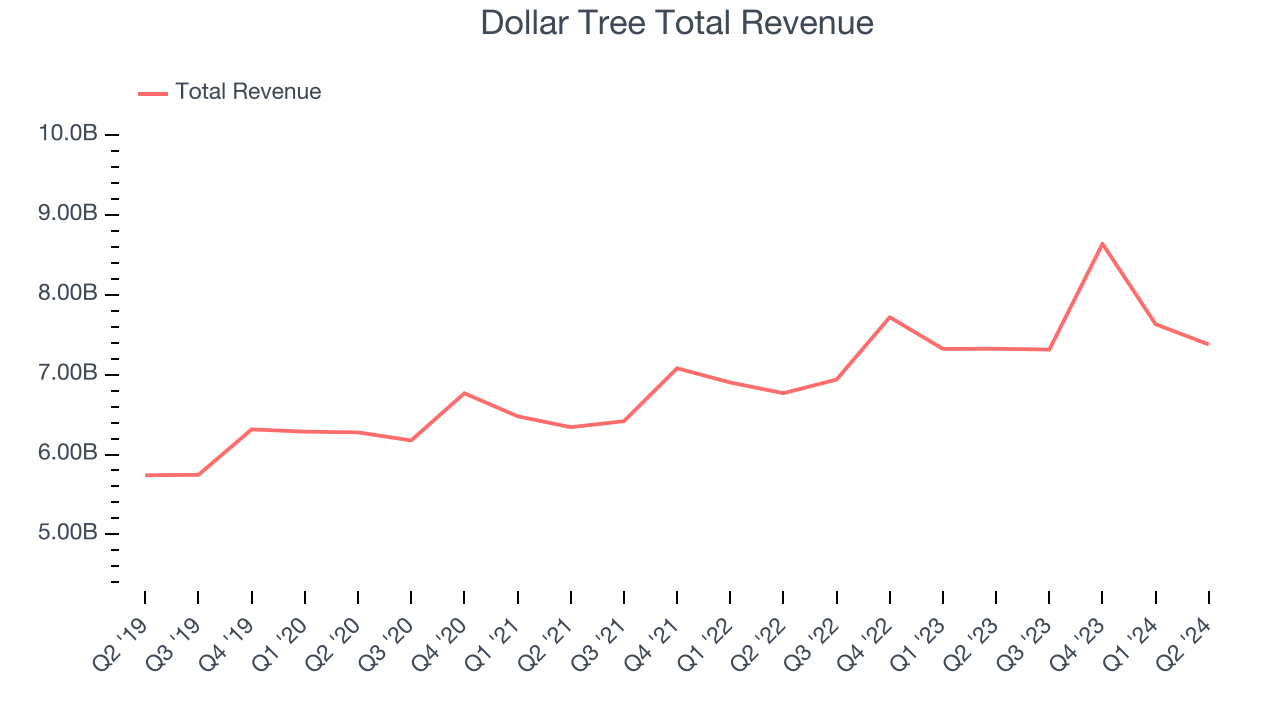

Discount treasure-hunt retailer Dollar Tree (NASDAQ:DLTR) missed analysts’ expectations in Q2 CY2024, with revenue flat year on year at $7.38 billion. Next quarter’s revenue guidance of $7.5 billion also underwhelmed, coming in 1.1% below analysts’ estimates. It made a GAAP profit of $0.62 per share, down from its profit of $0.91 per share in the same quarter last year.

Is now the time to buy Dollar Tree? Find out in our full research report.

Dollar Tree (DLTR) Q2 CY2024 Highlights:

- Revenue: $7.38 billion vs analyst estimates of $7.48 billion (1.4% miss)

- EPS: $0.62 vs analyst expectations of $1.05 (40.8% miss)

- The company dropped its revenue guidance for the full year to $30.75 billion at the midpoint from $31.5 billion, a 2.4% decrease

- Gross Margin (GAAP): 30.1%, in line with the same quarter last year

- EBITDA Margin: 5.7%, down from 6.7% in the same quarter last year

- Free Cash Flow was -$193.8 million compared to -$253.6 million in the same quarter last year

- Locations: 16,388 at quarter end, down from 16,476 in the same quarter last year

