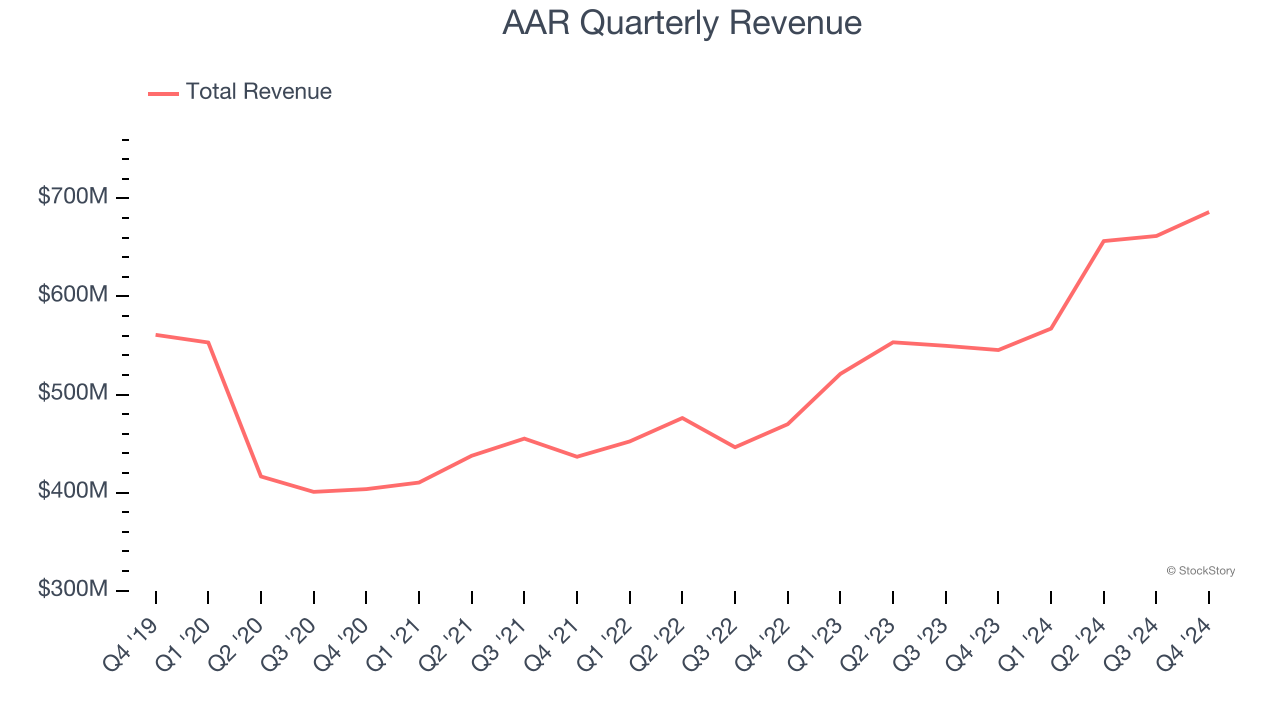

Aviation and defense services provider AAR CORP (NYSE:AIR) reported Q4 CY2024 results beating Wall Street’s revenue expectations, with sales up 25.8% year on year to $686.1 million. Its non-GAAP profit of $0.90 per share was 6.9% above analysts’ consensus estimates.

Is now the time to buy AAR? Find out in our full research report.

AAR (AIR) Q4 CY2024 Highlights:

- Revenue: $686.1 million vs analyst estimates of $654.1 million (25.8% year-on-year growth, 4.9% beat)

- Adjusted EPS: $0.90 vs analyst estimates of $0.84 (6.9% beat)

- Adjusted EBITDA: $78.4 million vs analyst estimates of $73.81 million (11.4% margin, 6.2% beat)

