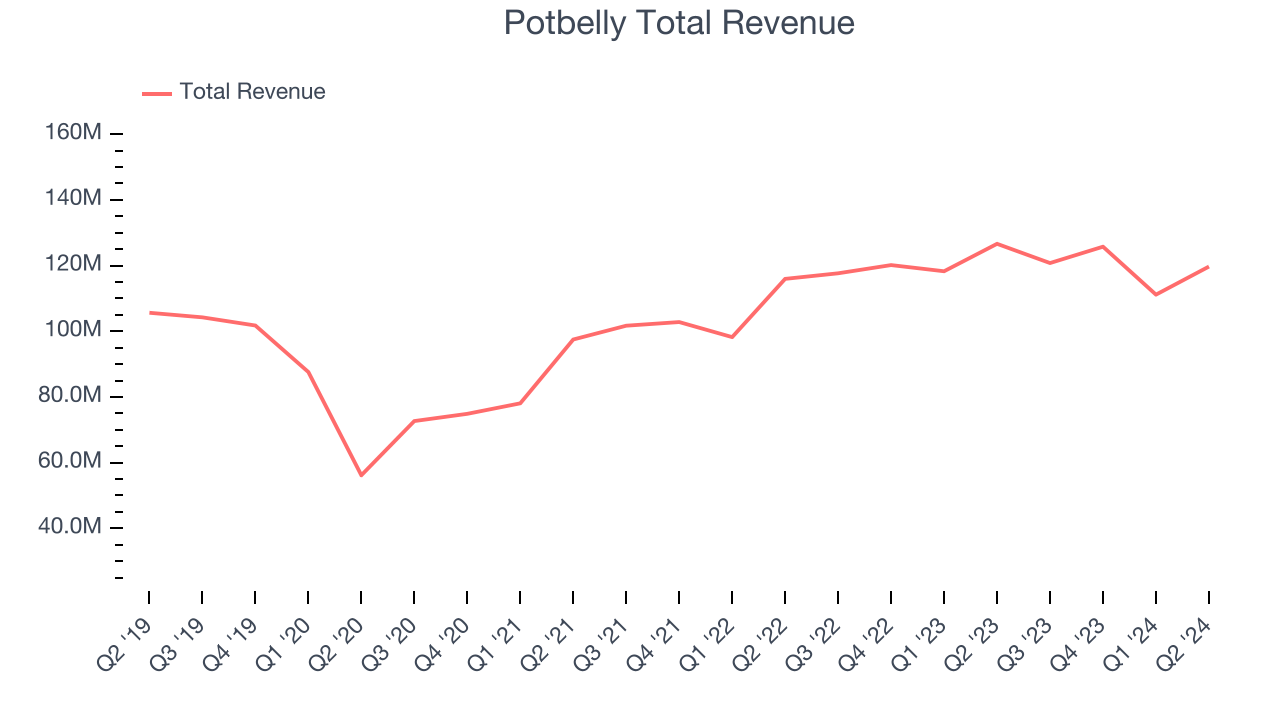

Casual sandwich chain Potbelly (NASDAQ:PBPB) reported results in line with analysts' expectations in Q2 CY2024, with revenue down 5.5% year on year to $119.7 million. It made a non-GAAP profit of $0.08 per share, improving from its profit of $0.07 per share in the same quarter last year.

Is now the time to buy Potbelly? Find out in our full research report.

Potbelly (PBPB) Q2 CY2024 Highlights:

- Revenue: $119.7 million vs analyst estimates of $119.6 million (small beat)

- EPS (non-GAAP): $0.08 vs analyst estimates of $0.06 (33.3% beat)

- Gross Margin (GAAP): 36.4%, up from 32.2% in the same quarter last year

- EBITDA Margin: 7.1%, in line with the same quarter last year

- Free Cash Flow was -$4.84 million compared to -$3.27 million in the previous quarter

