Reflecting On Semiconductor Manufacturing Stocks’ Q2 Earnings: IPG Photonics (NASDAQ:IPGP)

Jabin Bastian /

September 16, 2024

Earnings results often indicate what direction a company will take in the months ahead. With Q2 behind us, let’s have a look at IPG Photonics (NASDAQ:IPGP) and its peers.

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 2.7% below.

Stocks--especially those trading at higher multiples--had a strong end of 2023, but this year has seen periods of volatility. Mixed signals about inflation have led to uncertainty around rate cuts, and while some semiconductor manufacturing stocks have fared somewhat better than others, they have collectively declined. On average, share prices are down 4.5% since the latest earnings results.

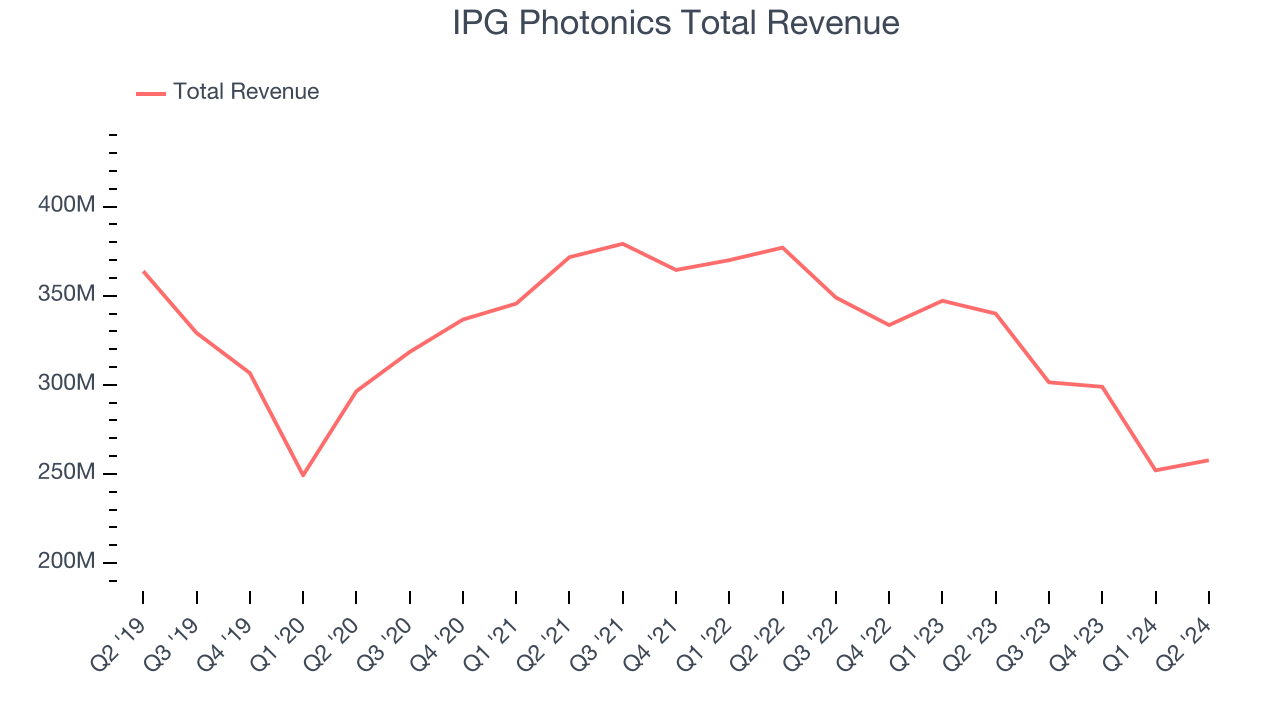

IPG Photonics (NASDAQ:IPGP)

Both a designer and manufacturer of its products, IPG Photonics (NASDAQ:IPGP) is a provider of high-performance fiber lasers used for cutting, welding, and processing raw materials.

IPG Photonics reported revenues of $257.6 million, down 24.2% year on year. This print was in line with analysts’ expectations, but overall, it was a slower quarter for the company with underwhelming revenue guidance for the next quarter and a decline in its operating margin.

"IPG's second quarter results reflect a challenging demand environment, particularly across industrial and e-mobility markets. Our focus on financial execution allowed the company to generate strong cash flow from operations and significantly reduce inventory, while continuing to work on significant product cost reductions," said Dr. Mark Gitin, IPG Photonics' Chief Executive Officer.

IPG Photonics delivered the slowest revenue growth of the whole group. Unsurprisingly, the stock is down 22.8% since reporting and currently trades at $67.67.

Read our full report on IPG Photonics here, it’s free.