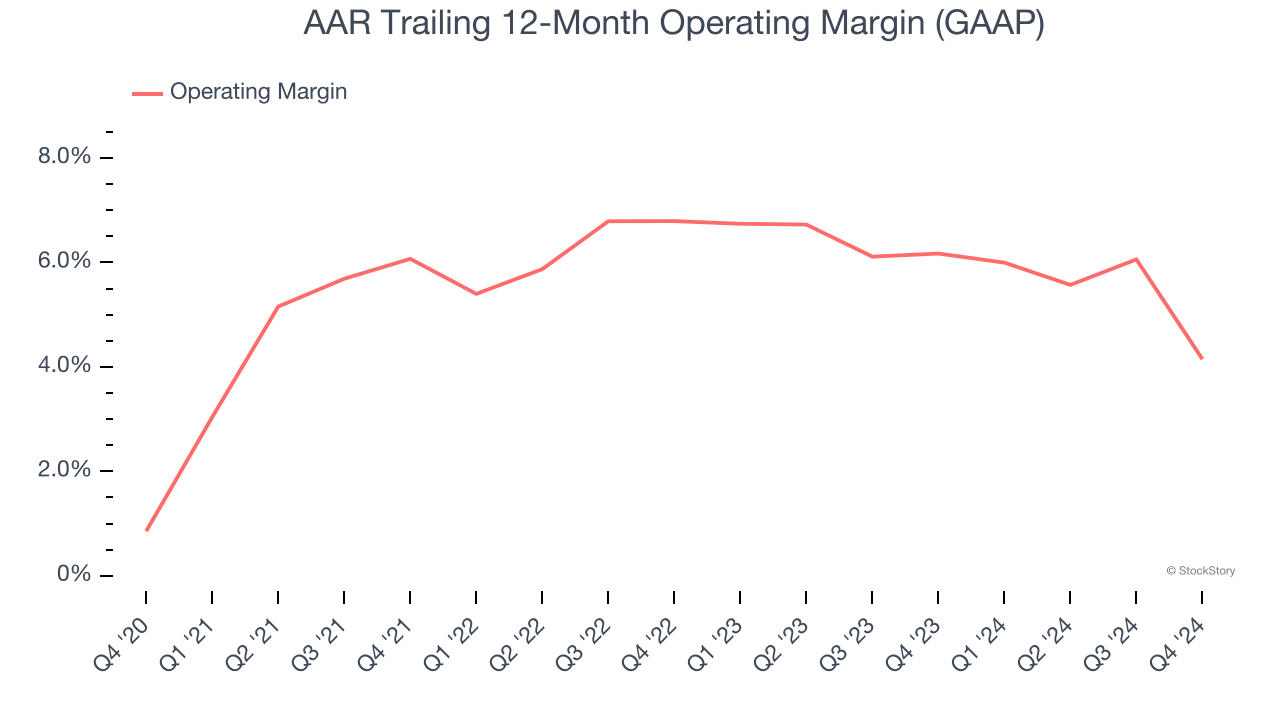

- Operating Margin: -0.3%, down from 7% in the same quarter last year

- Free Cash Flow Margin: 2%, similar to the same quarter last year

- Market Capitalization: $2.19 billion

"AAR delivered another solid quarter with record sales and improved margins," said John M. Holmes, AAR's Chairman, President and Chief Executive Officer.

Company Overview

The first third-party MRO approved by the FAA for Safety Management System Requirements, AAR (NYSE:AIR) is a provider of aircraft maintenance services

Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Sales Growth

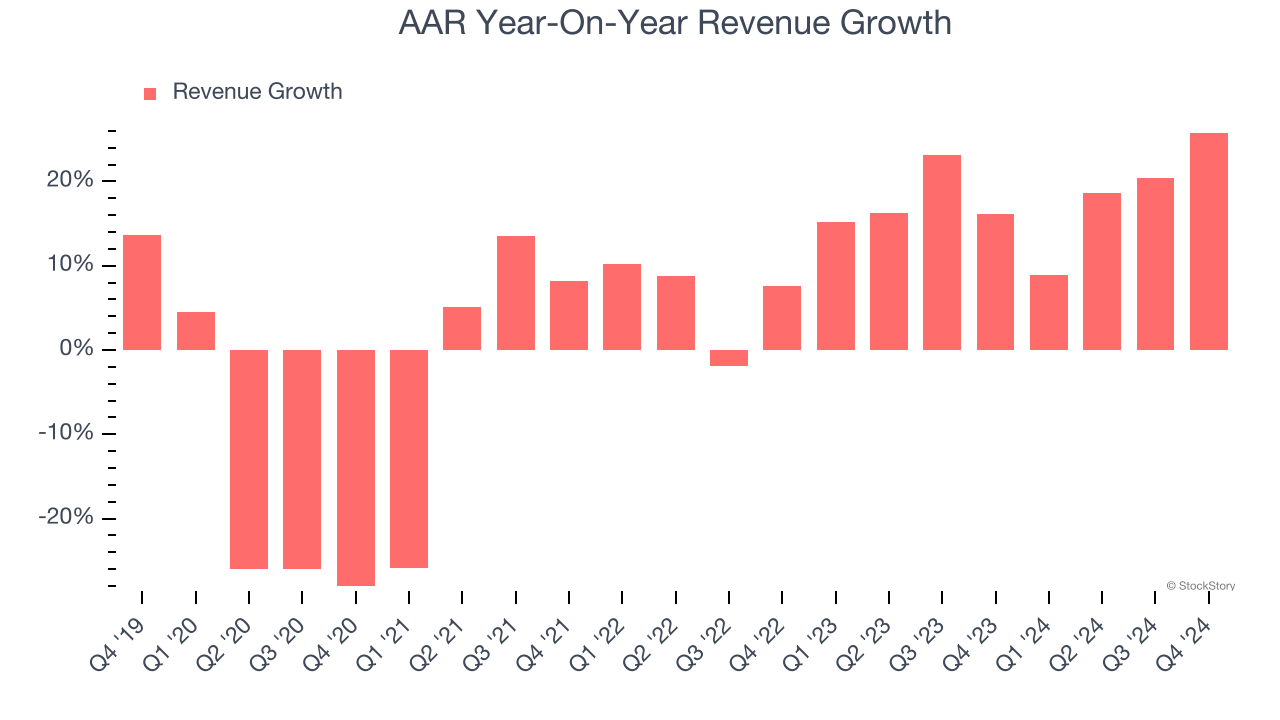

A company’s long-term sales performance can indicate its overall quality. Any business can put up a good quarter or two, but many enduring ones grow for years. Unfortunately, AAR’s 3.2% annualized revenue growth over the last five years was sluggish. This fell short of our benchmark for the industrials sector, but there are still things to like about AAR.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. AAR’s annualized revenue growth of 18.1% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

AAR also breaks out the revenue for its three most important segments: Parts Supply, Repair & Engineering, and Integrated Solutions, which are 39.9%, 33.3%, and 23.8% of revenue. Over the last two years, AAR’s revenues in all three segments increased. Its Parts Supply revenue (engine and airframe parts) averaged year-on-year growth of 17.6% while its Repair & Engineering (maintenance, repair, and overhaul services) and Integrated Solutions (fleet management) revenues averaged 32.1% and 13.9%.

This quarter, AAR reported robust year-on-year revenue growth of 25.8%, and its $686.1 million of revenue topped Wall Street estimates by 4.9%.

Looking ahead, sell-side analysts expect revenue to grow 9.3% over the next 12 months, a deceleration versus the last two years. Despite the slowdown, this projection is healthy and implies the market sees success for its products and services.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) stock benefiting from the rise of AI. Click here to access our free report one of our favorites growth stories.

Operating Margin

AAR was profitable over the last five years but held back by its large cost base. Its average operating margin of 4.8% was weak for an industrials business.

On the plus side, AAR’s operating margin rose by 3.3 percentage points over the last five years.

This quarter, AAR’s breakeven margin was down 7.4 percentage points year on year. This contraction shows it was recently less efficient because its expenses grew faster than its revenue.

