Boeing (NYSE:BA) Misses Q2 Sales Targets, Names New CEO

Kayode Omotosho /

July 31, 2024

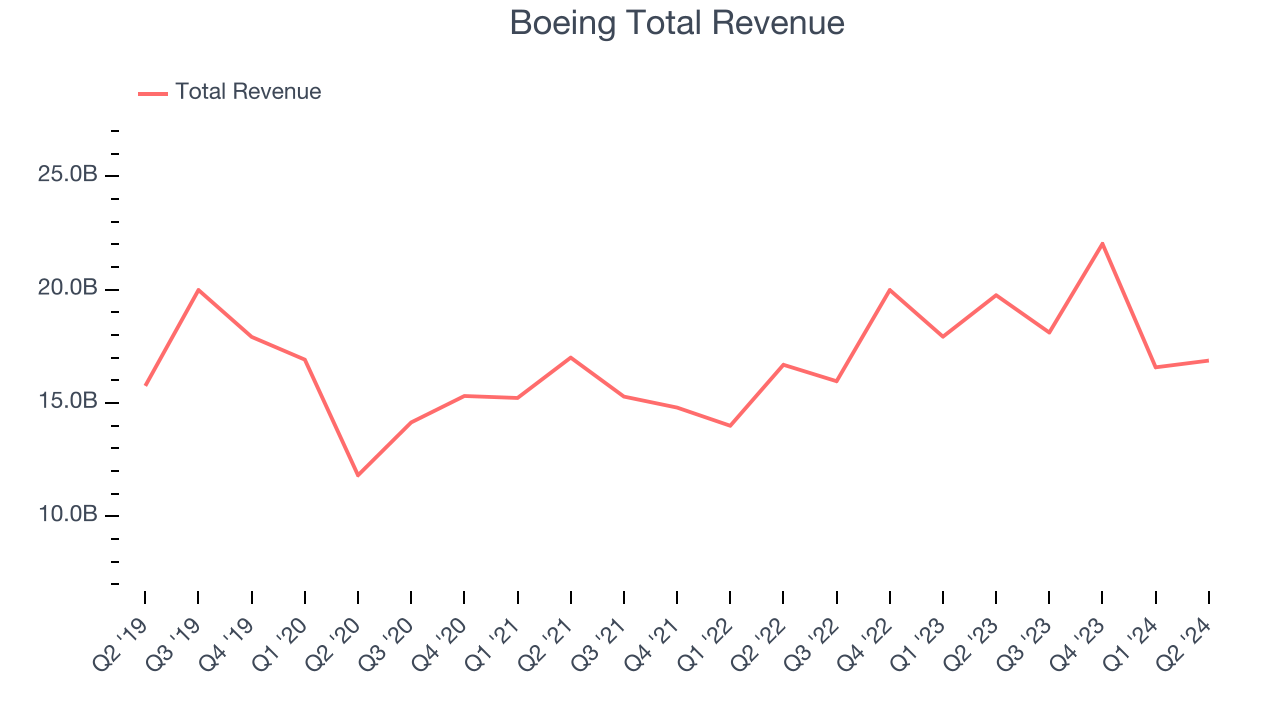

Aerospace and defense company Boeing (NYSE:BA) fell short of analysts' expectations in Q2 CY2024, with revenue down 14.6% year on year to $16.87 billion. It made a non-GAAP loss of $2.90 per share, down from its loss of $0.82 per share in the same quarter last year.

Is now the time to buy Boeing? Find out in our full research report.

