ESAB (NYSE:ESAB) Posts Better-Than-Expected Sales In Q2

Jabin Bastian /

August 2, 2024

Welding and cutting equipment manufacturer ESAB (NYSE:ESAB) beat analysts' expectations in Q2 CY2024, with revenue down 1.9% year on year to $707.1 million. It made a non-GAAP profit of $1.32 per share, improving from its profit of $1.28 per share in the same quarter last year.

Is now the time to buy ESAB? Find out in our full research report.

ESAB (ESAB) Q2 CY2024 Highlights:

- Revenue: $707.1 million vs analyst estimates of $686.6 million (3% beat)

- EPS (non-GAAP): $1.32 vs analyst estimates of $1.27 (4.1% beat)

- EPS (non-GAAP) Guidance for the full year is $4.85 at the midpoint, missing analysts' estimates by 1.2%

- EBITDA Guidance for the full year is $505 million at the midpoint, below analyst estimates of $509.7 million

- Gross Margin (GAAP): 38.2%, up from 36.6% in the same quarter last year

- Free Cash Flow of $74,000, down 99.8% from the previous quarter

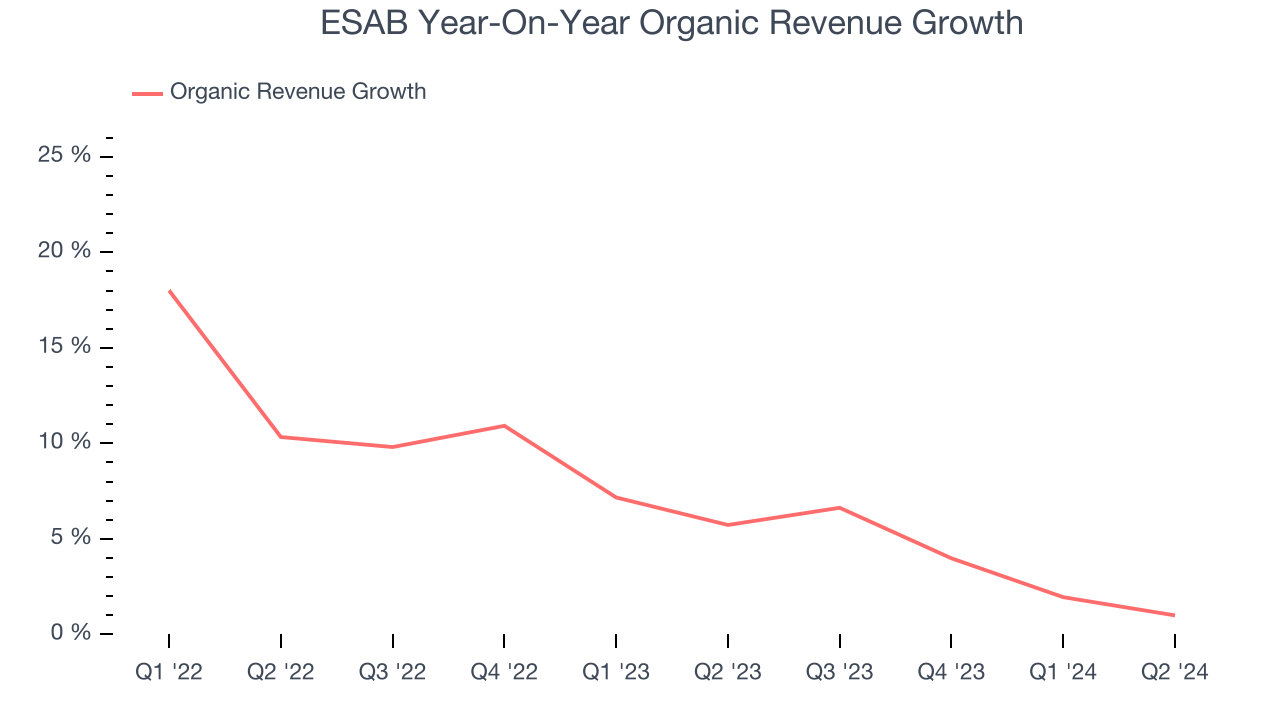

- Organic Revenue rose 1% year on year (5.7% in the same quarter last year)

- Market Capitalization: $5.94 billion

“The ESAB team continues to execute well in a challenging business environment. We are benefiting from our exposure to high-growth markets, such as India and the Middle East, as well as our strategy to improve our mix and focus on less cyclical end markets. Our recent acquisition of the welding business of Linde Bangladesh fills a gap for ESAB in Asia and cements our position as the leading Fabtech company in this fast-growing region,” stated Shyam P. Kambeyanda, President and CEO of ESAB.

