Take-Two (TTWO): Buy, Sell, or Hold Post Q4 Earnings?

Jabin Bastian /

March 26, 2025

What a time it’s been for Take-Two. In the past six months alone, the company’s stock price has increased by a massive 41.2%, reaching $214.09 per share. This run-up might have investors contemplating their next move.

Is now the time to buy Take-Two, or should you be careful about including it in your portfolio? Get the full breakdown from our expert analysts, it’s free.

Despite the momentum, we're cautious about Take-Two. Here are three reasons why you should be careful with TTWO and a stock we'd rather own.

Why Is Take-Two Not Exciting?

Best known for its Grand Theft Auto and NBA 2K franchises, Take Two (NASDAQ:TTWO) is one of the world’s largest video game publishers.

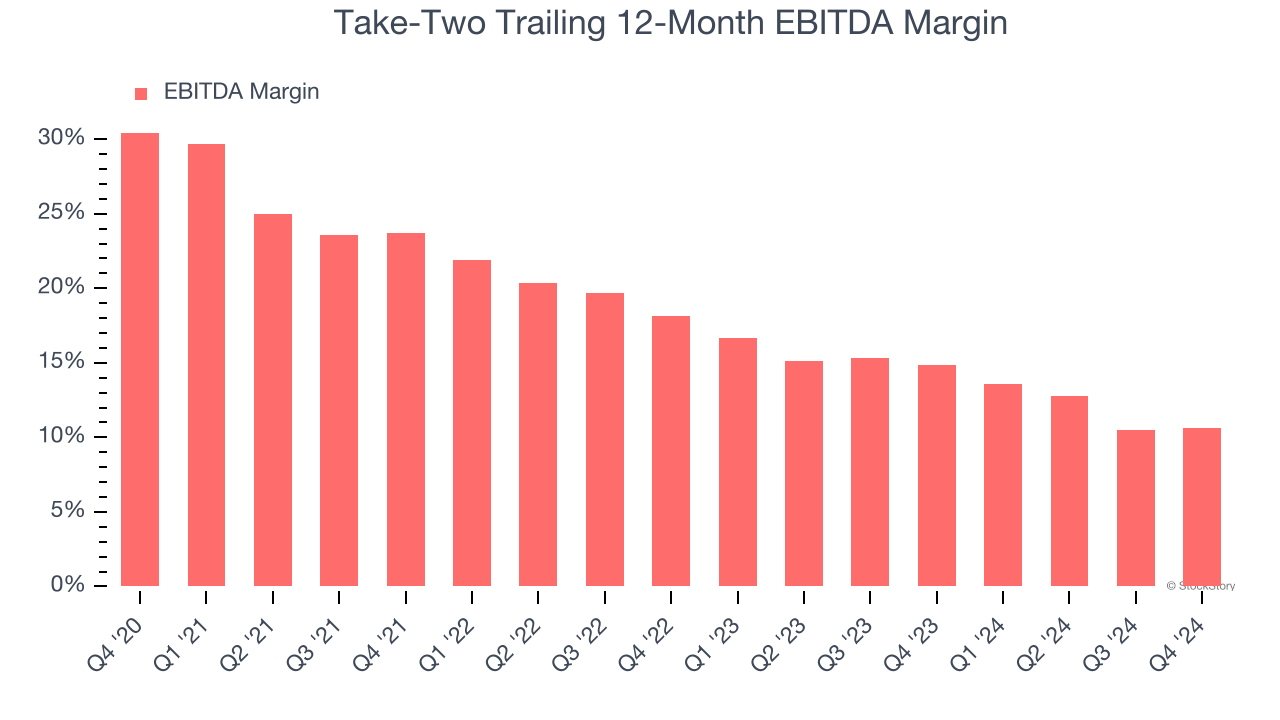

1. Shrinking EBITDA Margin

Operating income is often evaluated to assess a company’s underlying profitability. In a similar vein, EBITDA is used to analyze consumer internet companies because it excludes various one-time or non-cash expenses (depreciation), providing a clearer view of the business’s profit potential.