Boeing (BA) Q2 CY2024 Highlights:

- Boeing has named Robert “Kelly” Ortberg as CEO to succeed Dave Calhoun; Ortberg previously led aerospace supplier Rockwell Collins

- Revenue: $16.87 billion vs analyst estimates of $17.35 billion (2.8% miss)

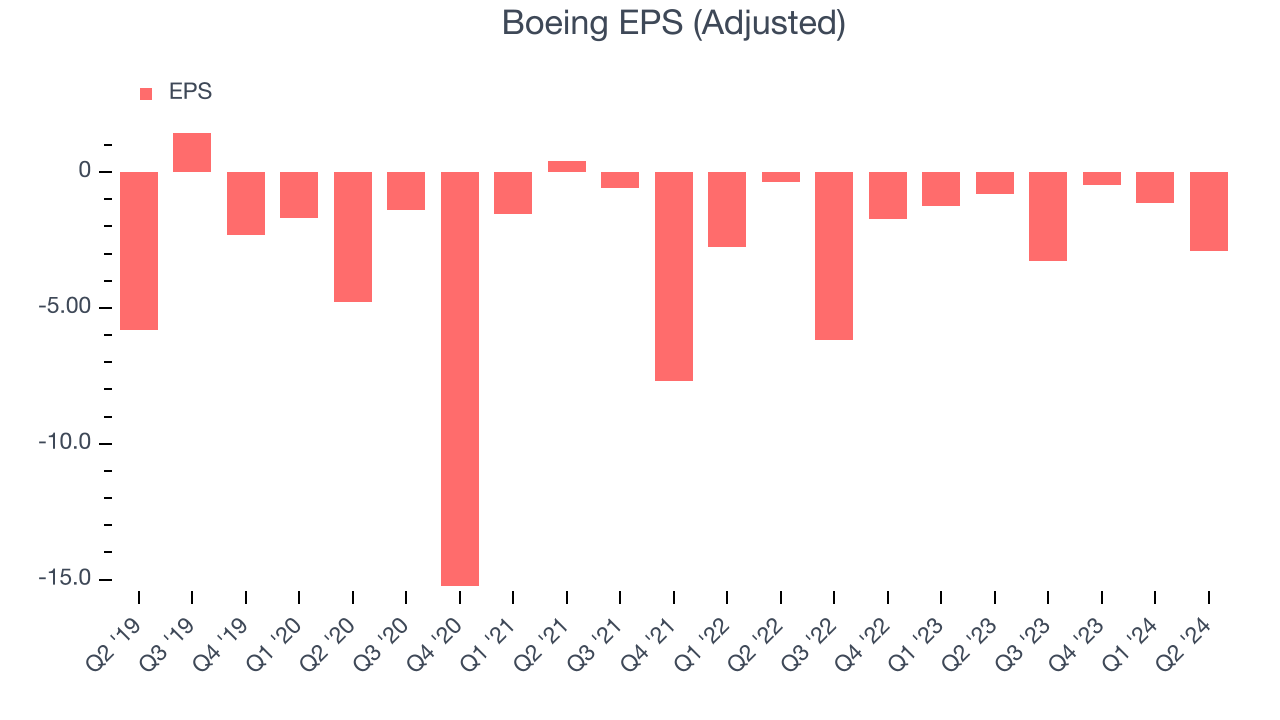

- EPS (non-GAAP): -$2.90 vs analyst estimates of -$2.01

- "Despite a challenging quarter, we are making substantial progress strengthening our quality management system and positioning our company for the future...We are executing on our comprehensive safety and quality plan and have reached an agreement to acquire Spirit AeroSystems."

- Gross Margin (GAAP): 7.3%, down from 12.1% in the same quarter last year

- Free Cash Flow was -$4.33 billion compared to -$3.93 billion in the previous quarter