Having played a significant role in the construction of the iconic Sydney Opera House, ESAB (NYSE:ESAB) manufactures and sells welding and cutting equipment for numerous industries.

Professional Tools and Equipment

Automation that increases efficiency and connected equipment that collects analyzable data have been trending, creating new demand. Some professional tools and equipment companies also provide software to accompany measurement or automated machinery, adding a stream of recurring revenues to their businesses. On the other hand, professional tools and equipment companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

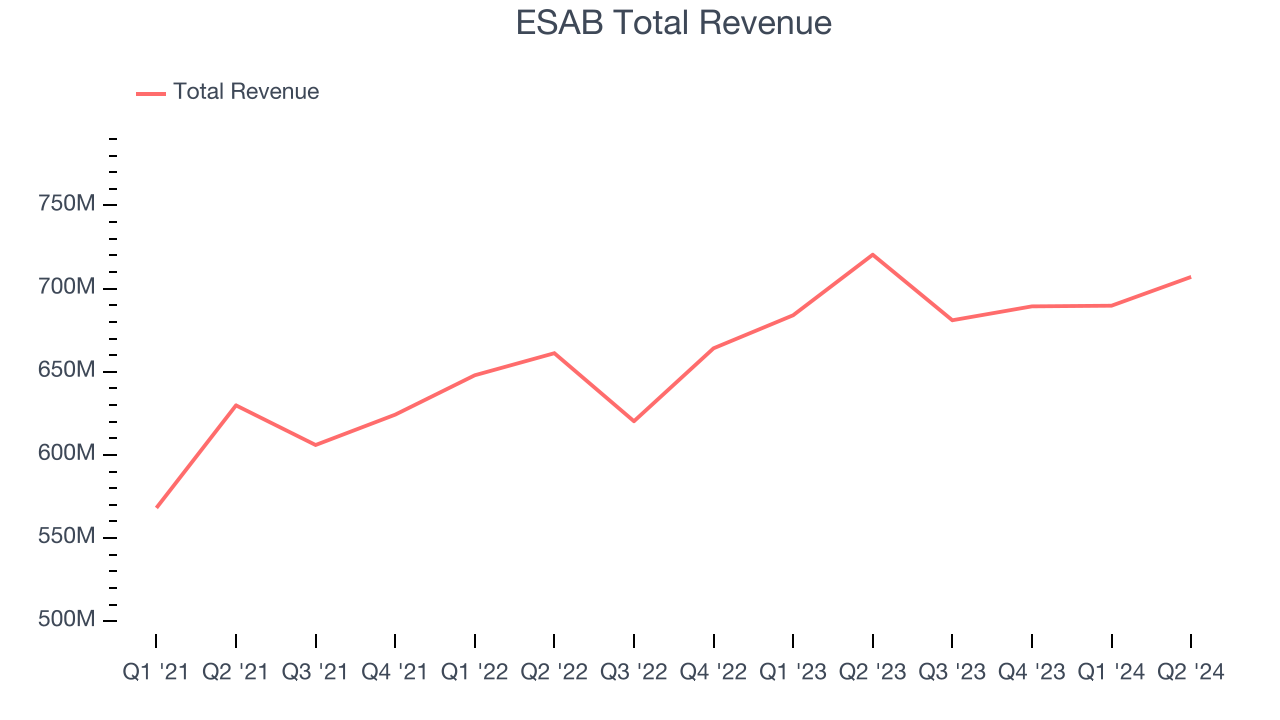

A company’s long-term performance can give signals about its business quality. Even a bad business can shine for one or two quarters, but a top-tier one tends to grow for years. Regrettably, ESAB's sales grew at a weak 5.3% compounded annual growth rate over the last three years. This shows it failed to expand in any major way and is a rough starting point for our analysis.

