Plug Power (NASDAQ:PLUG) Reports Sales Below Analyst Estimates In Q2 Earnings, Stock Drops

Radek Strnad /

August 8, 2024

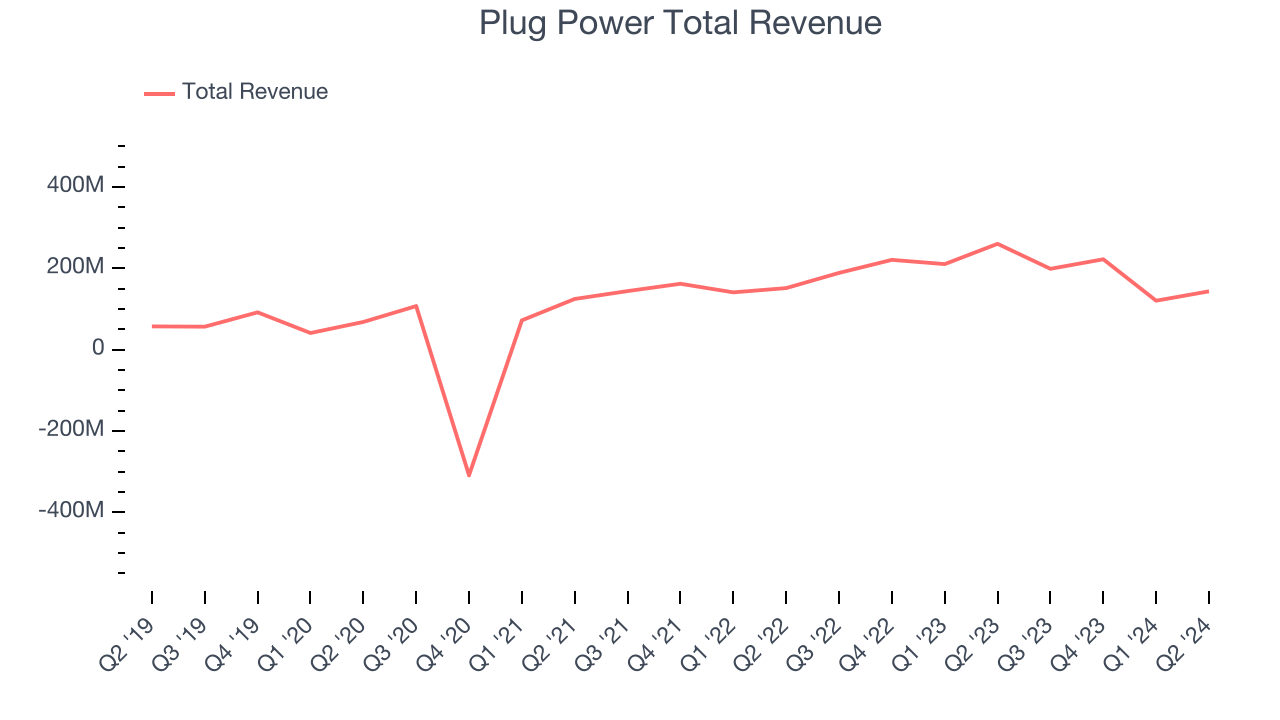

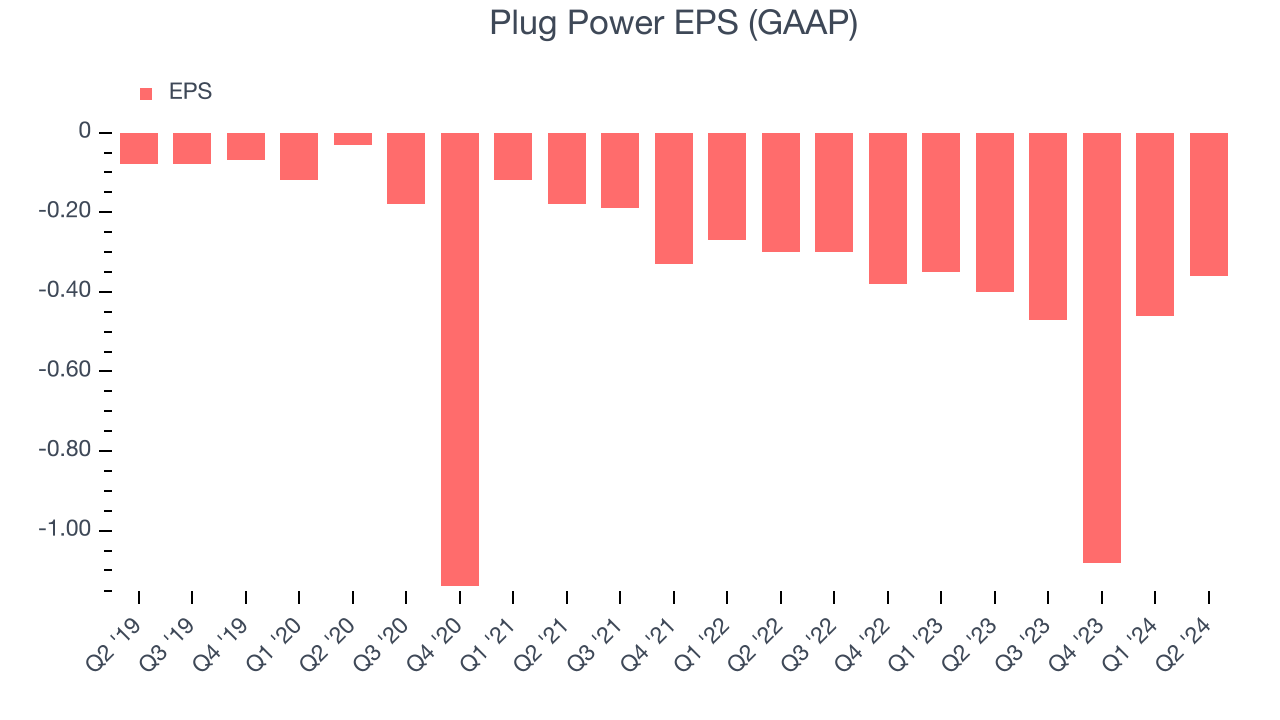

Fuel cell technology Plug Power (NASDAQ:PLUG) fell short of analysts' expectations in Q2 CY2024, with revenue down 44.9% year on year to $143.4 million. The company's full-year revenue guidance of $875 million at the midpoint also came in 3.9% below analysts' estimates. It made a GAAP loss of $0.36 per share, improving from its loss of $0.40 per share in the same quarter last year.

Is now the time to buy Plug Power? Find out in our full research report.

Plug Power (PLUG) Q2 CY2024 Highlights:

- Revenue: $143.4 million vs analyst estimates of $186.2 million (23% miss)

- EPS: -$0.36 vs analyst expectations of -$0.31 (17.3% miss)

- Gross Margin (GAAP): -91.6%, down from -27.2% in the same quarter last year

- Free Cash Flow was -$356 million compared to -$260.3 million in the previous quarter

- Market Capitalization: $1.71 billion

Plug Power CEO Andy Marsh stated: "The second quarter of 2024 has been pivotal for Plug Power as we continue to make strides in our strategic initiatives and operational capabilities. The addition of Dean Fullerton as COO strengthens our leadership team, and our recent achievements in electrolyzer deployments and partnerships demonstrate our unwavering commitment to advancing the hydrogen economy. We are excited about the opportunities ahead and remain focused on delivering sustainable energy solutions that drive value for our customers and stakeholders."

Powering forklifts for Walmart’s distribution centers, Plug Power (NASDAQ:PLUG) provides hydrogen fuel cells used to power electric motors.

Renewable Energy

Renewable energy companies are buoyed by the secular trend of green energy that is upending traditional power generation. Those who innovate and evolve with this dynamic market can win share while those who continue to rely on legacy technologies can see diminishing demand, which includes headwinds from increasing regulation against “dirty” energy. Additionally, these companies are at the whim of economic cycles, as interest rates can impact the willingness to invest in renewable energy projects.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Over the last five years, Plug Power grew its sales at an incredible 29% compounded annual growth rate. This shows it expanded quickly, a useful starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Plug Power's recent history shows its demand slowed significantly as its annualized revenue growth of 7% over the last two years is well below its five-year trend.

Plug Power also breaks out the revenue for its three most important segments: Product, Power Purchase Agreements, and Fuel, which are 53.6%, 13.7%, and 20.8% of revenue. Over the last two years, Plug Power's revenues in all three segments increased. Its Product revenue (equipment and infrastructure sales) averaged year-on-year growth of 10.6% while its Power Purchase Agreements (renewable energy contracts) and Fuel (delivering fuel to customers) revenues averaged 47.3% and 31.3%.

