Jamf (NASDAQ:JAMF) Exceeds Q2 Expectations, Provides Encouraging Quarterly Guidance

Petr Huřťák /

August 7, 2024

Apple device management company, Jamf (NASDAQ:JAMF) reported results ahead of analysts' expectations in Q2 CY2024, with revenue up 13.3% year on year to $153 million. Guidance for next quarter's revenue was also better than expected at $157.5 million at the midpoint, 1.3% above analysts' estimates. It made a non-GAAP profit of $0.14 per share, improving from its profit of $0.05 per share in the same quarter last year.

Is now the time to buy Jamf? Find out in our full research report.

Jamf (JAMF) Q2 CY2024 Highlights:

- Revenue: $153 million vs analyst estimates of $151.7 million (small beat)

- Adjusted Operating Income: $23.54 million vs analyst estimates of $21.95 million (7.2% beat)

- EPS (non-GAAP): $0.14 vs analyst expectations of $0.14 (in line)

- Revenue Guidance for Q3 CY2024 is $157.5 million at the midpoint, above analyst estimates of $155.5 million

- The company slightly lifted its revenue guidance for the full year from $620.5 million to $624 million at the midpoint

- Gross Margin (GAAP): 77.1%, down from 79.7% in the same quarter last year

- Free Cash Flow of $13.34 million is up from -$17.66 million in the previous quarter

- Billings: $158.7 million at quarter end, up 6.3% year on year

- Market Capitalization: $2.08 billion

Founded in 2002 by Zach Halmstad and Chip Pearson, right around the time when Apple began to dominate the personal computing market, Jamf (NASDAQ:JAMF) provides software for companies to manage Apple devices such as Macs, iPads, and iPhones.

Automation Software

The whole purpose of software is to automate tasks to increase productivity. Today, innovative new software techniques, often involving AI and machine learning, are finally allowing automation that has graduated from simple one- or two-step workflows to more complex processes integral to enterprises. The result is surging demand for modern automation software.

Sales Growth

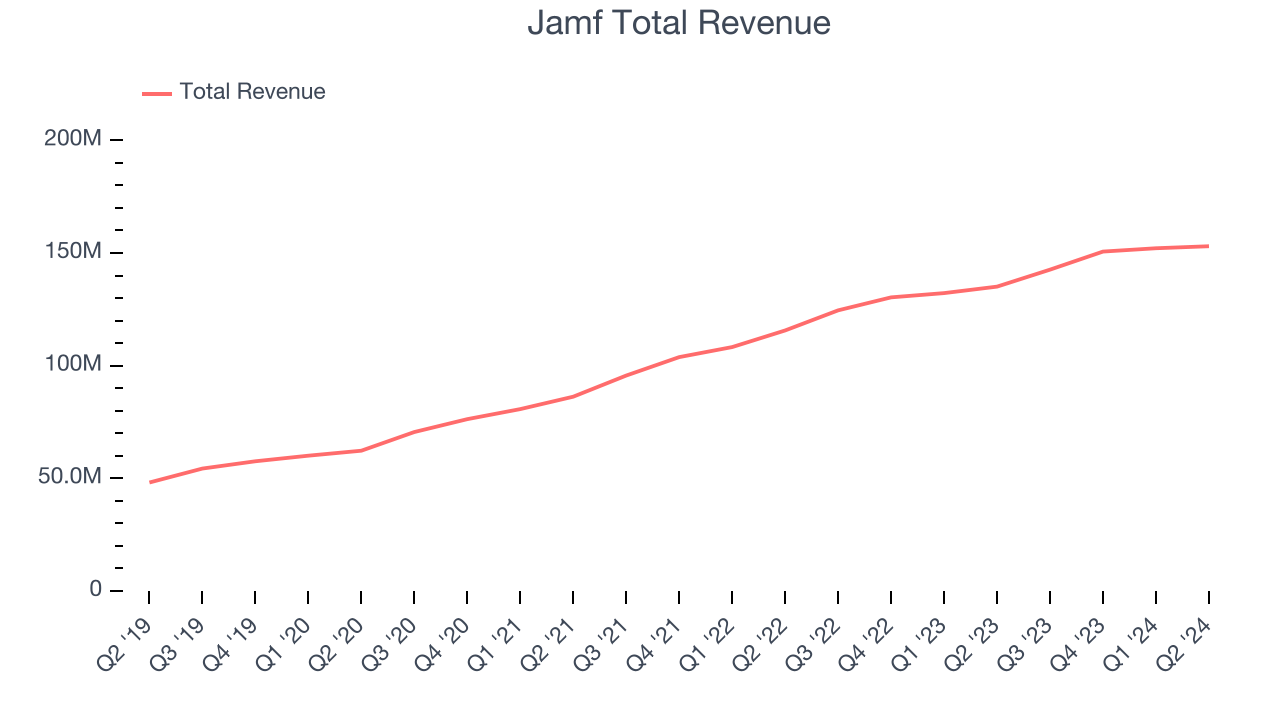

As you can see below, Jamf's 24% annualized revenue growth over the last three years has been solid, and its sales came in at $153 million this quarter.

