Alta (NYSE:ALTG) Misses Q2 Sales Targets

Max Juang /

August 7, 2024

Equipment distribution company Alta Equipment Group (NYSE:ALTG) fell short of analysts' expectations in Q2 CY2024, with revenue up 4.2% year on year to $488.1 million. It made a non-GAAP profit of $0.01 per share, down from its profit of $0.19 per share in the same quarter last year.

Is now the time to buy Alta? Find out in our full research report.

Alta (ALTG) Q2 CY2024 Highlights:

- Revenue: $488.1 million vs analyst estimates of $505.5 million (3.4% miss)

- EPS (non-GAAP): $0.01 vs analyst estimates of $0.19 (-$0.18 miss)

- Gross Margin (GAAP): 27%, in line with the same quarter last year

- EBITDA Margin: 10.3%, in line with the same quarter last year

- Free Cash Flow was -$29.6 million compared to -$29.2 million in the previous quarter

- Market Capitalization: $289.7 million

LIVONIA, Mich., Aug. 07, 2024 (GLOBE NEWSWIRE) -- Alta Equipment Group Inc. (NYSE: ALTG) (“Alta”, "we", "our" or the “Company”), a leading provider of premium material handling, construction and environmental processing equipment and related services, today announced financial results for the second quarter ended June 30, 2024.

Founded in 1984, Alta Equipment Group (NYSE:ALTG) is a provider of industrial and construction equipment and services across the Midwest and Northeast United States.

Specialty Equipment Distributors

Historically, specialty equipment distributors have boasted deep selection and expertise in sometimes narrow areas like single-use packaging or unique lighting equipment. Additionally, the industry has evolved to include more automated industrial equipment and machinery over the last decade, driving efficiencies and enabling valuable data collection. Specialty equipment distributors whose offerings keep up with these trends can take share in a still-fragmented market, but like the broader industrials sector, this space is at the whim of economic cycles that impact the capital spending and manufacturing propelling industry volumes.

