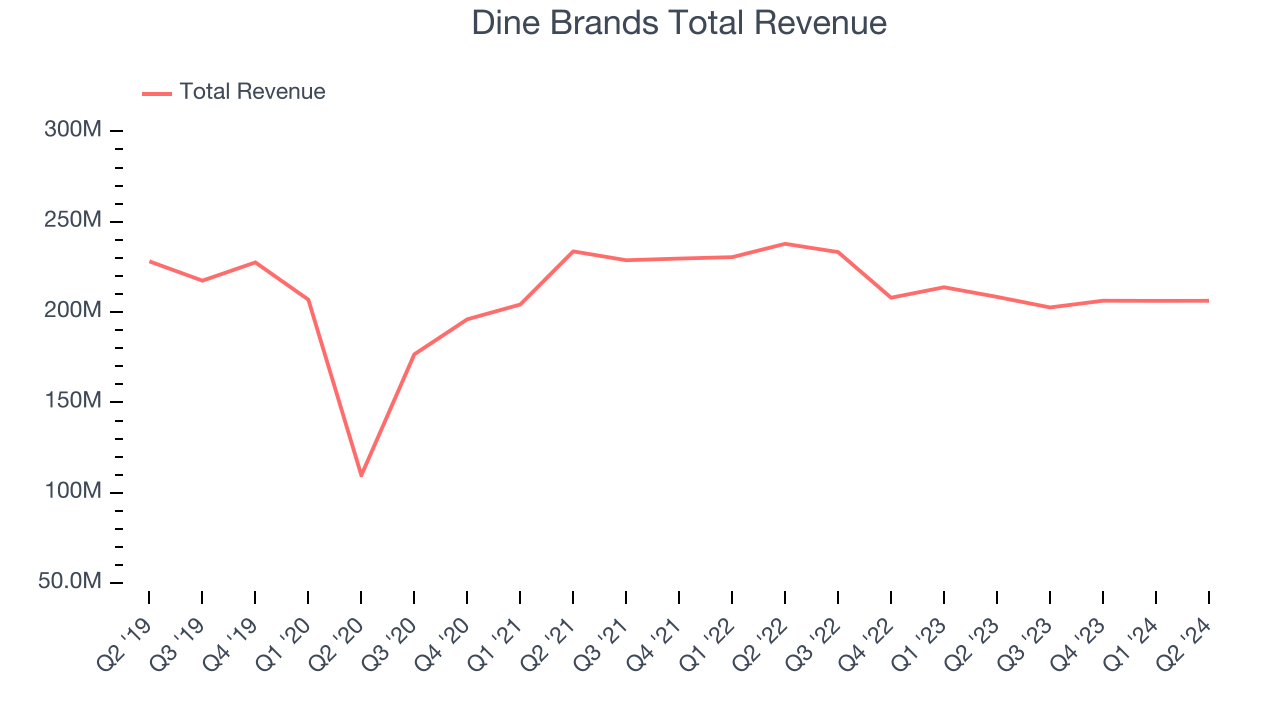

Casual restaurant chain Dine Brands (NYSE:DIN) fell short of analysts' expectations in Q2 CY2024, with revenue down 1% year on year to $206.3 million. It made a non-GAAP profit of $1.71 per share, down from its profit of $1.82 per share in the same quarter last year.

Is now the time to buy Dine Brands? Find out by accessing our full research report, it's free.

Dine Brands (DIN) Q2 CY2024 Highlights:

- Revenue: $206.3 million vs analyst estimates of $210.5 million (2% miss)

- EPS (non-GAAP): $1.71 vs analyst estimates of $1.64 (4.1% beat)