We at StockStory place the most emphasis on long-term growth, but within industrials, a stretched historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. ESAB's annualized revenue growth of 4.4% over the last two years aligns with its three-year trend, suggesting its demand was consistently weak.

ESAB also reports organic revenue, which strips out one-time events like acquisitions and currency fluctuations because they don't accurately reflect its fundamentals. Over the last two years, ESAB's organic revenue averaged 5.9% year-on-year growth. Because this number is better than its normal revenue growth, we can see that some mixture of divestitures and foreign exchange rates dampened its headline performance.

This quarter, ESAB's revenue fell 1.9% year on year to $707.1 million but beat Wall Street's estimates by 3%. Looking ahead, Wall Street expects revenue to remain flat over the next 12 months.

When a company has more cash than it knows what to do with, buying back its own shares can make a lot of sense–as long as the price is right. Luckily, we’ve found one, a low-priced stock that is gushing free cash flow AND buying back shares. Click here to claim your Special Free Report on a fallen angel growth story that is already recovering from a setback.

Operating Margin

Operating margin is an important measure of profitability as it shows the portion of revenue left after accounting for all core expenses–everything from the cost of goods sold to advertising and wages. It's also useful for comparing profitability across companies with different levels of debt and tax rates because it excludes interest and taxes.

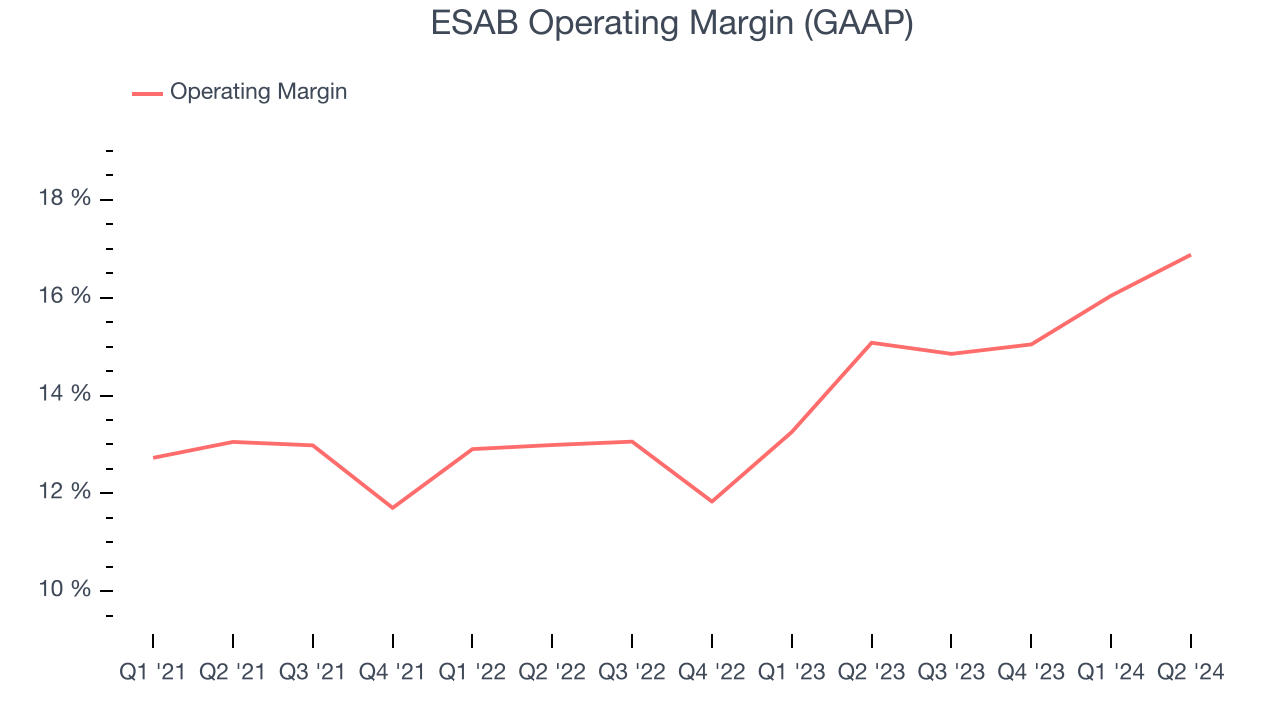

ESAB has been an optimally-run company over the last four years. It was one of the more profitable businesses in the industrials sector, boasting an average operating margin of 13.8%. This result isn't too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, ESAB's annual operating margin rose by 3.6 percentage points over the last four years, showing its efficiency has improved.