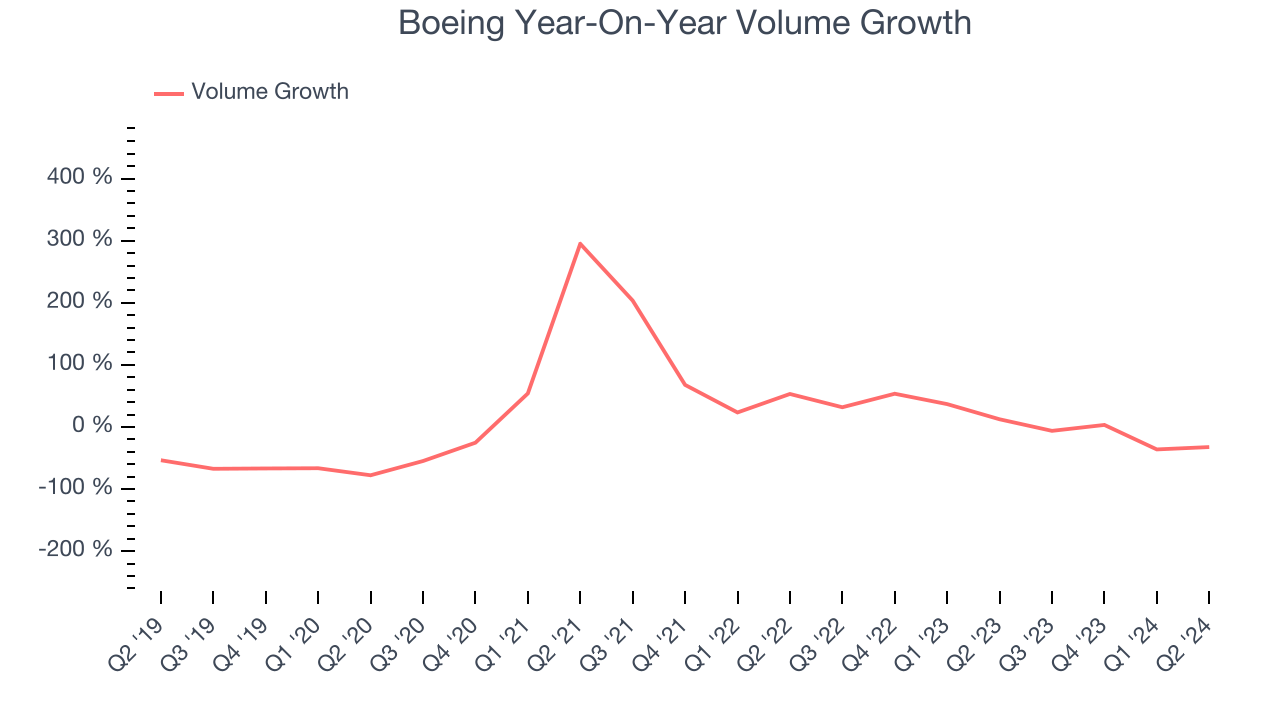

- Sales Volumes fell 32.4% year on year (12.4% in the same quarter last year)

- Market Capitalization: $115 billion

"Despite a challenging quarter, we are making substantial progress strengthening our quality management system and positioning our company for the future," said Dave Calhoun, Boeing president and chief executive officer.

One of the companies that forms a duopoly in the commercial aircraft market, Boeing (NYSE:BA) develops, manufactures, and services commercial airplanes, defense products, and space systems.

Aerospace

Aerospace companies often possess technical expertise and have made significant capital investments to produce complex products. It is an industry where innovation is important, and lately, emissions and automation are in focus, so companies that boast advances in these areas can take market share. On the other hand, demand for aerospace products can ebb and flow with economic cycles and geopolitical tensions, which can be particularly painful for companies with high fixed costs.

Sales Growth

Reviewing a company's long-term performance can reveal insights into its business quality. Any business can have short-term success, but a top-tier one tends to sustain growth for years. Over the last five years, Boeing's revenue declined by 4.4% per year. This shows demand was weak, a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Boeing's annualized revenue growth of 10% over the last two years is above its five-year trend, suggesting its demand recently accelerated.

Boeing also reports its sales volumes, which reached 92 in the latest quarter. Over the last two years, Boeing's sales volumes averaged 7.9% year-on-year growth. Because this number is lower than its revenue growth, we can see the company benefited from price increases.