Sales Growth

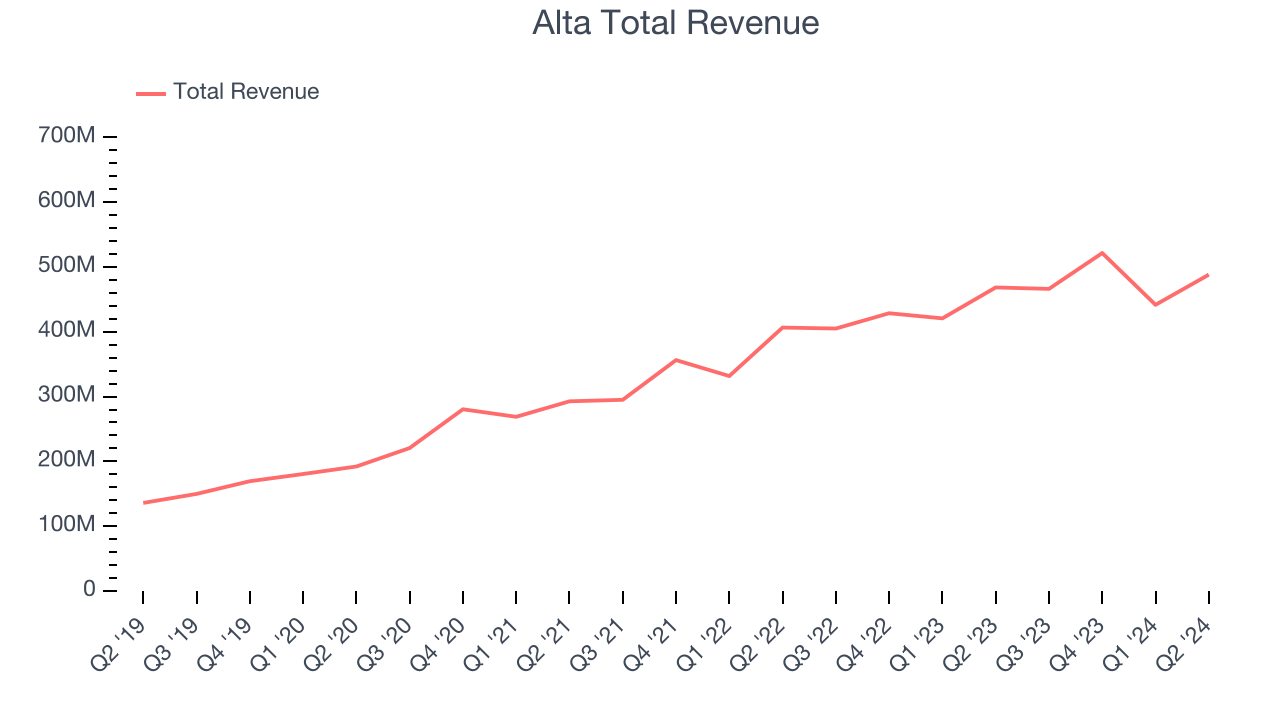

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Over the last five years, Alta grew its sales at an incredible 32.6% compounded annual growth rate. This is encouraging because it shows Alta's offerings resonate with customers, a helpful starting point.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Alta's annualized revenue growth of 17.5% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

This quarter, Alta's revenue grew 4.2% year on year to $488.1 million, falling short of Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 6.2% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

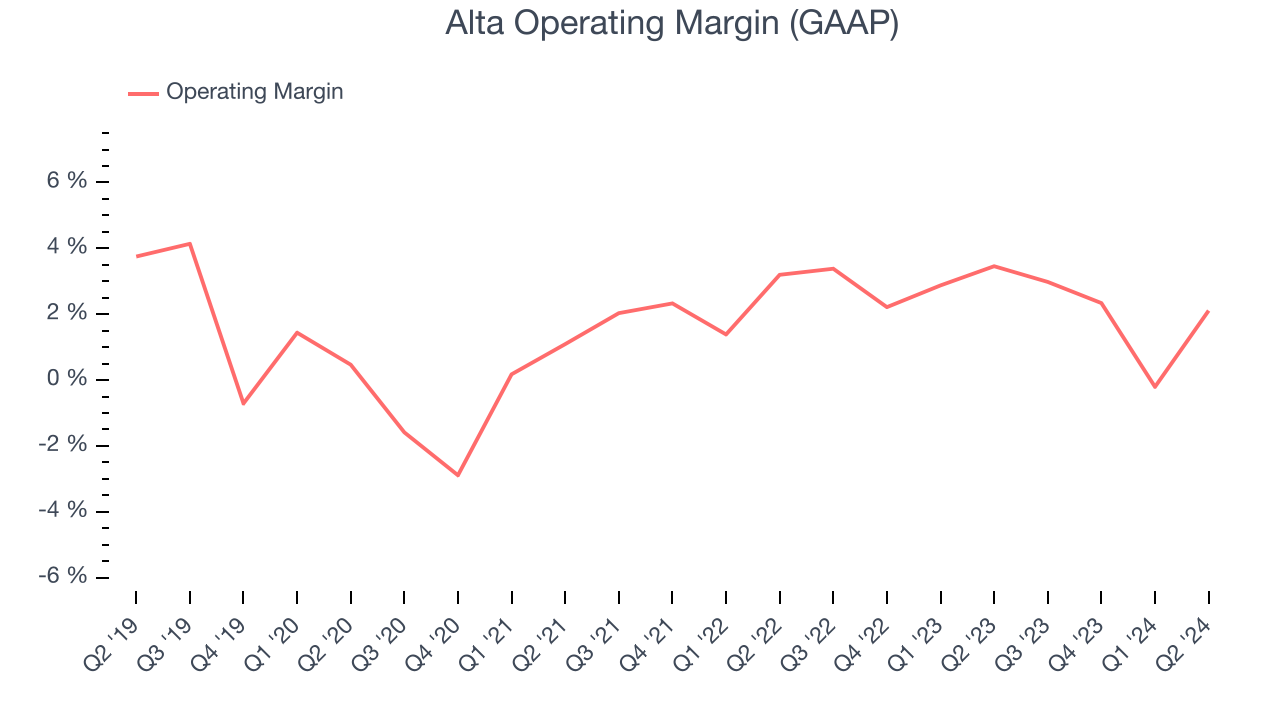

Alta was profitable over the last five years but held back by its large expense base. It demonstrated lousy profitability for an industrials business, producing an average operating margin of 1.8%. This result isn't too surprising given its low gross margin as a starting point.