This quarter, ESAB generated an operating profit margin of 16.9%, up 1.8 percentage points year on year. This increase was encouraging, and since the company's operating margin rose more than its gross margin, we can infer it was recently more efficient with expenses such as sales, marketing, R&D, and administrative overhead.

EPS

Analyzing revenue trends tells us about a company's historical growth, but earnings per share (EPS) growth points to the profitability of that growth–for example, a company could inflate sales through excessive spending on advertising and promotions.

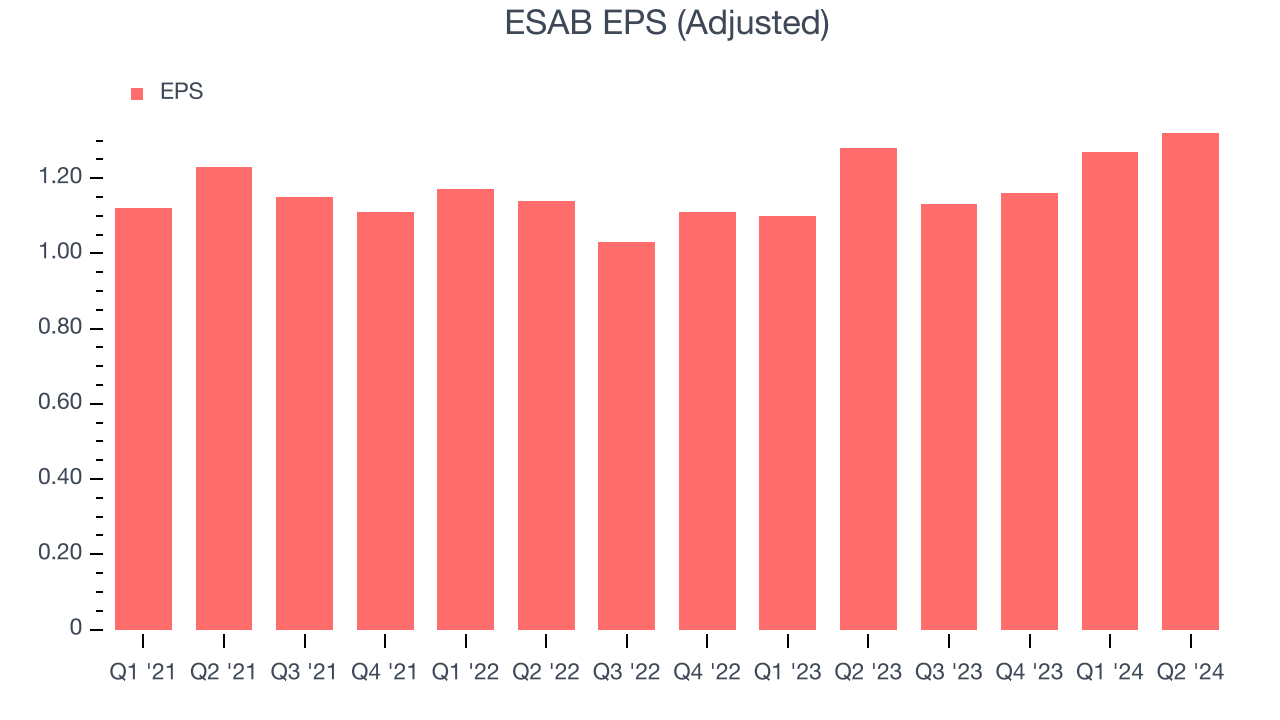

ESAB's EPS grew at a weak 3.3% compounded annual growth rate over the last two years, lower than its 4.4% annualized revenue growth. However, its operating margin actually expanded during this timeframe, telling us non-fundamental factors affected its ultimate earnings.

