As the Q2 earnings season wraps, let’s dig into this quarter’s best and worst performers in the sales and marketing software industry, including Sprout Social (NASDAQ:SPT) and its peers.

The Internet and the exploding amount of data have transformed how businesses interact with, market to, and transact with their customers. Personalization of offerings, e-commerce, targeted advertising and data-empowered sales teams are now table stakes for modern businesses, and sales and marketing software providers are becoming the tools of evolving customer interaction.

The 23 sales and marketing software stocks we track reported a mixed Q2. As a group, revenues beat analysts’ consensus estimates by 1.2% while next quarter’s revenue guidance was in line.

Big picture, the Federal Reserve has a dual mandate of inflation and employment. The former had been running hot throughout 2021 and 2022 but cooled towards the central bank's 2% target as of late. This prompted the Fed to cut its policy rate by 50bps (half a percent) in September 2024. Given recent employment data that suggests the US economy could be wobbling, the markets will be assessing whether this rate and future cuts (the Fed signaled more to come in 2024 and 2025) are the right moves at the right time or whether they're too little, too late for a macro that has already cooled.

Thankfully, sales and marketing software stocks have been resilient with share prices up 7.7% on average since the latest earnings results.

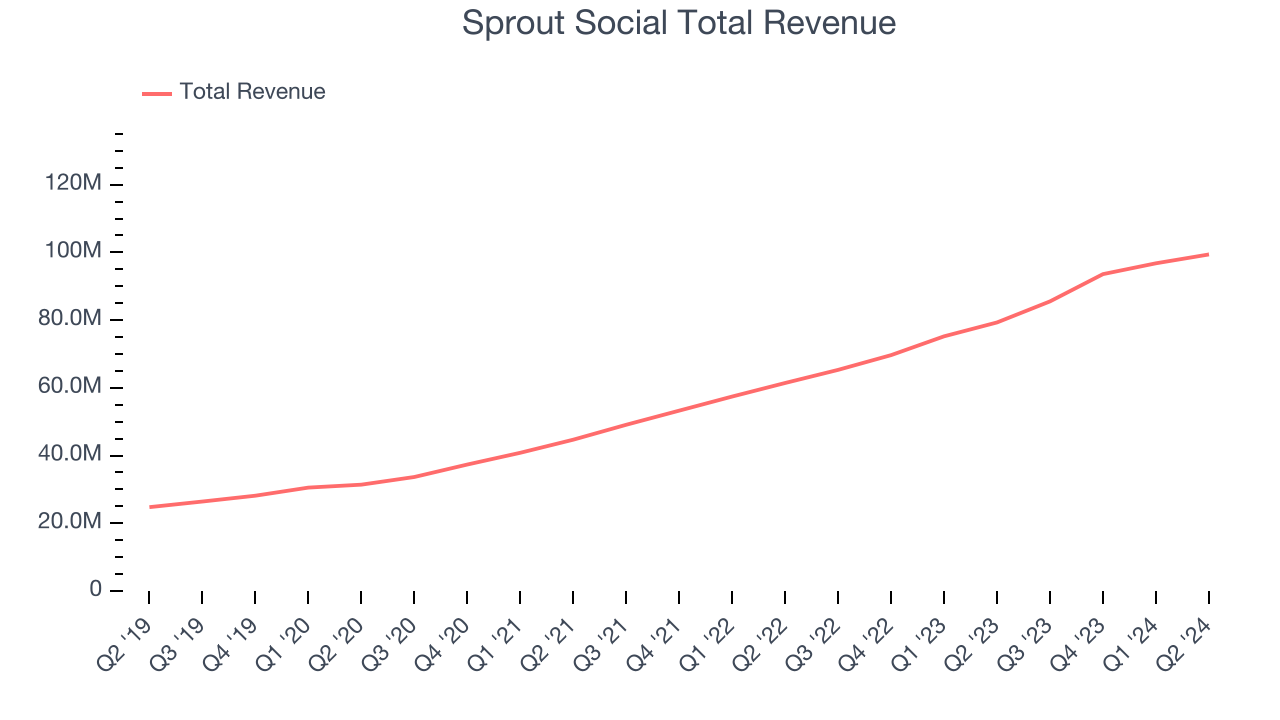

Sprout Social (NASDAQ:SPT)

Founded by Justyn Howard and Aaron Rankin in 2010, Sprout Social (NASDAQ:SPT) provides a software as a service platform that companies can use to schedule and respond to posts on major social media networks like Twitter, Facebook, Instagram, Youtube and LinkedIn.

Sprout Social reported revenues of $99.4 million, up 25.3% year on year. This print was in line with analysts’ expectations, and overall, it was a satisfactory quarter for the company with an impressive beat of analysts’ billings estimates but a miss of analysts’ ARR (annual recurring revenue) estimates.

“We’re pleased to share that we’re tracking ahead of the plan outlined last quarter,” said Ryan Barretto, President and incoming CEO.

The stock is down 23.9% since reporting and currently trades at $28.45.

Is now the time to buy Sprout Social? Access our full analysis of the earnings results here, it’s free.