Analyzing the trend in its profitability, Take-Two’s EBITDA margin decreased by 13.1 percentage points over the last few years. This raises questions about the company’s expense base because its revenue growth should have given it leverage on its fixed costs, resulting in better economies of scale and profitability. Its EBITDA margin for the trailing 12 months was 10.7%.

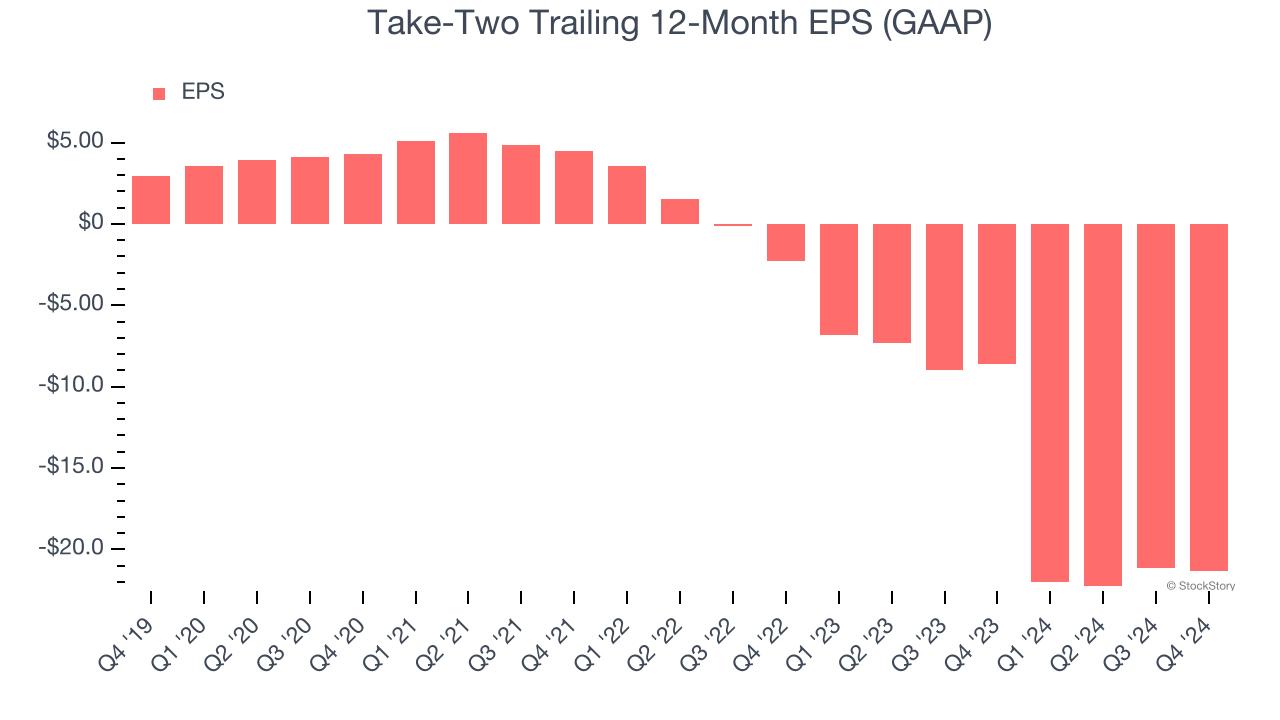

2. EPS Trending Down

Analyzing the change in earnings per share (EPS) shows whether a company's incremental sales were profitable – for example, revenue could be inflated through excessive spending on advertising and promotions.

Sadly for Take-Two, its EPS declined by 88.8% annually over the last three years while its revenue grew by 16.9%. This tells us the company became less profitable on a per-share basis as it expanded.