This quarter, Jamf's quarterly revenue was once again up 13.3% year on year. However, its growth did slow down compared to last quarter as the company's revenue increased by just $893,000 in Q2 compared to $1.48 million in Q1 CY2024. While we'd like to see revenue increase by a greater amount each quarter, a one-off fluctuation is usually not concerning.

Next quarter's guidance suggests that Jamf is expecting revenue to grow 10.4% year on year to $157.5 million, slowing down from the 14.5% year-on-year increase it recorded in the same quarter last year. Looking ahead, analysts covering the company were expecting sales to grow 9.7% over the next 12 months before the earnings results announcement.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Cash Is King

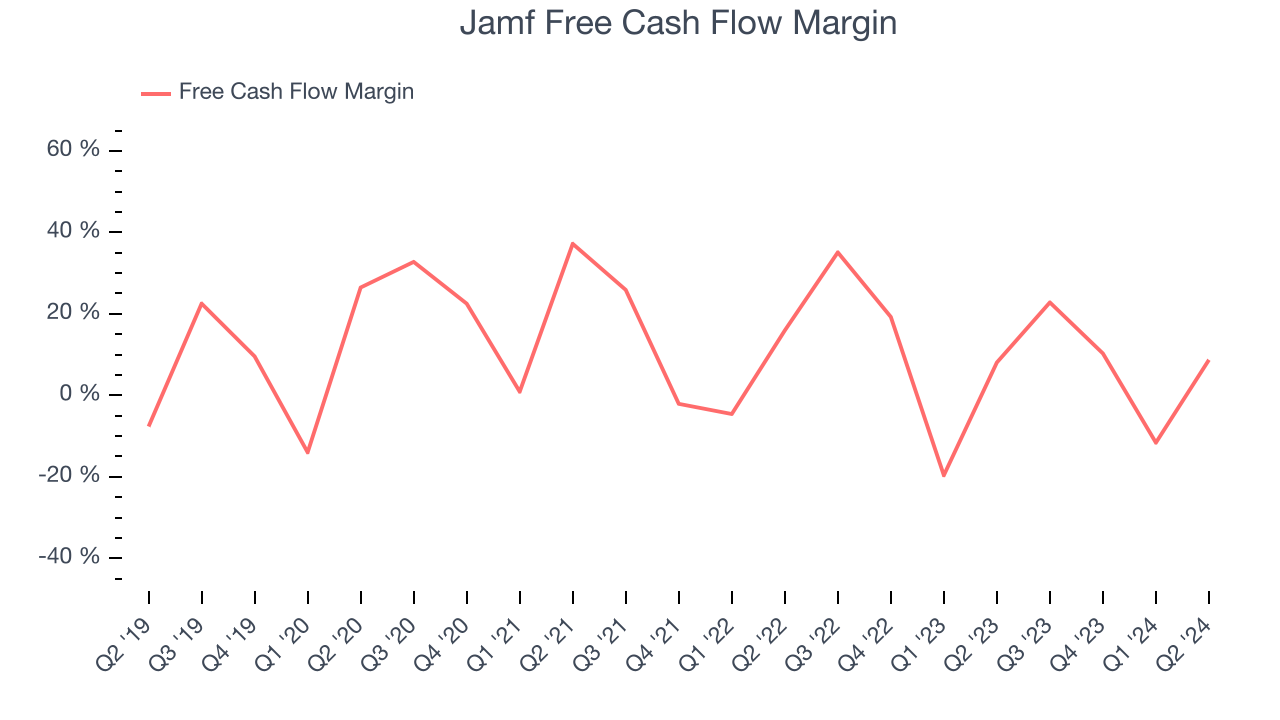

If you've followed StockStory for a while, you know we emphasize free cash flow. Why, you ask? We believe that in the end, cash is king, and you can't use accounting profits to pay the bills.

Jamf has shown mediocre cash profitability over the last year, giving the company limited opportunities to return capital to shareholders. Its free cash flow margin averaged 7.3%, subpar for a software business.

Jamf's free cash flow clocked in at $13.34 million in Q2, equivalent to a 8.7% margin. This quarter's cash profitability was in line with the comparable period last year and above its one-year average.

Over the next year, analysts predict Jamf's cash conversion will improve. Their consensus estimates imply its free cash flow margin of 7.3% for the last 12 months will increase to 18.1%, giving it more money to invest.

Key Takeaways from Jamf's Q2 Results

It was encouraging to see Jamf slightly beat analysts' revenue guidance expectations. On the other hand, its billings unfortunately missed analysts' expectations and its gross margin decreased. Overall, this was a mixed but overall mediocre quarter for Jamf. The stock traded down 3% to $15.84 immediately following the results.

Jamf may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.