Looking at the trend in its profitability, Alta's annual operating margin might have seen some fluctuations but has remained more or less the same over the last five years, which doesn't help its cause.

This quarter, Alta generated an operating profit margin of 2.1%, down 1.3 percentage points year on year. Since Alta's operating margin decreased more than its gross margin, we can assume the company was recently less efficient because expenses such as sales, marketing, R&D, and administrative overhead increased.

EPS

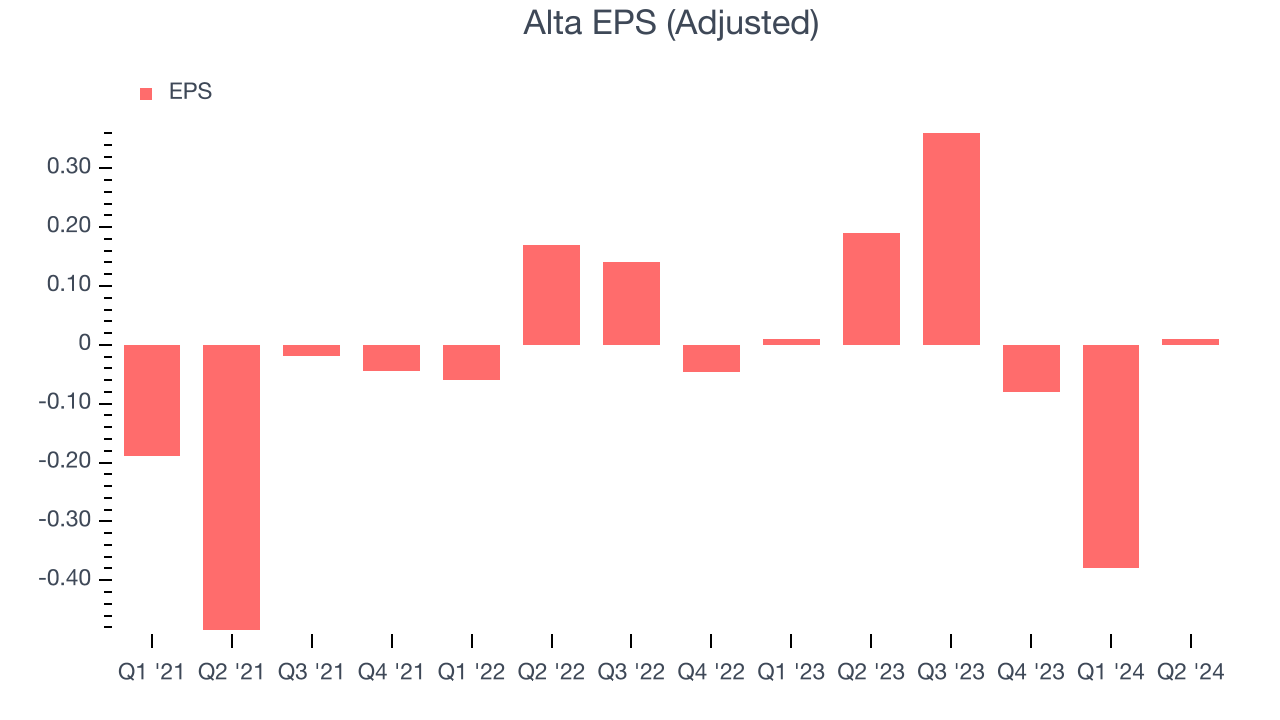

Analyzing revenue trends tells us about a company's historical growth, but earnings per share (EPS) growth points to the profitability of that growth–for example, a company could inflate sales through excessive spending on advertising and promotions.

