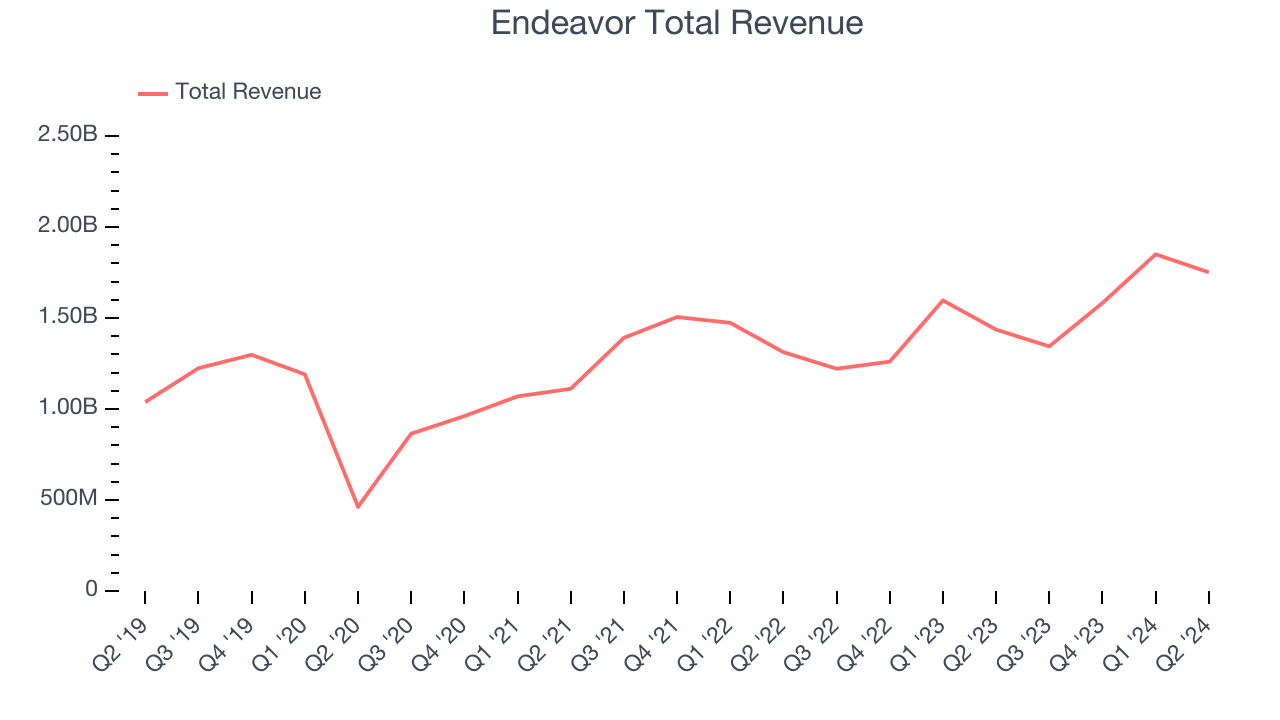

Global talent agency and entertainment company Endeavor (NYSE:EDR) missed analysts' expectations in Q2 CY2024, with revenue up 21.9% year on year to $1.75 billion. It made a GAAP loss of $0.70 per share, down from its profit of $1.30 per share in the same quarter last year.

Is now the time to buy Endeavor? Find out in our full research report.

Endeavor (EDR) Q2 CY2024 Highlights:

- Endeavor will be acquired by private equity firm Silver Lake for $27.50 per share in cash

- Revenue: $1.75 billion vs analyst estimates of $2.00 billion (12.4% miss)

- EPS: -$0.70 vs analyst estimates of $0.21 (-$0.91 miss)

- Gross Margin (GAAP): 57.6%, down from 59.3% in the same quarter last year

- EBITDA Margin: 21.7%, in line with the same quarter last year

- Market Capitalization: $8.22 billion

“TKO and PBR benefited from strong consumer demand and engagement during the quarter, and we continued to drive growth in our representation segment,” said Ariel Emanuel, CEO, Endeavor.

Owner of the UFC, WWE, and a client roster including Christian Bale, Endeavor (NYSE:EDR) is a diversified global entertainment, sports, and content company known for its talent representation and involvement in the entertainment industry.

Media

The advent of the internet changed how shows, films, music, and overall information flow. As a result, many media companies now face secular headwinds as attention shifts online. Some have made concerted efforts to adapt by introducing digital subscriptions, podcasts, and streaming platforms. Time will tell if their strategies succeed and which companies will emerge as the long-term winners.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Over the last five years, Endeavor grew its sales at a weak 11.9% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within consumer discretionary, product cycles are short and revenue can be hit-driven due to rapidly changing trends and consumer preferences. Endeavor's recent history shows its demand slowed as its annualized revenue growth of 7.2% over the last two years is below its five-year trend.