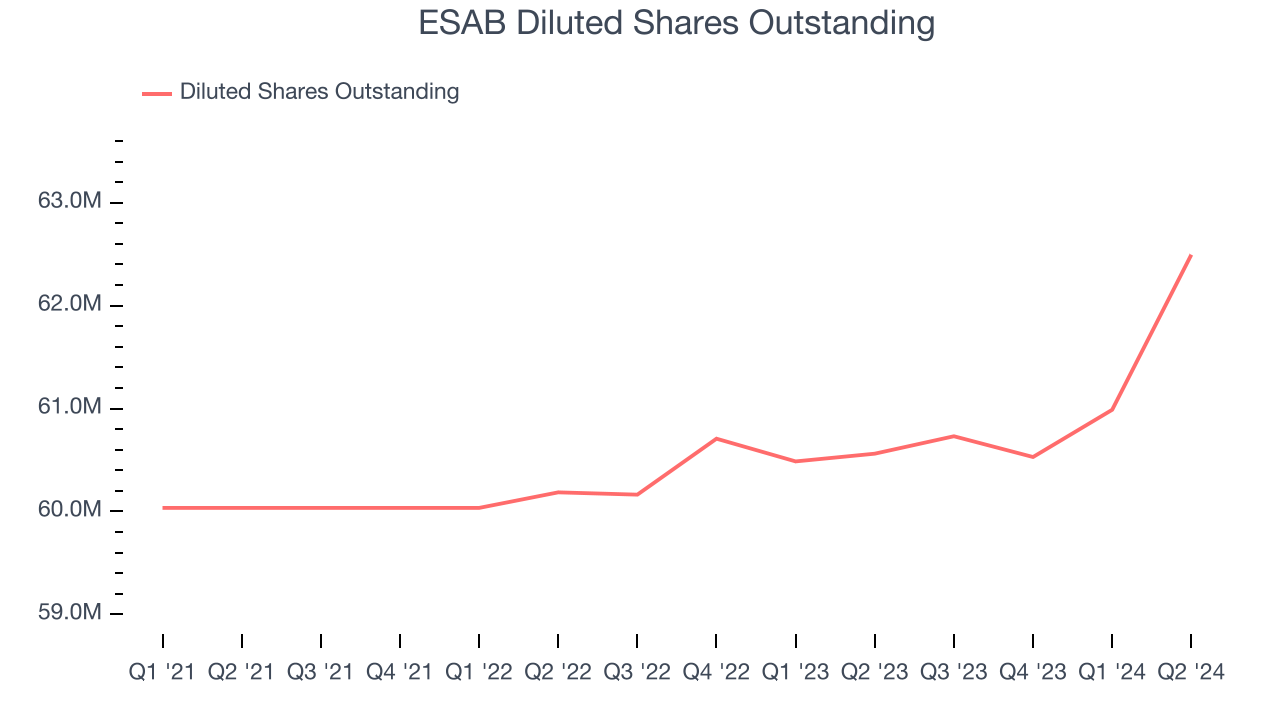

We can take a deeper look into ESAB's earnings to better understand the drivers of its performance. A two-year view shows ESAB has diluted its shareholders, growing its share count by 3.8%. This dilution overshadowed its increased operating efficiency and has led to lower per share earnings. Taxes and interest expenses can also affect EPS but don't tell us as much about a company's fundamentals.

In Q2, ESAB reported EPS at $1.32, up from $1.28 in the same quarter last year. This print beat analysts' estimates by 4.1%. Over the next 12 months, Wall Street expects ESAB to grow its earnings. Analysts are projecting its EPS of $4.88 in the last year to climb by 7.7% to $5.26.

Key Takeaways from ESAB's Q2 Results

We were impressed by how significantly ESAB blew past analysts' revenue expectations this quarter. We were also glad its EPS outperformed Wall Street's estimates. On the other hand, its organic revenue missed and guidance was below expectations. Overall, this was a mixed but overall mediocre quarter for ESAB. The stock remained flat at $98.24 immediately following the results.

So should you invest in ESAB right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.