This quarter, Boeing missed Wall Street's estimates and reported a rather uninspiring 14.6% year-on-year revenue decline, generating $16.87 billion of revenue. Looking ahead, Wall Street expects sales to grow 19.7% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Operating Margin

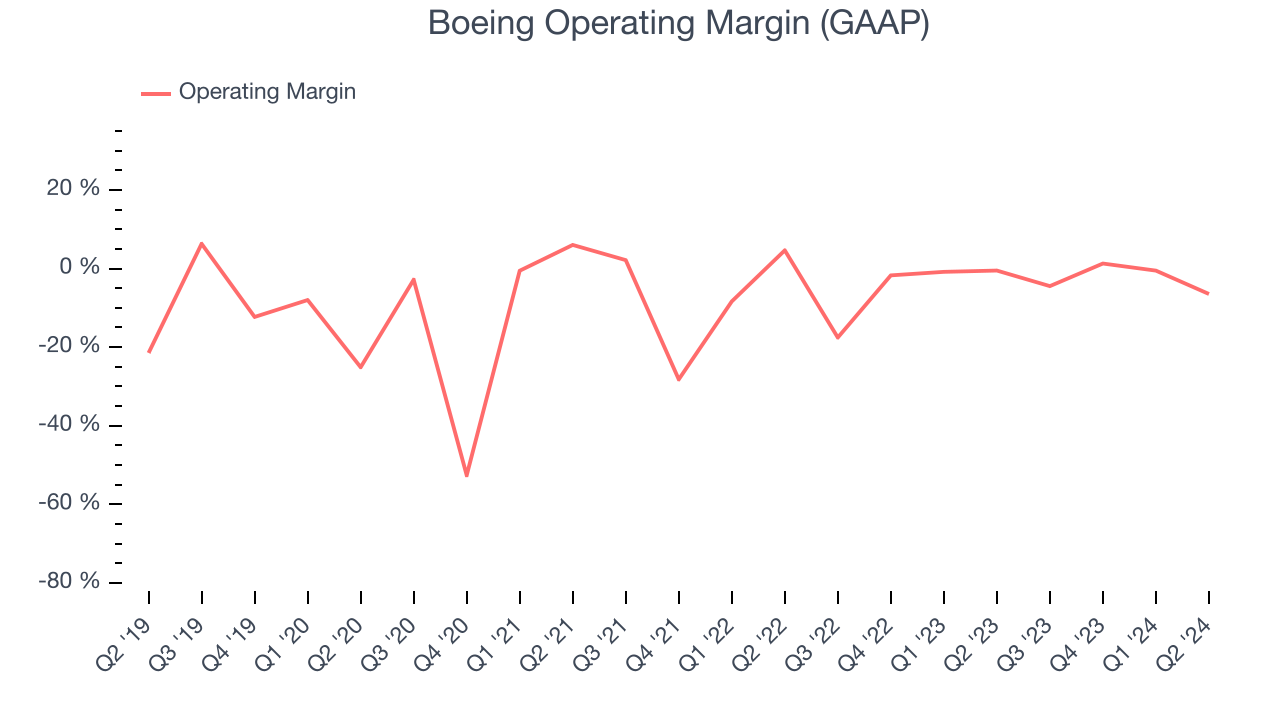

Unprofitable industrials companies require extra attention because they could get caught swimming naked if the tide goes out. It's hard to trust that Boeing can endure a full cycle as its high expenses have contributed to an average operating margin of negative 6.6% over the last five years.

On the bright side, Boeing's annual operating margin rose by 5.6 percentage points over the last five years. Still, it will take much more for the company to reach long-term profitability.

This quarter, Boeing generated an operating profit margin of negative 6.5%, down 6 percentage points year on year. This contraction shows it was recently less efficient because its expenses increased relative to its revenue.