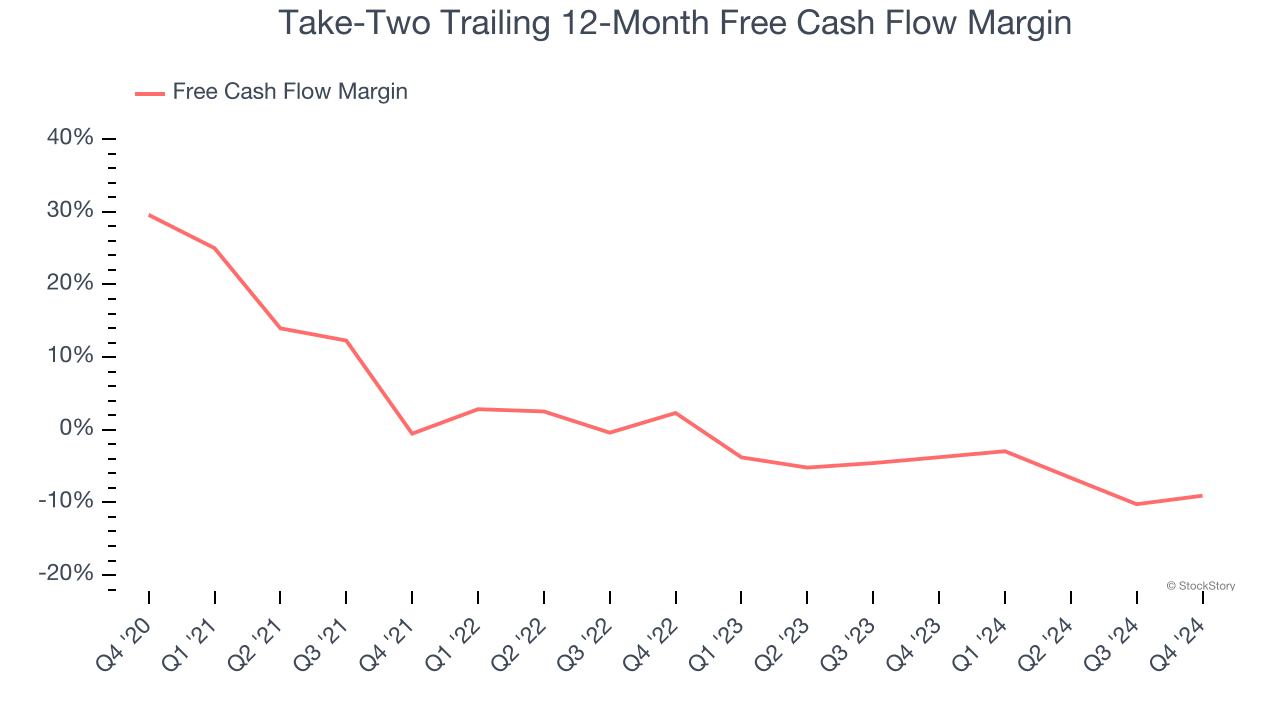

3. Cash Burn Ignites Concerns

Free cash flow isn't a prominently featured metric in company financials and earnings releases, but we think it's telling because it accounts for all operating and capital expenses, making it tough to manipulate. Cash is king.

Take-Two’s demanding reinvestments have consumed many resources over the last two years, contributing to an average free cash flow margin of negative 6.4%. This means it lit $6.44 of cash on fire for every $100 in revenue. This is a stark contrast from its EBITDA margin, and its investments (i.e., stocking inventory, building new facilities) are the primary culprit.

Final Judgment

Take-Two’s business quality ultimately falls short of our standards. Following the recent surge, the stock trades at 19.5× forward EV-to-EBITDA (or $214.09 per share). This valuation tells us a lot of optimism is priced in - we think there are better stocks to buy right now. Let us point you toward the most dominant software business in the world.

Stocks We Like More Than Take-Two

With rates dropping, inflation stabilizing, and the elections in the rearview mirror, all signs point to the start of a new bull run - and we’re laser-focused on finding the best stocks for this upcoming cycle.

Put yourself in the driver’s seat by checking out our Top 9 Market-Beating Stocks. This is a curated list of our High Quality stocks that have generated a market-beating return of 175% over the last five years.

Stocks that made our list in 2019 include now familiar names such as Nvidia (+2,183% between December 2019 and December 2024) as well as under-the-radar businesses like Comfort Systems (+751% five-year return). Find your next big winner with StockStory today for free.