Zoom (ZM) Surprises With Strong Q1, Provides Optimistic Guidance For Next Quarter

Radek Strnad /

June 1, 2021

Video conferencing platform Zoom (ZM) reported strong growth in the Q1 FY2022 earnings announcement, with revenue up 191% year on year to $956.2 million. Zoom made a GAAP profit of $227.5 million, improving on its profit of $27 million, in the same quarter last year.

What do these results signal for the future of Zoom? Get early access our full analysis here

Zoom (ZM) Q1 FY2022 Highlights:

- Revenue: $956.2 million vs analyst estimates of $908.1 million (5.29% beat)

- EPS (non-GAAP): $1.32 vs analyst estimates of $0.98 (34.5% beat)

- Revenue guidance for Q2 2022 is $987.5 million at the midpoint, above analyst estimates of $933.4 million

- The company lifted revenue guidance for the full year, from $3.77 billion to $3.98 billion at the midpoint, a 5.63% increase

- Free cash flow of $454.2 million, up 20.1% from previous quarter

- Net Revenue Retention Rate: 130%, in line with previous quarter

- Customers: 497,000 customers with more than 10 employees

- Gross Margin (GAAP): 72.2%, up from 69.7% previous quarter

- Updated valuation: Zoom is flat at $327.4 and accounting for the revenue added in Q1 now trades at 30.5x price-to-sales (LTM), compared to 37.1x just before the results.

“We kicked off the fiscal year with a very strong first quarter, posting 191% total year-over-year revenue growth combined with strong profitability and cash flow. Our steadfast commitment to empowering customers to work and learn from anywhere with our expansive, innovative, and frictionless video communications platform continued to drive our results. With this solid start, we are pleased to raise our total guidance range to $3.975 billion to $3.990 billion for the full fiscal year,” said Zoom founder and CEO, Eric S. Yuan.

Zoom: User Experience as a Moat

Started in 2011 by Eric Yuan who once ran engineering for Cisco’s video conferencing business, Zoom become a household name during the Covid pandemic. It offers an easy to use, cloud-based platform for video conferencing, audio conferencing and screen sharing. Today it's used not only for business meetings but also by teachers to conduct classes, by developers to write code together, and by lawyers in court (even though sometimes they might end up looking like a cat).

Zoom didn’t invent video conferencing, it just made it a lot less painful. The platform works reasonably well even on a spotty internet connection, is easy to use, cheap and works across mobile and desktop. The company is notoriously customer obsessed and Yuan, the CEO has been known to personally write to disgruntled users for feedback. And that is important because there is a lot of competition in the video conferencing space from products like Google Meet, Microsoft Teams, Cisco Webex or upcoming startups like Around.co and Zoom is under pressure to keep one step ahead. But it is likely that remote and hybrid models of work are here to stay and video conferencing tools are the clear beneficiaries of it.

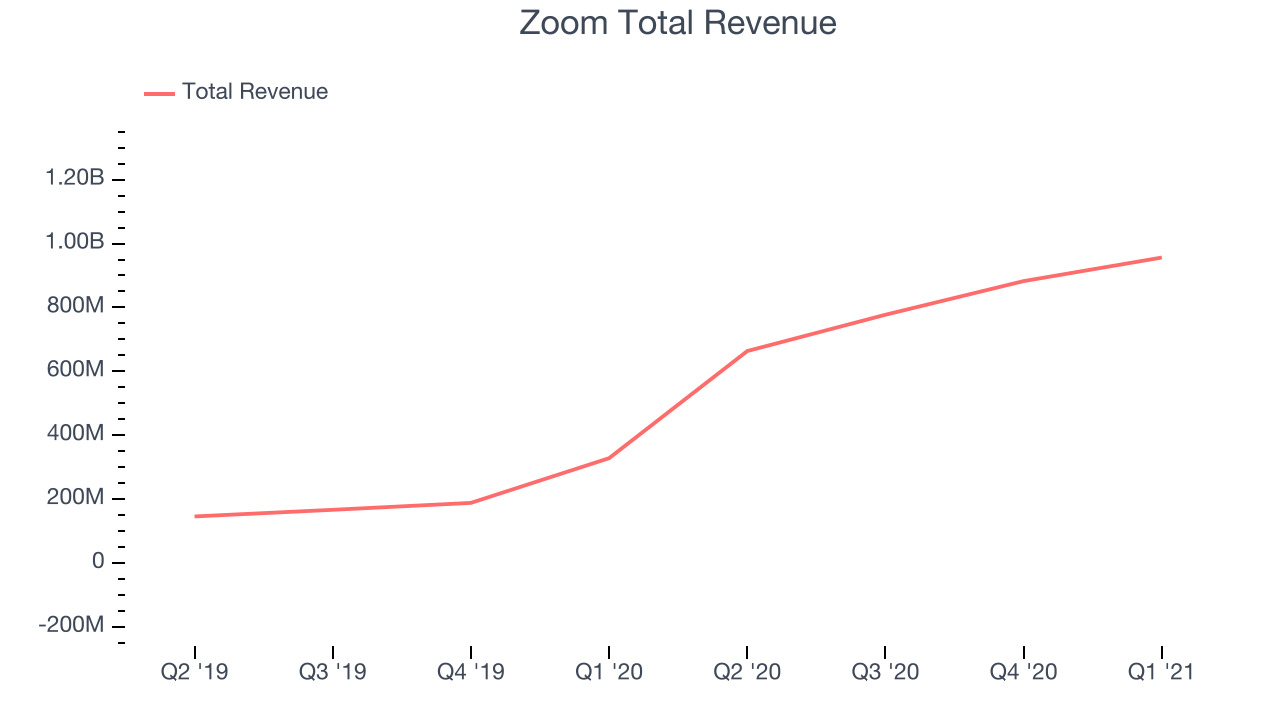

As you can see below, Zoom's revenue growth has been incredible over the last twelve months, growing from $328.1 million to $956.2 million.