- Gross Margin (GAAP): 48.1%, in line with the same quarter last year

- EBITDA Margin: 32.5%, in line with the same quarter last year

- Free Cash Flow of $18.18 million, down 33.2% from the previous quarter

- Locations: 3,436 at quarter end, down from 3,451 in the same quarter last year

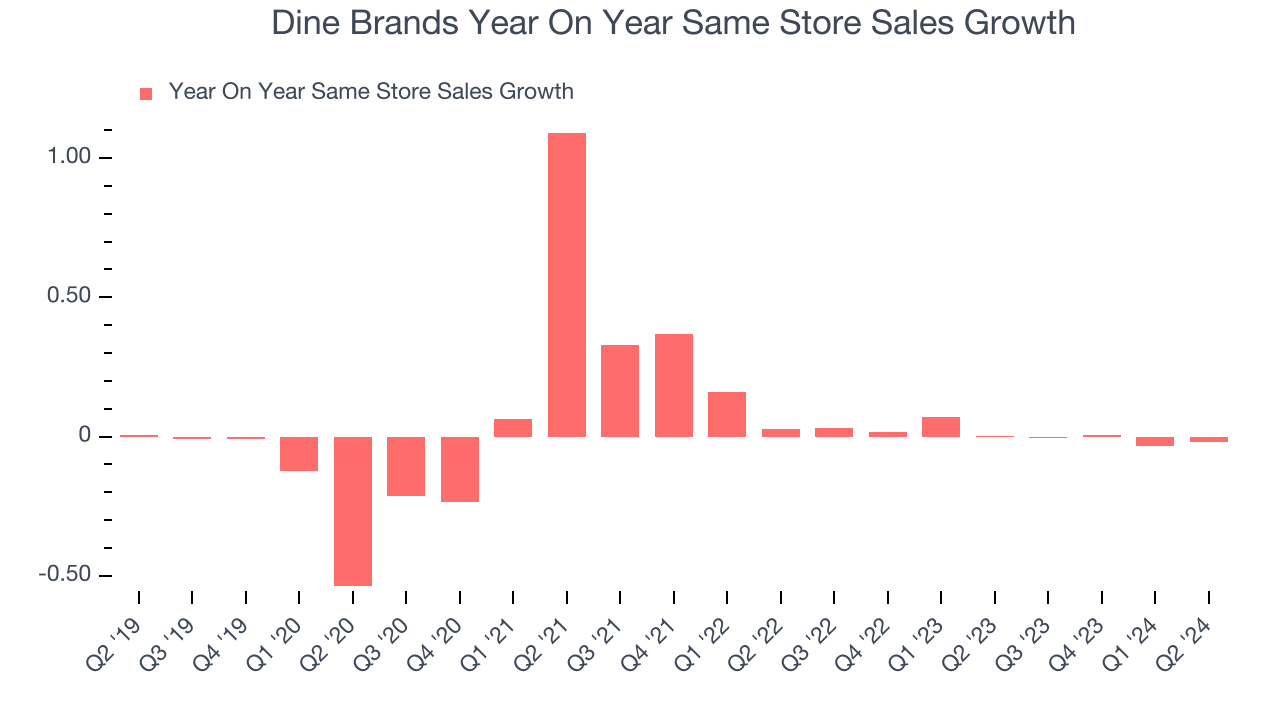

- Same-Store Sales fell 1.8% year on year (0.3% in the same quarter last year)

- Market Capitalization: $491.6 million

“Our brands have a long history of weathering economic cycles and despite the consumer pullback the industry witnessed this quarter, we are confident that our strategies around profitable promotions, menu innovation and development will help us manage both short-term challenges while positioning us for the long term,” said John Peyton, chief executive officer, Dine Brands Global, Inc.

Operating a franchise model, Dine Brands (NYSE:DIN) is a casual restaurant chain that owns the Applebee’s and IHOP banners.

Sit-Down Dining

Sit-down restaurants offer a complete dining experience with table service. These establishments span various cuisines and are renowned for their warm hospitality and welcoming ambiance, making them perfect for family gatherings, special occasions, or simply unwinding. Their extensive menus range from appetizers to indulgent desserts and wines and cocktails. This space is extremely fragmented and competition includes everything from publicly-traded companies owning multiple chains to single-location mom-and-pop restaurants.

Sales Growth

Dine Brands is a mid-sized restaurant chain, which sometimes brings disadvantages compared to larger competitors benefiting from better brand awareness and economies of scale. On the other hand, Dine Brands can still achieve high growth rates because its revenue base is not yet monstrous.

As you can see below, the company's revenue has declined over the last five years, dropping 1.2% annually as it didn't open many new restaurants.

This quarter, Dine Brands missed Wall Street's estimates and reported a rather uninspiring 1% year-on-year revenue decline, generating $206.3 million in revenue. Looking ahead, Wall Street expects sales to grow 2.2% over the next 12 months, an acceleration from this quarter.

Here at StockStory, we certainly understand the potential of thematic investing. Diverse winners from Microsoft (MSFT) to Alphabet (GOOG), Coca-Cola (KO) to Monster Beverage (MNST) could all have been identified as promising growth stories with a megatrend driving the growth. So, in that spirit, we’ve identified a relatively under-the-radar profitable growth stock benefitting from the rise of AI, available to you FREE via this link.

Same-Store Sales

Same-store sales growth is a key performance indicator used to measure organic growth and demand for restaurants.

Dine Brands's demand within its existing restaurants has barely risen over the last eight quarters. On average, the company's same-store sales growth has been flat.

In the latest quarter, Dine Brands's same-store sales fell 1.8% year on year. This decline was a reversal from the 0.3% year-on-year increase it posted 12 months ago. We'll be keeping a close eye on the company to see if this turns into a longer-term trend.

Key Takeaways from Dine Brands's Q2 Results

It was encouraging to see Dine Brands slightly top analysts' gross margin expectations this quarter. On the other hand, its revenue unfortunately missed analysts' expectations. Overall, this was a bad quarter for Dine Brands. The stock traded down 1.7% to $31.33 immediately after reporting.

Dine Brands may have had a tough quarter, but does that actually create an opportunity to invest right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.