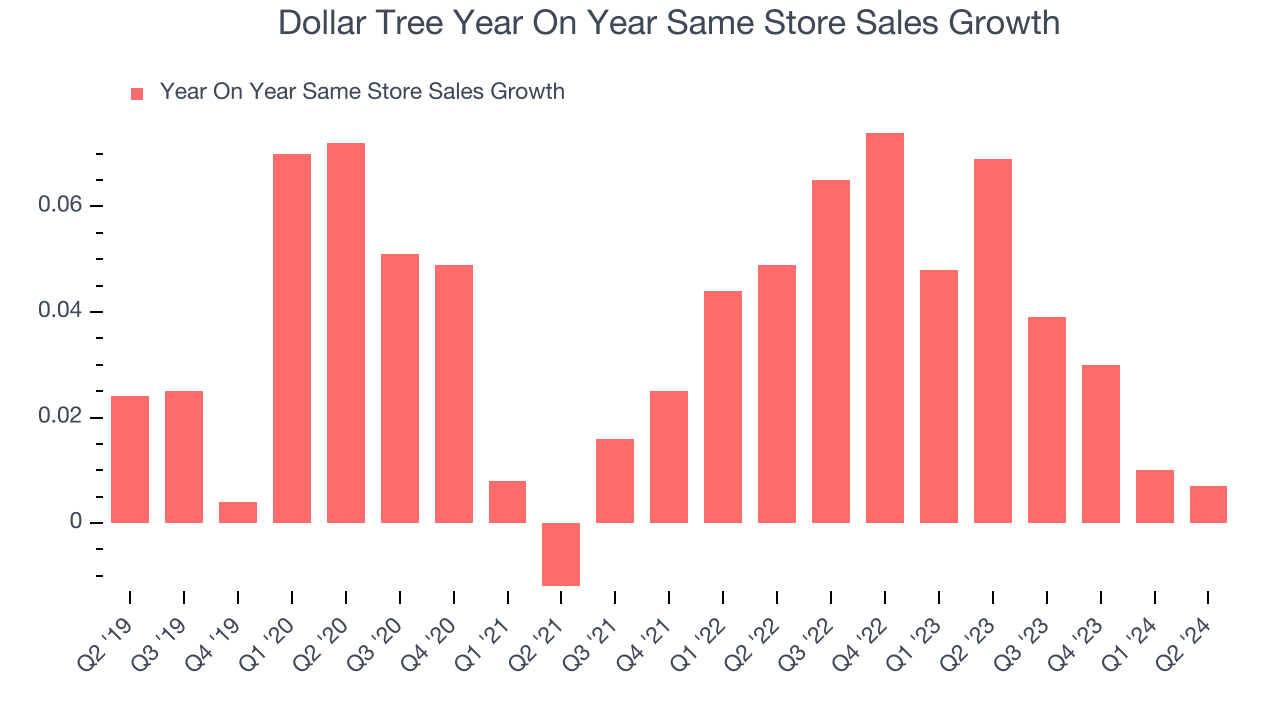

- Same-Store Sales were flat year on year (6.9% in the same quarter last year)

- Market Capitalization: $17.55 billion

A treasure hunt because there’s no guarantee of consistent product selection, Dollar Tree (NASDAQ:DLTR) is a discount retailer that sells general merchandise and select packaged food at extremely low prices.

Discount Grocery Store

Traditional grocery stores are go-tos for many families, but discount grocers serve those who may not have a traditional grocery store nearby or who may have different spending thresholds. Certain rural or lower-income areas simply don’t have a grocery store. Additionally, some lower-income families would prefer to buy in smaller quantities than available at most stores (think one or two paper towel rolls at a time). While online competition threatens all of retail, grocery is one of the least penetrated because of the nature of buying food. Furthermore, those buying small quantities for immediate need are even less likely to leverage e-commerce for these purposes.

Sales Growth

Dollar Tree is one of the larger companies in the consumer retail industry and benefits from economies of scale, enabling it to gain more leverage on fixed costs and offer consumers lower prices.

As you can see below, the company’s annualized revenue growth rate of 5.9% over the last five years was sluggish as its store footprint remained relatively unchanged, implying that growth was driven by more sales at existing, established stores.

This quarter, Dollar Tree’s revenue grew 0.7% year on year to $7.38 billion, falling short of Wall Street’s estimates. The company is guiding for revenue to rise 2.5% year on year to $7.5 billion next quarter, slowing from the 5.4% year-on-year increase it recorded in the same quarter last year. Looking ahead, Wall Street expects sales to grow 3% over the next 12 months, an acceleration from this quarter.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

Dollar Tree’s demand within its existing stores has generally risen over the last two years but lagged behind the broader consumer retail sector. On average, the company’s same-store sales have grown by 4.3% year on year. Given its flat store count over the same period, this performance stems from increased foot traffic at existing stores or higher e-commerce sales as the company shifts demand from in-store to online.

In the latest quarter, Dollar Tree’s year on year same-store sales were flat. By the company’s standards, this growth was a meaningful deceleration from the 6.9% year-on-year increase it posted 12 months ago. We’ll be watching Dollar Tree closely to see if it can reaccelerate growth.

Key Takeaways from Dollar Tree’s Q2 Results

We struggled to find many strong positives in these results. Its revenue and EPS missed analysts’ expectations, and it lowered its full-year revenue guidance. Overall, this was a weaker quarter. The stock traded down 11.2% to $72.50 immediately following the results.

Dollar Tree may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.