AeroVironment (NASDAQ:AVAV) Exceeds Q1 Expectations But Stock Drops

Anthony Lee /

June 26, 2024

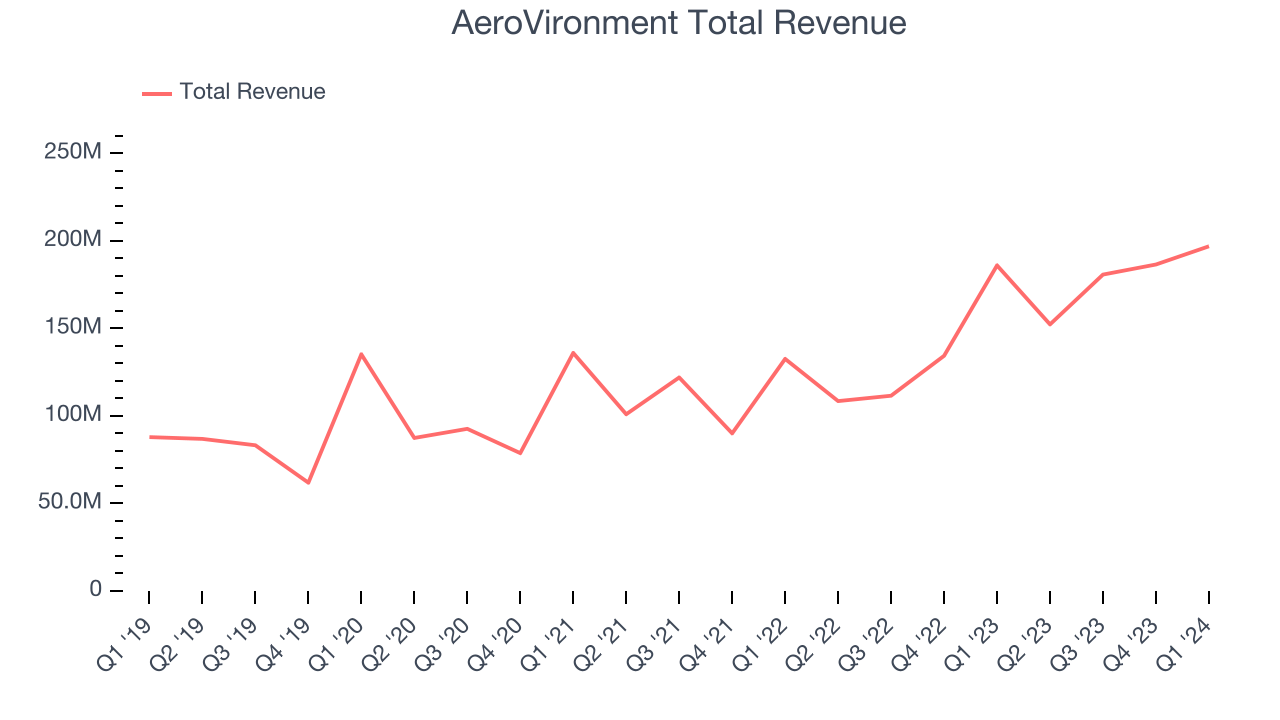

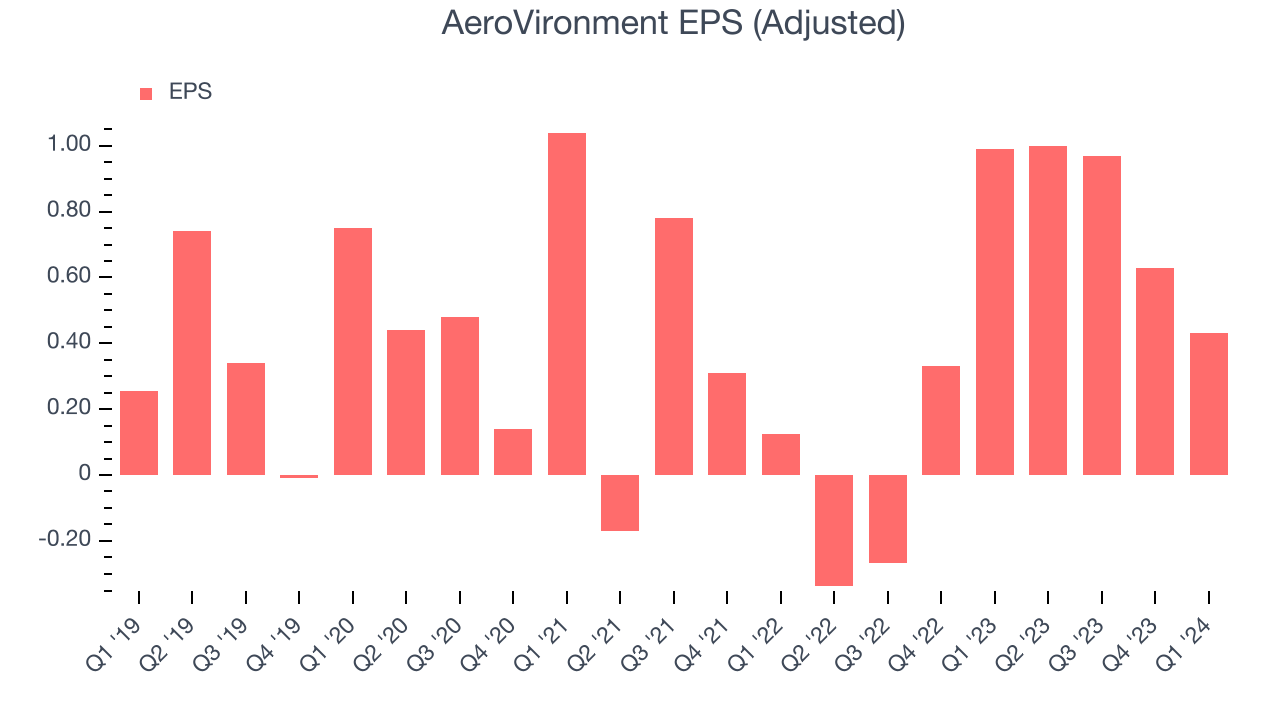

Aerospace and defense company AeroVironment (NASDAQGS:AVAV) reported Q1 CY2024 results topping analysts' expectations, with revenue up 5.9% year on year to $197 million. On the other hand, the company's full-year revenue guidance of $805 million at the midpoint came in slightly below analysts' estimates. It made a non-GAAP profit of $0.43 per share, down from its profit of $0.99 per share in the same quarter last year.

Is now the time to buy AeroVironment? Find out in our full research report.

AeroVironment (AVAV) Q1 CY2024 Highlights:

- Revenue: $197 million vs analyst estimates of $189 million (4.2% beat)

- EPS (non-GAAP): $0.43 vs analyst estimates of $0.21 ($0.22 beat)

- Management's revenue guidance for the upcoming financial year 2025 is $805 million at the midpoint, missing analyst estimates by 0.6% and implying 12.3% growth (vs 36.8% in FY2024)

- EBITDA Guidance for the full year is $148 million at the midpoint, below analyst estimates of $155.3 million

- Gross Margin (GAAP): 38.4%, in line with the same quarter last year

- Free Cash Flow was -$20.76 million, down from $48.76 million in the previous quarter

- Market Capitalization: $5.39 billion

Focused on the future of autonomous military combat, AeroVironment (NASDAQGS:AVAV) specializes in advanced unmanned aircraft systems and electric vehicle charging solutions.

Defense Contractors

Defense contractors typically require technical expertise and government clearance. Companies in this sector can also enjoy long-term contracts with government bodies, leading to more predictable revenues. Combined, these factors create high barriers to entry and can lead to limited competition. Lately, geopolitical tensions–whether it be Russia’s invasion of Ukraine or China’s aggression towards Taiwan–highlight the need for defense spending. On the other hand, demand for these products can ebb and flow with defense budgets and even who is president, as different administrations can have vastly different ideas of how to allocate federal funds.

Sales Growth

A company’s long-term performance can indicate its business health. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Luckily, AeroVironment's sales grew at an incredible 17.9% compounded annual growth rate over the last five years. This is encouraging because it shows AeroVironment's offerings resonate with customers, a helpful starting point for our assessment of quality.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. AeroVironment's annualized revenue growth of 26.8% over the last two years is above its five-year trend, suggesting its demand was strong and recently accelerated.

AeroVironment also breaks out the revenue for its most important segments, Products and Services, which are 83.6% and 16.4% of revenue. Over the last two years, AeroVironment's Products revenue (aircrafts, missile systems, satellites) averaged 66.2% year-on-year growth. On the other hand, its Services revenue (maintenance, training, consulting) averaged 18.9% declines.

