Dillard's (NYSE:DDS) Misses Q2 Sales Targets

Adam Hejl /

August 15, 2024

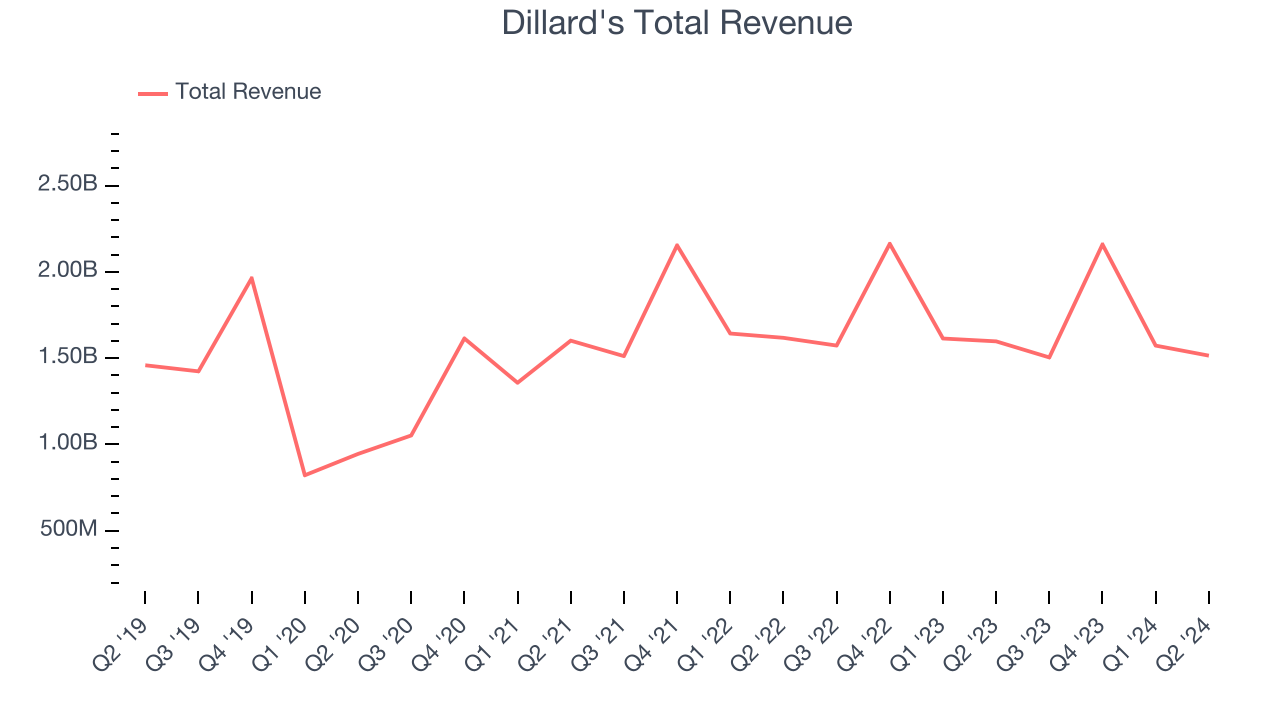

Department store chain Dillard’s (NYSE:DDS) fell short of analysts’ expectations in Q2 CY2024, with revenue down 5.2% year on year to $1.51 billion. It made a GAAP profit of $4.59 per share, down from its profit of $7.98 per share in the same quarter last year.

Is now the time to buy Dillard's? Find out in our full research report.

Dillard's (DDS) Q2 CY2024 Highlights:

- Revenue: $1.51 billion vs analyst estimates of $1.53 billion (1.1% miss)

- EPS: $4.59 vs analyst expectations of $6.01 (23.6% miss)

- Gross Margin (GAAP): 38.6%, down from 40% in the same quarter last year

- EBITDA Margin: 13%, in line with the same quarter last year

- Free Cash Flow was -$94.4 million, down from $85.44 million in the same quarter last year