Sadly for Alta, its EPS declined by 97.9% annually over the last two years while its revenue grew 17.5%. This tells us the company became less profitable on a per-share basis as it expanded.

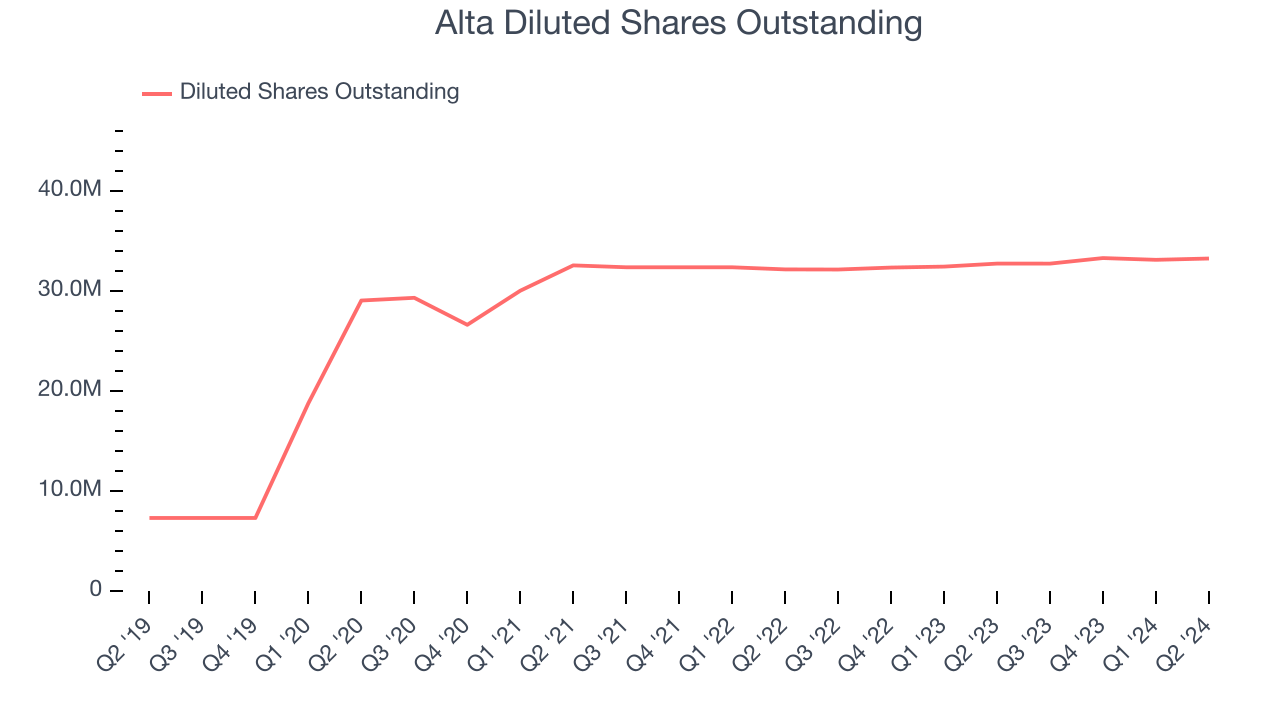

Diving into the nuances of Alta's earnings can give us a better understanding of its performance. Alta's operating margin has declined 1.1 percentage points over the last two years while its share count has grown 3.4%. This means the company not only became less efficient with its operating expenses but also diluted its shareholders.

In Q2, Alta reported EPS at $0.01, down from $0.19 in the same quarter last year. This print missed analysts' estimates, but we care more about long-term EPS growth than short-term movements. We also like to analyze expected EPS growth based on Wall Street analysts' consensus projections, but there is insufficient data.

Key Takeaways from Alta's Q2 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its EPS fell short of Wall Street's estimates. Overall, this was a weaker quarter for Alta. The stock remained flat at $8.19 immediately after reporting.

So should you invest in Alta right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.