This quarter, AeroVironment reported solid year-on-year revenue growth of 5.9%, and its $197 million of revenue outperformed Wall Street's estimates by 4.2%. Looking ahead, Wall Street expects sales to grow 14% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

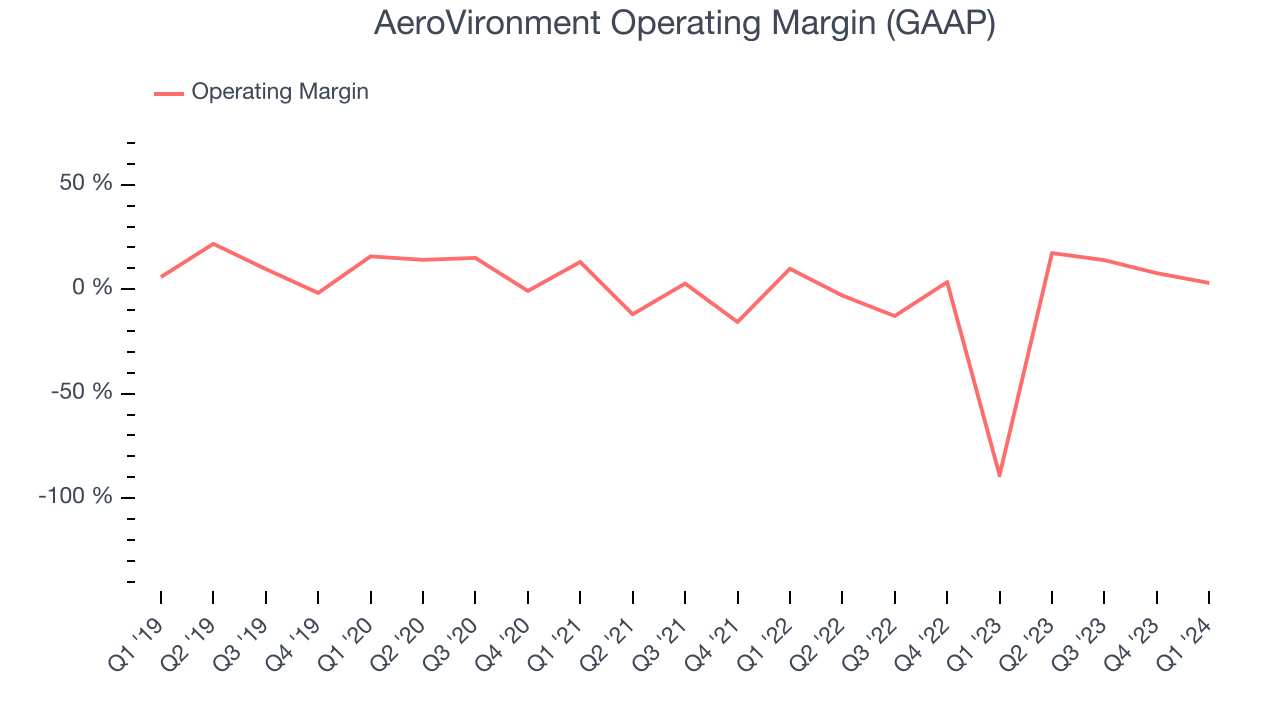

Operating Margin

Operating margin is a key measure of profitability. Think of it as net income–the bottom line–excluding the impact of taxes and interest on debt, which are less connected to business fundamentals.

Although AeroVironment was profitable this quarter from an operational perspective, it's generally struggled when zooming out. Its high expenses have contributed to an average operating margin of negative 1.1% over the last five years. Unprofitable industrials companies require extra attention because they could get caught swimming naked when the tide goes out. It's hard to trust that AeroVironment can endure a full cycle.

Analyzing the trend in its profitability, AeroVironment's annual operating margin decreased by 2.8 percentage points over the last five years. The company's performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn't pass those costs onto its customers.

This quarter, AeroVironment generated an operating profit margin of 3%, up 92.1 percentage points year on year.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

AeroVironment's EPS grew at a spectacular 15.3% compounded annual growth rate over the last five years. However, this performance was lower than its 17.9% annualized revenue growth, telling us the company became less profitable on a per-share basis as it expanded.

We can take a deeper look into AeroVironment's earnings quality to better understand the drivers of its performance. As we mentioned earlier, AeroVironment's operating margin improved this quarter but declined by 2.8 percentage points over the last five years. This was the most relevant factor (aside from revenue) behind its lower earnings; taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a shorter period to see if we are missing a change in the business. For AeroVironment, its two-year annual EPS growth of 70.3% was higher than its five-year trend. We love it when earnings growth accelerates, especially when it accelerates off an already high base.

In Q1, AeroVironment reported EPS at $0.43, down from $0.99 in the same quarter last year. Despite falling year on year, this print easily cleared analysts' estimates. Over the next 12 months, Wall Street expects AeroVironment to grow its earnings. Analysts are projecting its EPS of $3.03 in the last year to climb by 11.1% to $3.37.

Key Takeaways from AeroVironment's Q1 Results

We were impressed by how significantly AeroVironment blew past analysts' EPS expectations this quarter. We were also excited its operating margin outperformed Wall Street's estimates. On the other hand, its full-year revenue and EBITDA guidance fell short of Wall Street's estimates. The poor outlook trumped this quarter's beats, sending the stock price down. The stock traded down 7.7% to $178 immediately following the results.

So should you invest in AeroVironment right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.