We can dig further into the company's revenue dynamics by analyzing its three most important segments: Events, Sports, and Representation, which are 27%, 51.1%, and 23.5% of revenue. Over the last two years, Endeavor's Sports revenue (UFC, Euroleague) averaged 57.4% year-on-year growth while its Events (live events) and Representation (WME talent agency, IMG Models) revenues averaged 8.6% and 8.7% declines.

This quarter, Endeavor generated an excellent 21.9% year-on-year revenue growth rate, but its $1.75 billion of revenue fell short of Wall Street's high expectations. Looking ahead, Wall Street expects sales to grow 19.8% over the next 12 months, a deceleration from this quarter.

Today’s young investors won’t have read the timeless lessons in Gorilla Game: Picking Winners In High Technology because it was written more than 20 years ago when Microsoft and Apple were first establishing their supremacy. But if we apply the same principles, then enterprise software stocks leveraging their own generative AI capabilities may well be the Gorillas of the future. So, in that spirit, we are excited to present our Special Free Report on a profitable, fast-growing enterprise software stock that is already riding the automation wave and looking to catch the generative AI next.

Operating Margin

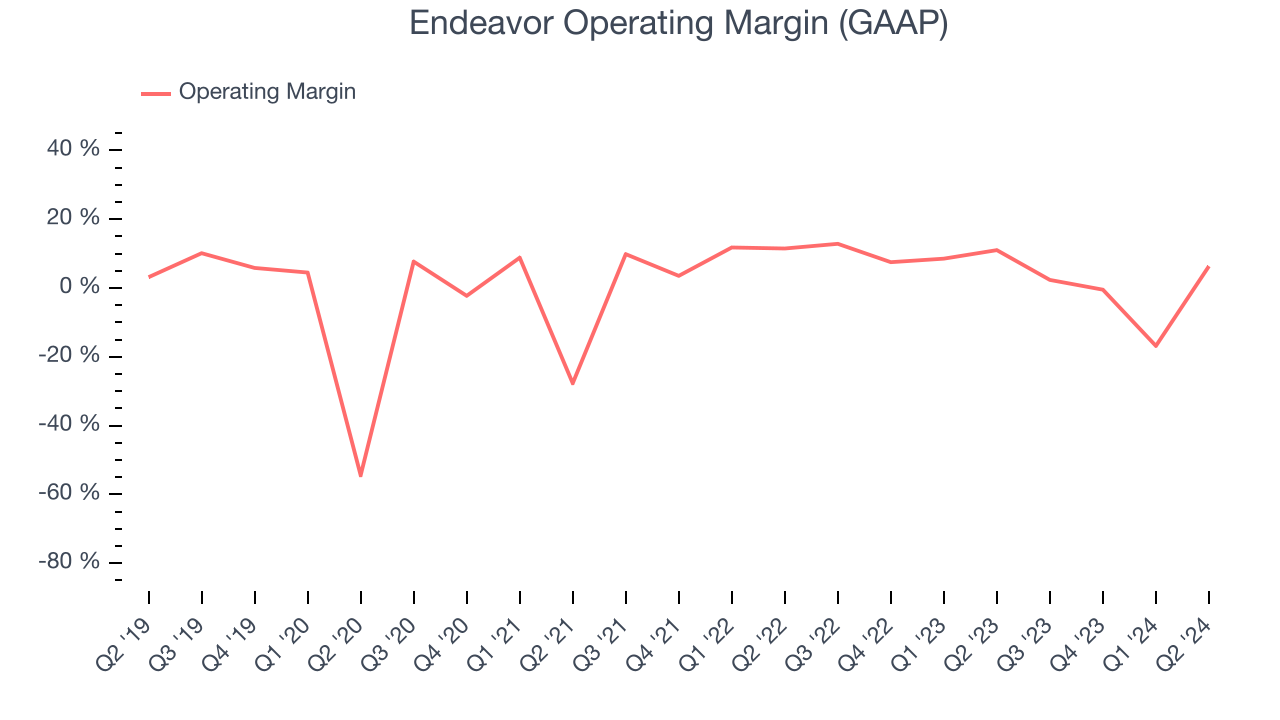

Endeavor's operating margin has shrunk over the last year and averaged 3.1%. The company's profitability was mediocre for a consumer discretionary business and shows it couldn't pass its higher operating expenses onto its customers.

This quarter, Endeavor generated an operating profit margin of 6.4%, down 4.7 percentage points year on year. This contraction shows it was recently less efficient because its expenses grew faster than its revenue.

Key Takeaways from Endeavor's Q2 Results

We struggled to find many strong positives in these results. Its revenue unfortunately missed and its EPS fell short of Wall Street's estimates. Overall, this was a mixed but overall mediocre quarter for Endeavor. The stock remained flat at $27.21 immediately after reporting.

So should you invest in Endeavor right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.