Earnings Per Share

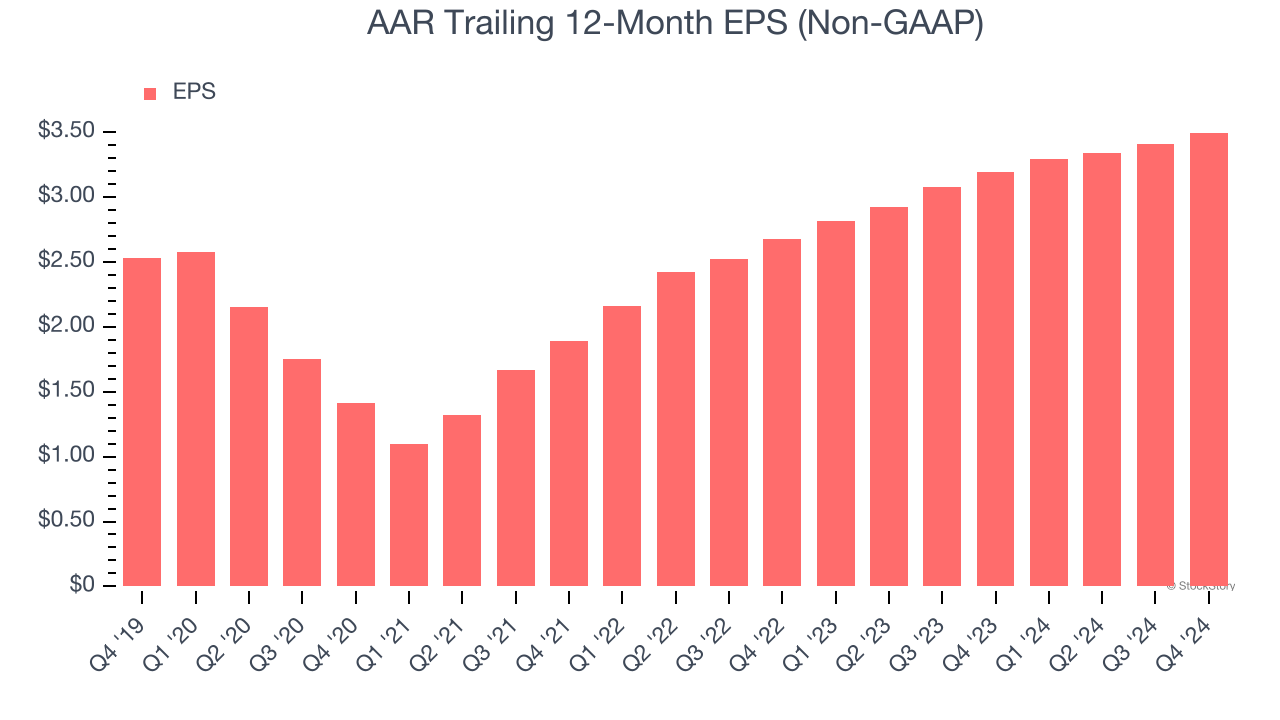

We track the long-term change in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company’s growth is profitable.

AAR’s EPS grew at an unimpressive 6.7% compounded annual growth rate over the last five years. On the bright side, this performance was better than its 3.2% annualized revenue growth and tells us the company became more profitable on a per-share basis as it expanded.

Diving into the nuances of AAR’s earnings can give us a better understanding of its performance. As we mentioned earlier, AAR’s operating margin declined this quarter but expanded by 3.3 percentage points over the last five years. This was the most relevant factor (aside from the revenue impact) behind its higher earnings; taxes and interest expenses can also affect EPS but don’t tell us as much about a company’s fundamentals.

Like with revenue, we analyze EPS over a shorter period to see if we are missing a change in the business.

For AAR, its two-year annual EPS growth of 14.2% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.In Q4, AAR reported EPS at $0.90, up from $0.82 in the same quarter last year. This print beat analysts’ estimates by 6.9%. Over the next 12 months, Wall Street expects AAR’s full-year EPS of $3.50 to grow 17.3%.

Key Takeaways from AAR’s Q4 Results

We were impressed by how significantly AAR blew past analysts’ revenue expectations this quarter. We were also glad its EBITDA outperformed Wall Street’s estimates. Zooming out, we think this quarter featured some important positives. The stock traded up 5.2% to $65.03 immediately following the results.

AAR may have had a good quarter, but does that mean you should invest right now? If you’re making that decision, you should consider the bigger picture of valuation, business qualities, as well as the latest earnings. We cover that in our actionable full research report which you can read here, it’s free.