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Sadly for Boeing, its EPS declined more than its revenue over the last five years, dropping by 26.3% annually. However, its operating margin actually expanded during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

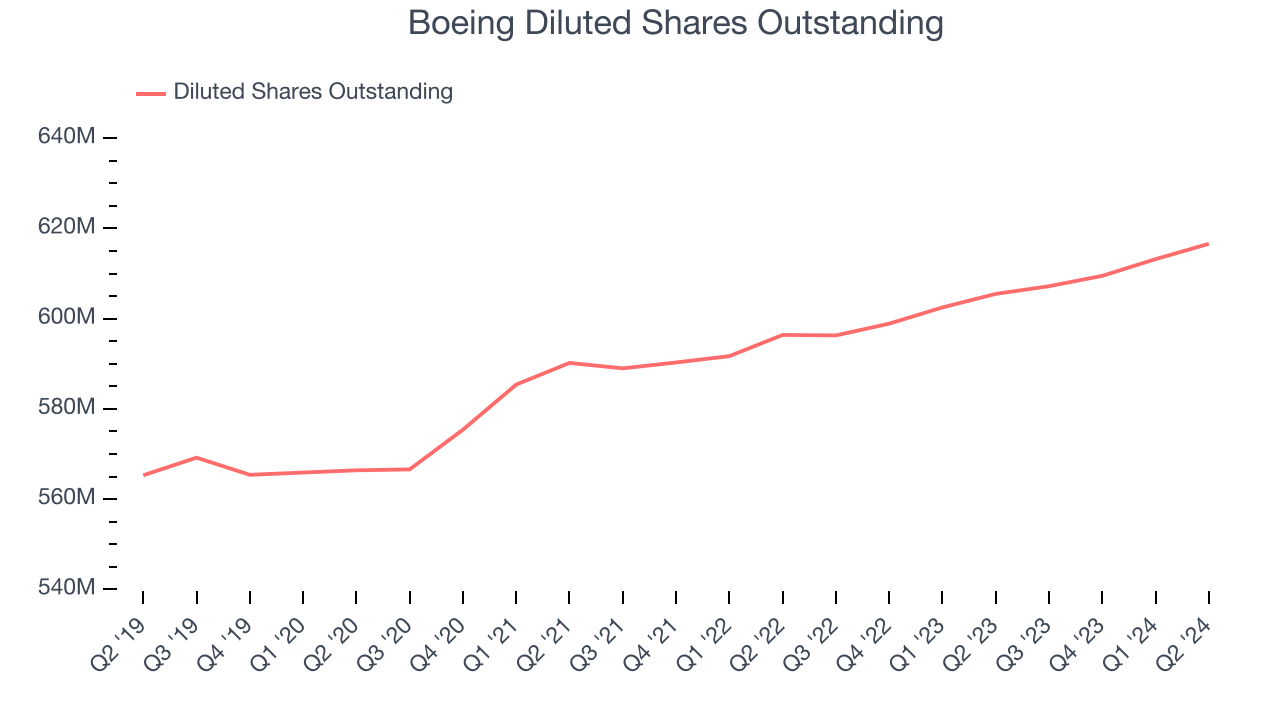

Diving into the nuances of Boeing's earnings can give us a better understanding of its performance. A five-year view shows Boeing has diluted its shareholders, growing its share count by 9.1%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

Like with revenue, we also analyze EPS over a more recent period because it can give insight into an emerging theme or development for the business. For Boeing, its two-year annual EPS growth of 17.5% was higher than its five-year trend. This acceleration made it one of the faster-growing industrials companies in recent history.

In Q2, Boeing reported EPS at negative $2.90, down from negative $0.82 in the same quarter last year. This print missed analysts' estimates. Over the next 12 months, Wall Street is optimistic. Analysts are projecting Boeing's EPS of negative $7.76 in the last year to flip to positive $2.28.

Key Takeaways from Boeing's Q2 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its EPS fell short of Wall Street's estimates. Overall, this was a bad quarter for Boeing. It seems expectations going into this quarter were quite low, though, given some of the negative headlines about safety issues and delayed deliveries . There seems to be a relief rally that the quarter wasn't worse. The stock traded up 3.4% to $193.20 immediately after reporting.

So should you invest in Boeing right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.