Semiconductor Manufacturing Q2 Earnings: Nova (NASDAQ:NVMI) Simply the Best

Max Juang /

October 1, 2024

The end of the earnings season is always a good time to take a step back and see who shined (and who not so much). Let’s take a look at how semiconductor manufacturing stocks fared in Q2, starting with Nova (NASDAQ:NVMI).

The semiconductor industry is driven by demand for advanced electronic products like smartphones, PCs, servers, and data storage. The need for technologies like artificial intelligence, 5G networks, and smart cars is also creating the next wave of growth for the industry. Keeping up with this dynamism requires new tools that can design, fabricate, and test chips at ever smaller sizes and more complex architectures, creating a dire need for semiconductor capital manufacturing equipment.

The 14 semiconductor manufacturing stocks we track reported a strong Q2. As a group, revenues beat analysts’ consensus estimates by 1.9% while next quarter’s revenue guidance was 2.7% below.

Inflation progressed towards the Fed's 2% goal recently, leading the Fed to reduce its policy rate by 50bps (half a percent or 0.5%) in September 2024. This is the first cut in four years. While CPI (inflation) readings have been supportive lately, employment measures have bordered on worrisome. The markets will be debating whether this rate cut's timing (and more potential ones in 2024 and 2025) is ideal for supporting the economy or a bit too late for a macro that has already cooled too much.

Semiconductor manufacturing stocks have held steady amidst all this with average share prices relatively unchanged since the latest earnings results.

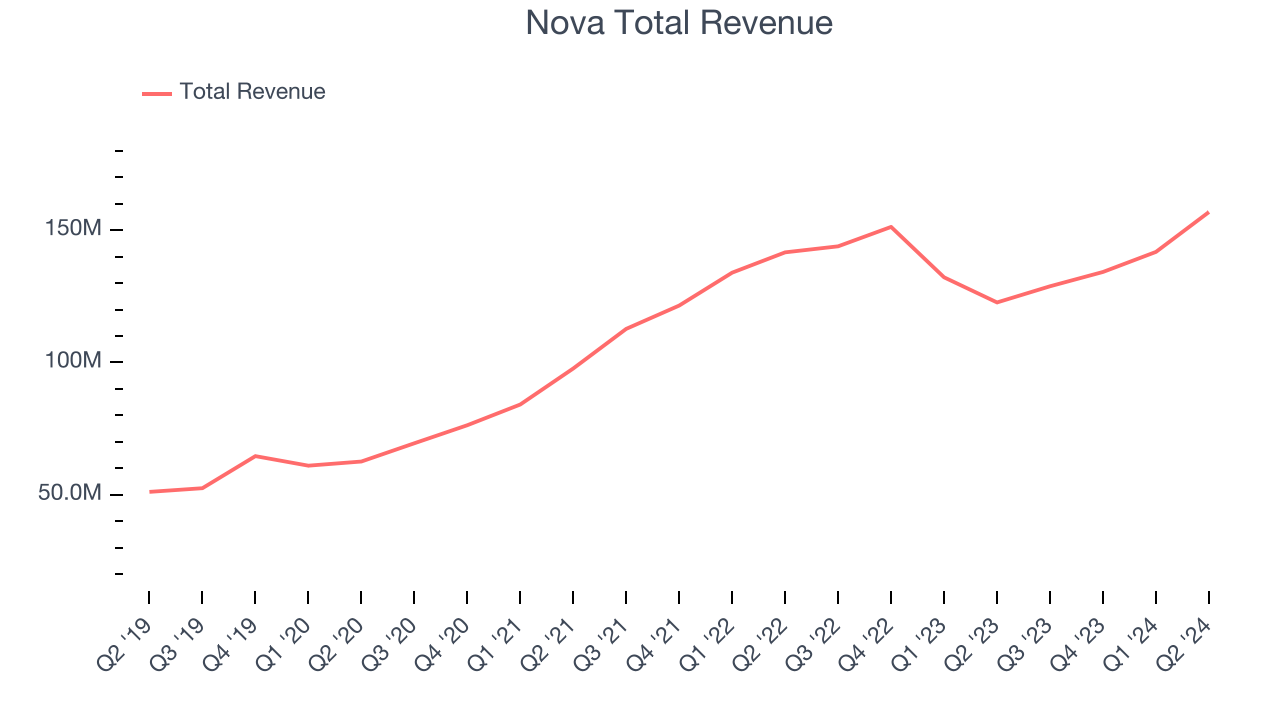

Best Q2: Nova (NASDAQ:NVMI)

Headquartered in Israel, Nova (NASDAQ:NVMI) is a provider of quality control systems used in semiconductor manufacturing.

Nova reported revenues of $156.9 million, up 27.8% year on year. This print exceeded analysts’ expectations by 5.9%. Overall, it was an exceptional quarter for the company with an impressive beat of analysts’ EPS estimates and a significant improvement in its operating margin.

"Nova delivered an exceptionally strong quarter, exceeding the high end of the guidance, with record results across the board," said Gaby Waisman, President and CEO.

Nova achieved the fastest revenue growth of the whole group. Unsurprisingly, the stock is up 16.3% since reporting and currently trades at $210.81.