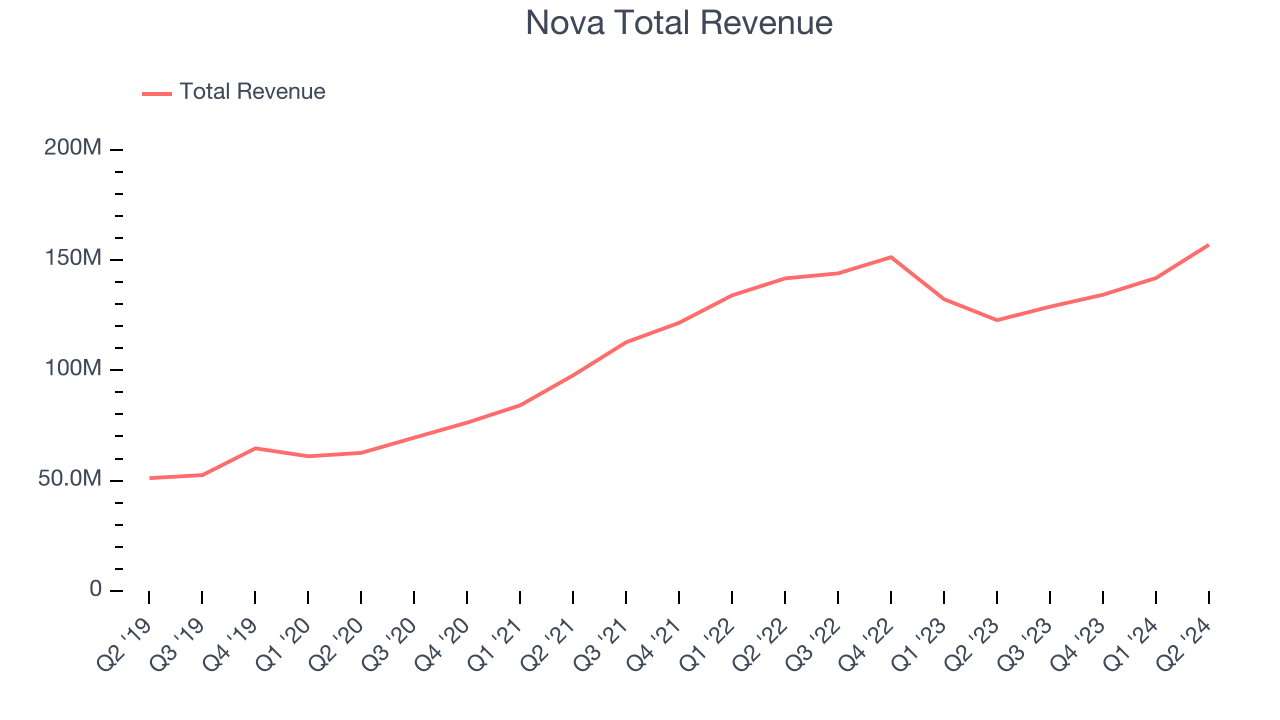

Best Q2: Nova (NASDAQ:NVMI)

Headquartered in Israel, Nova (NASDAQ:NVMI) is a provider of quality control systems used in semiconductor manufacturing.

Nova reported revenues of $156.9 million, up 27.8% year on year, outperforming analysts’ expectations by 5.9%. The business had an exceptional quarter with an impressive beat of analysts’ EPS estimates and a significant improvement in its operating margin.

Nova achieved the fastest revenue growth among its peers. The market seems happy with the results as the stock is up 10.7% since reporting. It currently trades at $200.63.

Is now the time to buy Nova? Access our full analysis of the earnings results here, it’s free.

Photronics (NASDAQ:PLAB)

Sporting a global footprint of facilities, Photronics (NASDAQ:PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Photronics reported revenues of $211 million, down 5.9% year on year, falling short of analysts’ expectations by 6.2%. It was a softer quarter as it posted underwhelming revenue guidance for the next quarter and a miss of analysts’ EPS estimates.

Photronics delivered the weakest performance against analyst estimates in the group. As expected, the stock is down 3% since the results and currently trades at $23.32.

Read our full analysis of Photronics’s results here.

FormFactor (NASDAQ:FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ:FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $197.5 million, up 26.7% year on year. This print topped analysts’ expectations by 1.3%. Overall, it was an exceptional quarter as it also logged a significant improvement in its gross margin and an impressive beat of analysts’ EPS estimates.

The stock is down 18.5% since reporting and currently trades at $43.67.

Read our full, actionable report on FormFactor here, it’s free.

Lam Research (NASDAQ:LRCX)

Founded in 1980 by David Lam, who pioneered semiconductor etching technology, Lam Research (NASDAQ:LCRX) is one of the leading providers of the wafer fabrication equipment used to make semiconductors.

Lam Research reported revenues of $3.87 billion, up 20.7% year on year. This result beat analysts’ expectations by 1%. Overall, it was a strong quarter as it also logged an impressive beat of analysts’ EPS estimates and a meaningful improvement in its operating margin.

The stock is down 16.5% since reporting and currently trades at $770.56.

Read our full, actionable report on Lam Research here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.