And while we saw even higher rates of growth previously, the revenue growth was still very strong; up a rather splendid 191% year on year. But the growth did slow down compared to last quarter, as the revenue increased by just $73.7 million in Q1, compared to $105.2 million in Q4 2021. So while the growth is overall still impressive, we will be keeping an eye on the slowdown.

There are others doing even better. Founded by ex-Google engineers, a small company making software for banks has been growing revenue 80% year on year and is already up more than 400% since the IPO in December. You can find it on our platform for free.

Go-To-Market

Zoom is using a freemium model to attract customers and offers their limited basic plan for free, which has helped accelerate their user growth.

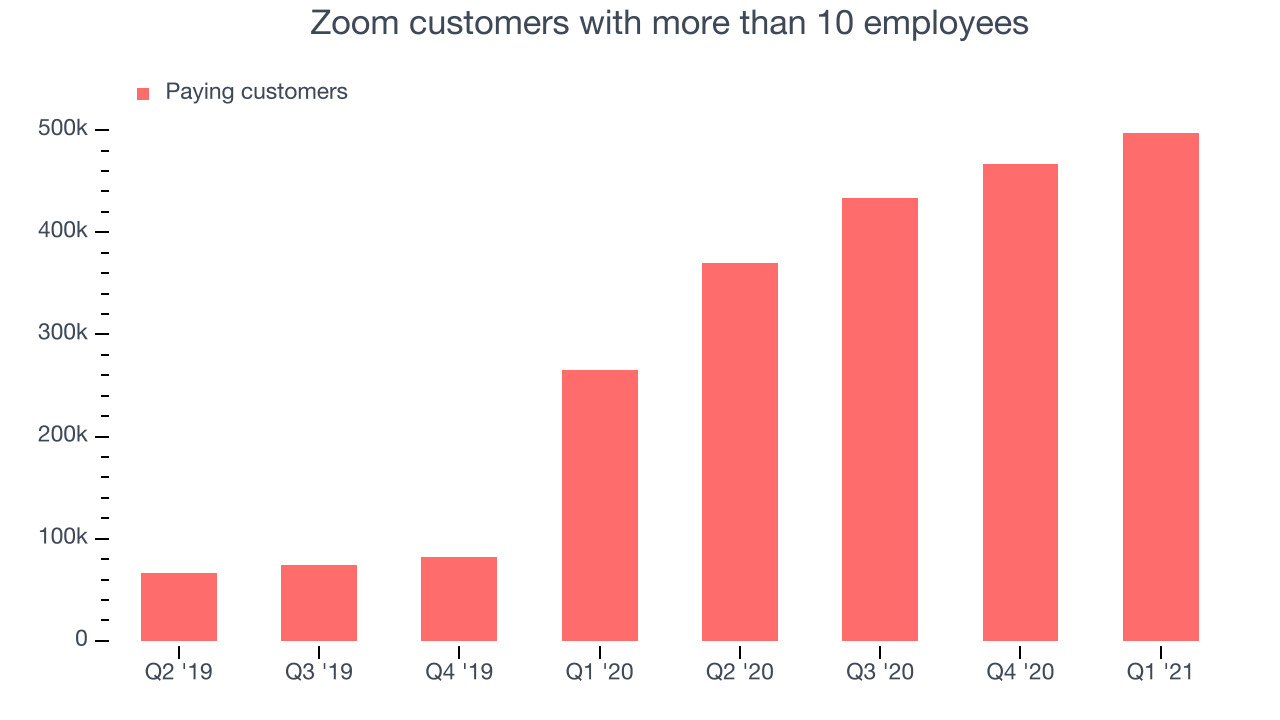

You can see below that at the end of the quarter Zoom reported 497,000 enterprise customers with more than 10 employees, an increase of 29,900 on last quarter. That is a bit less contract wins than last quarter and also quite a bit below what we have typically seen over the past couple of quarters, suggesting that the sales momentum with large customers is slowing down.

Key Takeaways from Zoom's Q1 Results

Sporting a market capitalisation of $97.6 billion, more than $4.68 billion in cash and operating free cash flow positive over the last twelve months, we're confident that Zoom has the resources it needs to pursue a high growth business strategy.

We were impressed by the exceptional revenue growth Zoom delivered this quarter. And we were also glad that the revenue guidance for the next quarter exceeded analysts' expectations. On the other hand, there was a slight slowdown in new contract wins. Zooming out, we think this was a fantastic quarter that should have shareholders cheering. While the market has high expectations of Zoom we think it will continue to stand out as one of the best quality SaaS stocks, even more so than before.

PS. If you found this analysis useful, you will love our earnings alerts! We publish so fast, you often have the opportunity to buy or sell before the market has fully absorbed the information. Never miss out on the right time to invest again. Signup here for free early access.

The author has no position in any of the stocks mentioned.