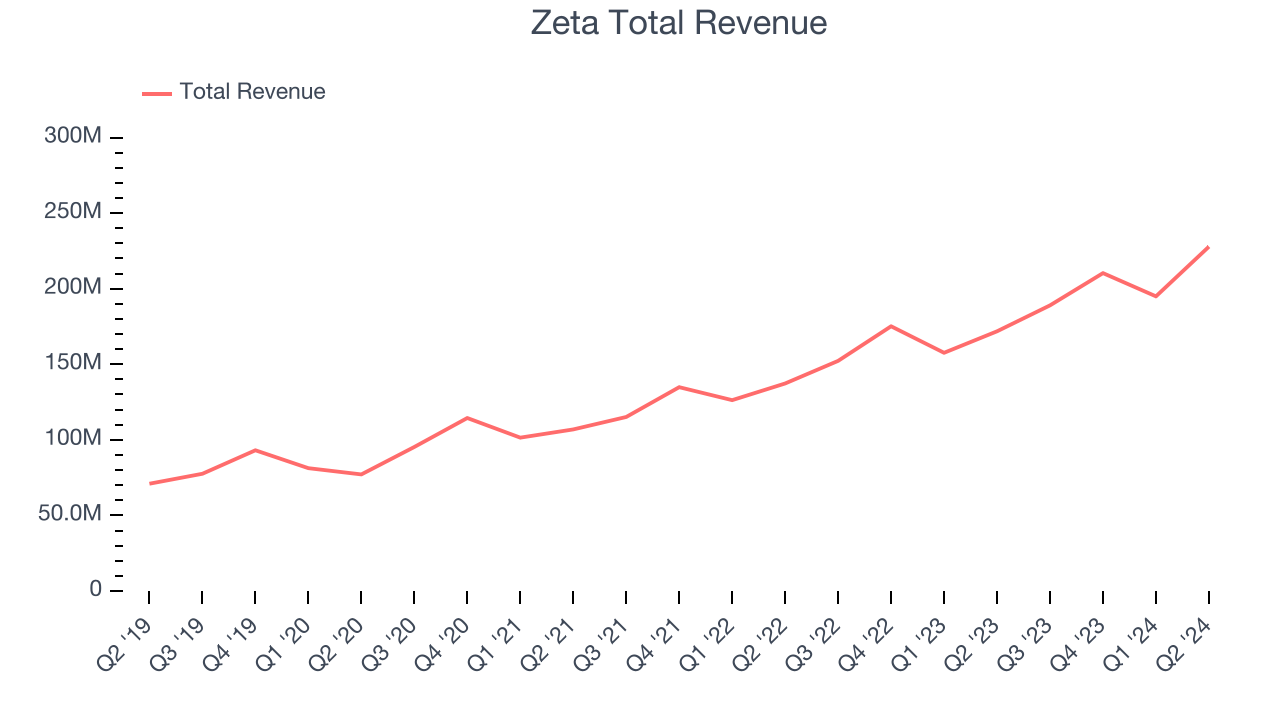

Best Q2: Zeta (NYSE:ZETA)

Co-founded by former Apple CEO John Scully, Zeta Global (NYSE:ZETA) provides software and data analytics tools that help companies market their products to billions of customers.

Zeta reported revenues of $227.8 million, up 32.6% year on year, outperforming analysts’ expectations by 7.2%. The business had an exceptional quarter with an impressive beat of analysts’ billings estimates and optimistic revenue guidance for the next quarter.

Zeta achieved the biggest analyst estimates beat among its peers. The market seems happy with the results as the stock is up 46.5% since reporting. It currently trades at $31.46.

Is now the time to buy Zeta? Access our full analysis of the earnings results here, it’s free.

Weakest Q2: PubMatic (NASDAQ:PUBM)

Founded in 2006 as an online ad platform helping ad sellers, Pubmatic (NASDAQ: PUBM) is a fully integrated cloud-based programmatic advertising platform.

PubMatic reported revenues of $67.27 million, up 6.2% year on year, falling short of analysts’ expectations by 4.1%. It was a disappointing quarter as it posted underwhelming revenue guidance for the next quarter.

As expected, the stock is down 26.1% since the results and currently trades at $14.49.

Read our full analysis of PubMatic’s results here.

HubSpot (NYSE:HUBS)

Started in 2006 by two MIT grad students, HubSpot (NYSE:HUBS) is a software-as-a-service platform that helps small and medium-sized businesses market themselves, sell, and get found on the internet.

HubSpot reported revenues of $637.2 million, up 20.4% year on year. This print topped analysts’ expectations by 2.9%. Overall, it was a satisfactory quarter as it also put up a decent beat of analysts’ billings estimates.

The company added 11,214 customers to reach a total of 228,054. The stock is up 15.4% since reporting and currently trades at $532.

Read our full, actionable report on HubSpot here, it’s free.

ON24 (NYSE:ONTF)

Started in 1998 as a platform to broadcast press conferences, ON24’s (NYSE:ONTF) software helps organizations organize online webinars and other virtual events and convert prospects into customers.

ON24 reported revenues of $37.35 million, down 11.3% year on year. This print surpassed analysts’ expectations by 3.2%. More broadly, it was a mixed quarter as it also logged full-year revenue guidance topping analysts’ expectations but a miss of analysts’ billings estimates.

ON24 had the slowest revenue growth among its peers. The stock is up 6.5% since reporting and currently trades at $6.21.

Read our full, actionable report on ON24 here, it’s free.

Join Paid Stock Investor Research

Help us make StockStory more helpful to investors like yourself. Join our paid user research session and receive a $50 Amazon gift card for your opinions. Sign up here.