- Locations: 425 at quarter end, down from 427 in the same quarter last year

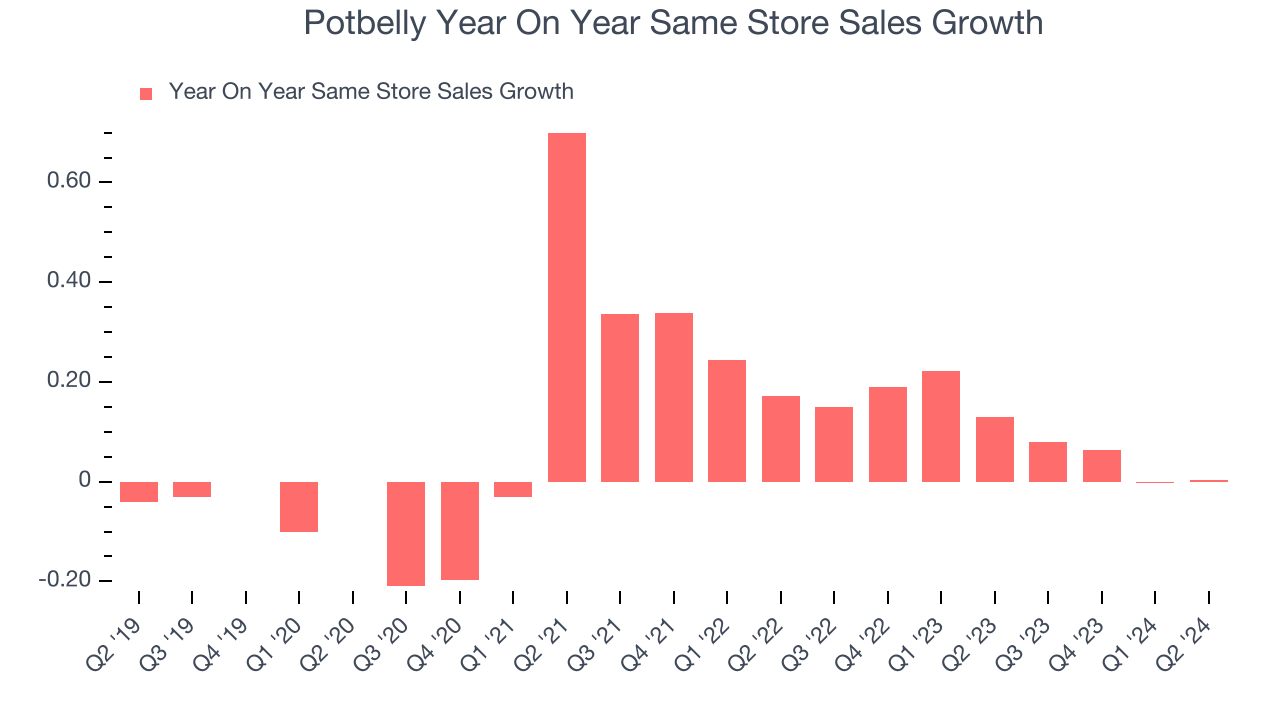

- Same-Store Sales were flat year on year (12.9% in the same quarter last year)

- Market Capitalization: $198.4 million

Bob Wright, President and Chief Executive Officer of Potbelly Corporation, commented, “The hard work and dedication of our team members during the second quarter enabled us to continue our growth in three key areas of the business. We grew same-store sales by 0.4%, we posted our 13th consecutive quarter of year-over-year shop margin expansion, and we opened four new shops to go along with franchise commitments for 22 additional shops. As we look ahead to the second half of 2024 and beyond, despite the challenging macro environment, we remain incredibly confident in the future of our brand. First and foremost, our customer satisfaction scores continue to indicate that our customers love our food and service. Second, our digital channels including our Potbelly Perks loyalty program remain a key driver of our business. And finally, we are seeing success with new shop openings, which on average, are outperforming our expectations. In short, we remain focused on executing our Five-Pillar Strategy as we grow our brand to create value for stakeholders.”

With a unique origin story where the company actually started as an antique shop, Potbelly (NASDAQ:PBPB) today is a chain known for its toasty sandwiches.

Modern Fast Food

Modern fast food is a relatively newer category representing a middle ground between traditional fast food and sit-down restaurants. These establishments feature an expanded menu selection priced above traditional fast food options, often incorporating fresher and cleaner ingredients to serve customers prioritizing quality. These eateries are capitalizing on the perception that your drive-through burger and fries joint is detrimental to your health because of inferior ingredients.

Sales Growth

Potbelly is a small restaurant chain, which sometimes brings disadvantages compared to larger competitors benefitting from better brand awareness and economies of scale.

As you can see below, the company's annualized revenue growth rate of 2.9% over the last five years was weak, but to its credit, it opened new restaurants and grew sales at existing, established dining locations.

This quarter, Potbelly reported a rather uninspiring 5.5% year-on-year revenue decline to $119.7 million in revenue, in line with Wall Street's estimates. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Same-Store Sales

Same-store sales growth is an important metric that tracks organic growth and demand for a restaurant's established locations.

Potbelly's demand has outpaced the broader restaurant sector over the last eight quarters. On average, the company has grown its same-store sales by a robust 10.4% year on year. This performance suggests its steady rollout of new restaurants could be beneficial for shareholders. When a company has strong demand, more locations should help it reach more customers seeking its meals.

In the latest quarter, Potbelly's year on year same-store sales were flat. By the company's standards, this growth was a meaningful deceleration from the 12.9% year-on-year increase it posted 12 months ago. We'll be watching Potbelly closely to see if it can reaccelerate growth.

Key Takeaways from Potbelly's Q2 Results

We were impressed by how significantly Potbelly blew past analysts' gross margin expectations this quarter. We were also excited its EPS outperformed Wall Street's estimates. Zooming out, we think this was a good quarter with some key areas of upside. The stock traded up 4.4% to $7.15 immediately following the results.

Potbelly may have had a good quarter, but does that mean you should invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.