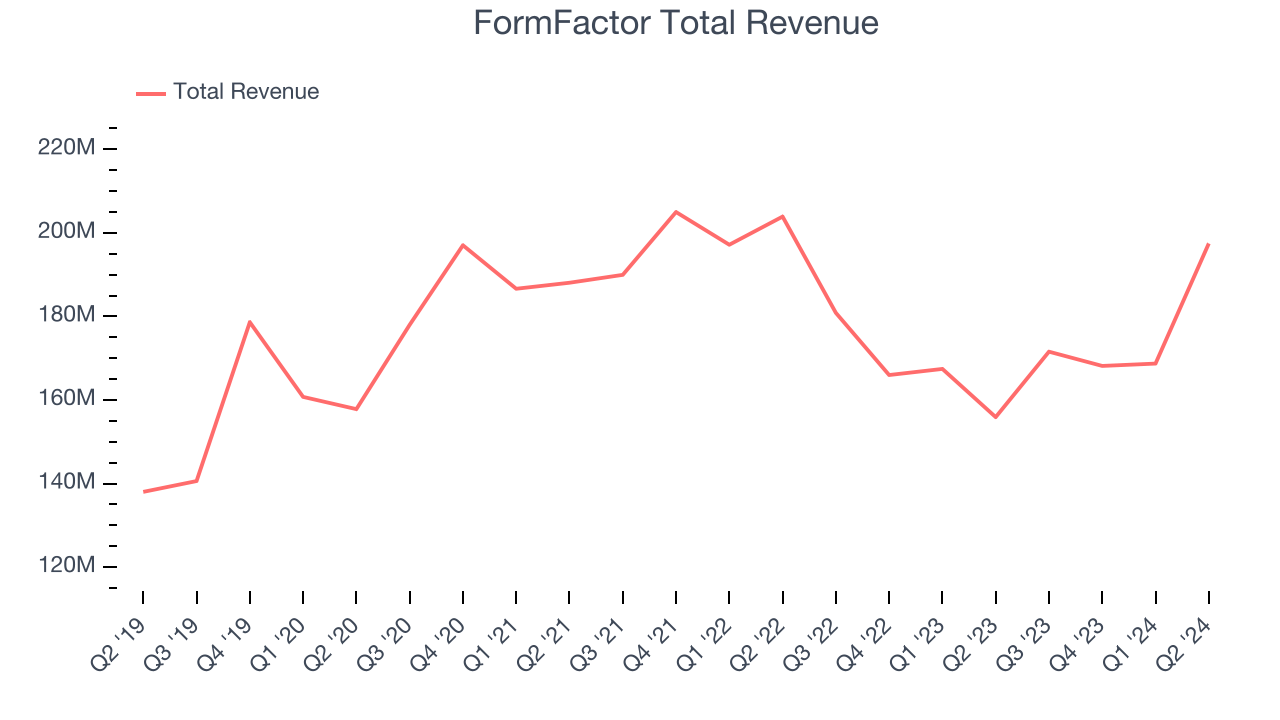

FormFactor (NASDAQ:FORM)

With customers across the foundry and fabless markets, FormFactor (NASDAQ:FORM) is a US-based provider of test and measurement technologies for semiconductors.

FormFactor reported revenues of $197.5 million, up 26.7% year on year, outperforming analysts’ expectations by 1.3%. The business had an exceptional quarter with a significant improvement in its gross margin and an impressive beat of analysts’ EPS estimates.

Although it had a fine quarter compared its peers, the market seems unhappy with the results as the stock is down 14.1% since reporting. It currently trades at $46.

Is now the time to buy FormFactor? Access our full analysis of the earnings results here, it’s free.

Slowest Q2: Photronics (NASDAQ:PLAB)

Sporting a global footprint of facilities, Photronics (NASDAQ:PLAB) is a manufacturer of photomasks, templates used to transfer patterns onto semiconductor wafers.

Photronics reported revenues of $211 million, down 5.9% year on year, falling short of analysts’ expectations by 6.2%. It was a softer quarter as it posted underwhelming revenue guidance for the next quarter and a miss of analysts’ EPS estimates.

Photronics delivered the weakest performance against analyst estimates in the group. Interestingly, the stock is up 3.9% since the results and currently trades at $24.99.

Read our full analysis of Photronics’s results here.

Lam Research (NASDAQ:LRCX)

Founded in 1980 by David Lam, the man who pioneered semiconductor etching technology, Lam Research (NASDAQ:LRCX) is one of the leading providers of wafer fabrication equipment used to make semiconductors.

Lam Research reported revenues of $3.87 billion, up 20.7% year on year. This print beat analysts’ expectations by 1%. It was a strong quarter as it also put up an impressive beat of analysts’ EPS estimates and a meaningful improvement in its operating margin.

The stock is down 11.2% since reporting and currently trades at $819.28.

Read our full, actionable report on Lam Research here, it’s free.

IPG Photonics (NASDAQ:IPGP)

Both a designer and manufacturer of its products, IPG Photonics (NASDAQ:IPGP) is a provider of high-performance fiber lasers used for cutting, welding, and processing raw materials.

IPG Photonics reported revenues of $257.6 million, down 24.2% year on year. This number was in line with analysts’ expectations. More broadly, it was a weak quarter as it produced underwhelming revenue guidance for the next quarter and a decline in its operating margin.

IPG Photonics had the slowest revenue growth among its peers. The stock is down 17.5% since reporting and currently trades at $72.25.

Read our full, actionable report on IPG Photonics here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.