifecycle, offering the ability to sign legally binding documents electronically through Adobe Sign. Lately Adobe has been expanding into offering software for hosting content online and providing customers with the ability to monetize their readers via advertising.

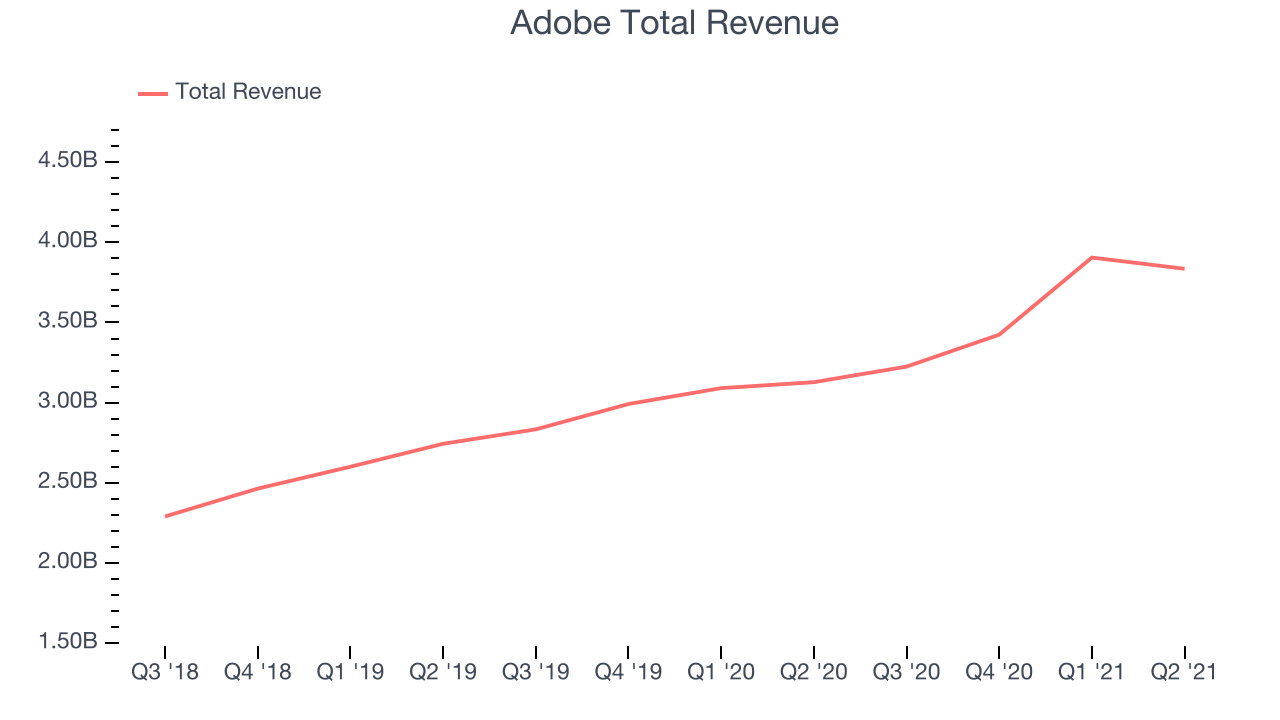

Sales Growth

As you can see below, Adobe's revenue growth has been decent over the last twelve months, growing from $3.12 billion to $3.83 billion.

This quarter, Adobe's quarterly revenue was once again up a very solid 22.6% year on year. But the growth did slow down compared to last quarter, as the revenue decreased by $70 million in Q2, compared to $481 million in Q1 2021. A one-off fluctuation is usually not concerning, but it is worth keeping in mind.

There are others doing even better. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 80% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

Profitability

Adobe successfully reinvented itself around 2012 when it switched from selling its software on CDs with a one-off licence to a subscription based software as a service model. What makes the cloud business model so attractive is that once the software is developed, it typically shouldn't cost much to provide it as an ongoing service to customers.

Adobe's gross profit margin, an important metric measuring how much money there is left after paying for servers, licences, technical support and other necessary running expenses was at 88.4% in Q2. That means that for every $1 in revenue the company had $0.88 left to spend on developing new products, marketing & sales and the general administrative overhead. This is a great gross margin, that allows companies like Adobe to fund large investments in product and sales during periods of rapid growth and be profitable when they reach maturity. It is good to see that the gross margin is staying stable which indicates that Adobe is doing a good job controlling costs and is not under a pressure from competition to lower prices.

Key Takeaways from Adobe's Q2 Results

With market capitalisation of $241 billion and more than $5.76 billion in cash, the company has the capacity to continue to prioritise growth.

We were impressed by how strongly Adobe outperformed analysts’ earnings expectations this quarter. And we were also glad that the earnings guidance for the next quarter exceeded analysts' expectations. Overall, we think this was a really good quarter, that should leave shareholders feeling very positive. While the market has high expectations of Adobe we think it will continue to stand out as a very compelling growth stock, arguably even more so than before.

PS. If you found this analysis useful, you will love our earnings alerts! We publish so fast, you often have the opportunity to buy or sell before the market has fully absorbed the information. Never miss out on the right time to invest again. Signup here for free early access.

The author has no position in any of the stocks mentioned.