This quarter, Plug Power missed Wall Street's estimates and reported a rather uninspiring 44.9% year-on-year revenue decline, generating $143.4 million of revenue. Looking ahead, Wall Street expects sales to grow 66.8% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

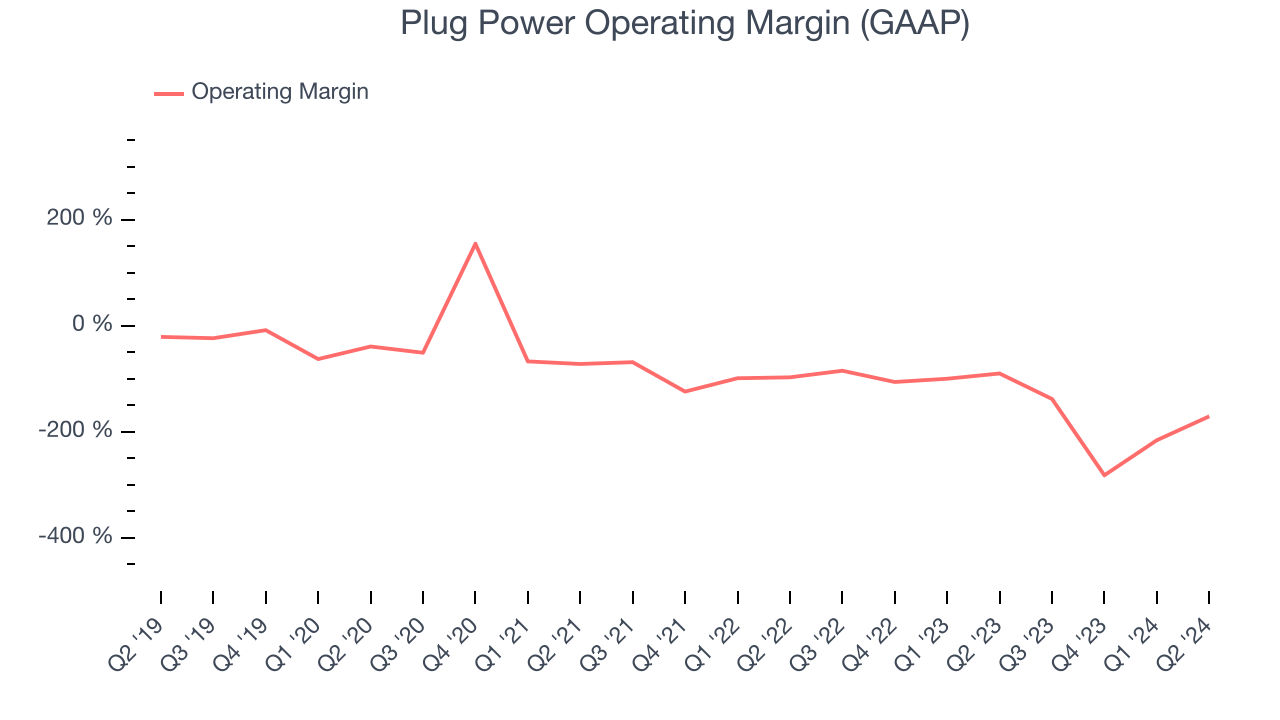

Unprofitable industrials companies require extra attention because they could get caught swimming naked if the tide goes out. It's hard to trust that Plug Power can endure a full cycle as its high expenses have contributed to an average operating margin of negative 148% over the last five years. This result isn't too surprising given its low gross margin as a starting point.

Analyzing the trend in its profitability, Plug Power's annual operating margin decreased significantly over the last five years. The company's performance was poor no matter how you look at it. It shows operating expenses were rising and it couldn't pass those costs onto its customers.

In Q2, Plug Power generated an operating profit margin of negative 171%, down 80.8 percentage points year on year. Since Plug Power's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

Analyzing long-term revenue trends tells us about a company's historical growth, but the long-term change in its earnings per share (EPS) points to the profitability of that growth–for example, a company could inflate its sales through excessive spending on advertising and promotions.

Plug Power's earnings losses deepened over the last five years as its EPS dropped 44.9% annually. We tend to steer our readers away from companies with falling EPS, where diminishing earnings could imply changing secular trends and preferences. If the tide turns unexpectedly, Plug Power's low margin of safety could leave its stock price susceptible to large downswings.

In Q2, Plug Power reported EPS at negative $0.36, up from negative $0.40 in the same quarter last year. Despite growing year on year, this print missed analysts' estimates. Over the next 12 months, Wall Street expects Plug Power to improve its earnings losses. Analysts are projecting its EPS of negative $2.37 in the last year to advance to negative $0.76.

Key Takeaways from Plug Power's Q2 Results

It was good to see Plug Power beat analysts' Fuel revenue expectations this quarter. On the other hand, its full-year revenue guidance missed and its revenue fell short of Wall Street's estimates. Overall, this was a mediocre quarter for Plug Power. The stock traded down 8.9% to $1.90 immediately following the results.

Plug Power may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.