- Locations: 273 at quarter end, down from 274 in the same quarter last year

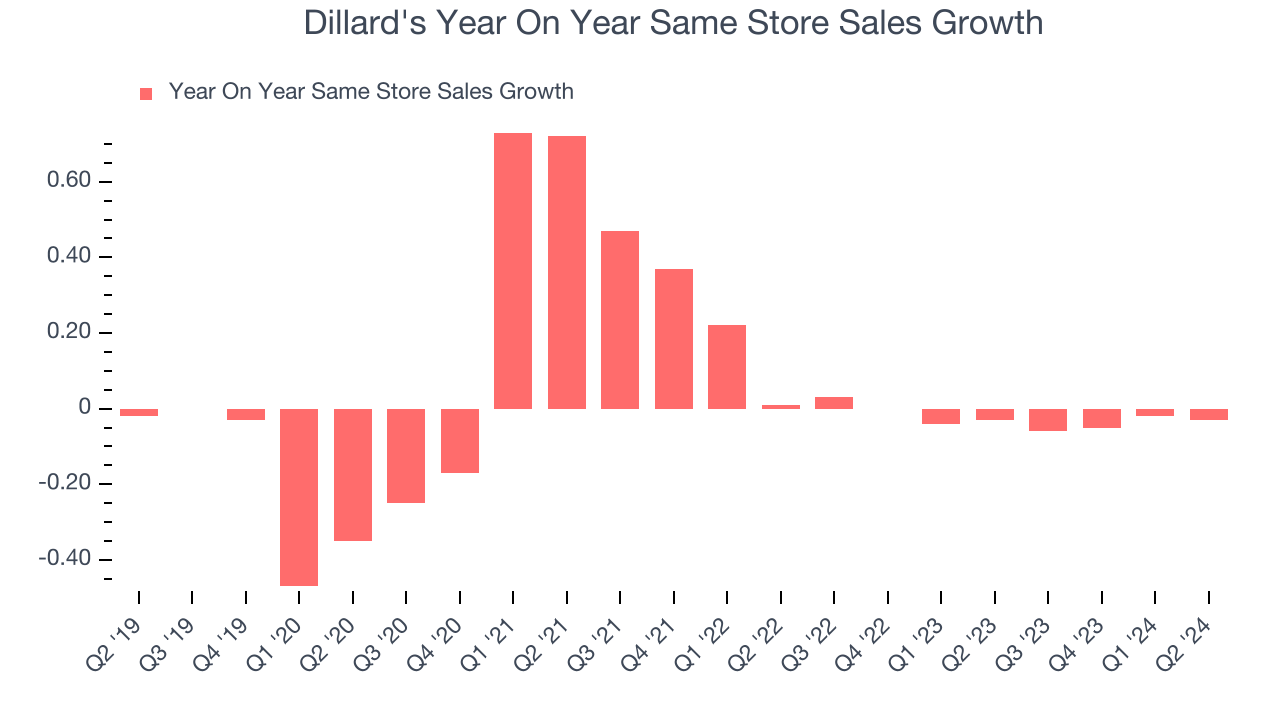

- Same-Store Sales fell 3% year on year, in line with the same quarter last year

- Market Capitalization: $6.35 billion

Dillard’s Chief Executive Officer William T. Dillard, II stated, “We are disappointed with our weak performance in the second quarter. While the consumer environment remained challenged, our expenses were up, squeezing our profitability. We are working to address this. We ended the quarter with over $1 billion in cash and short-term investments.”

With stores located largely in the Southern and Western US, Dillard’s (NYSE:DDS) is a department store chain that sells clothing, cosmetics, accessories, and home goods.

Department Store

Department stores emerged in the 19th century to provide customers with a wide variety of merchandise under one roof, offering a convenient and luxurious shopping experience. They played an important role in the history of American retail and urbanization, and prior to department stores, retailers tended to sell narrow specialty and niche items. But what was once new is now old, and department stores are somewhat considered a relic of the past. They are being attacked from multiple angles–stagnant foot traffic at malls where they’ve served as anchors; more nimble off-price and fast-fashion retailers; and e-commerce-first competitors not burdened by large physical footprints.

Sales Growth

Dillard's is larger than most consumer retail companies and benefits from economies of scale, giving it an edge over its competitors.

As you can see below, the company’s revenue was flat over the last five years as its store count dropped.

This quarter, Dillard's missed Wall Street’s estimates and reported a rather uninspiring 5.2% year-on-year revenue decline, generating $1.51 billion in revenue. Looking ahead, Wall Street expects revenue to decline 4.7% over the next 12 months.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

A company’s same-store sales growth shows the year-on-year change in sales for its brick-and-mortar stores that have been open for at least a year, give or take, and e-commerce platform. This is a key performance indicator for retailers because it measures organic growth and demand.

Dillard’s demand has been shrinking over the last eight quarters, and on average, its same-store sales have declined by 2.5% year on year. The company has been reducing its store count as fewer locations sometimes lead to higher same-store sales, but that hasn’t been the case here.

In the latest quarter, Dillard’s same-store sales fell 3% year on year. This performance was more or less in line with the same quarter last year.

Key Takeaways from Dillard’s Q2 Results

We struggled to find many strong positives in these results as its revenue and EPS missed analysts’ expectations. Overall, this was a weaker quarter. The stock remained flat at $348.89 immediately after reporting.

So should you invest in Dillard's right now? When making that decision, it’s important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it’s free.