Griffon (NYSE:GFF) Misses Q2 Sales Targets

Max Juang /

August 7, 2024

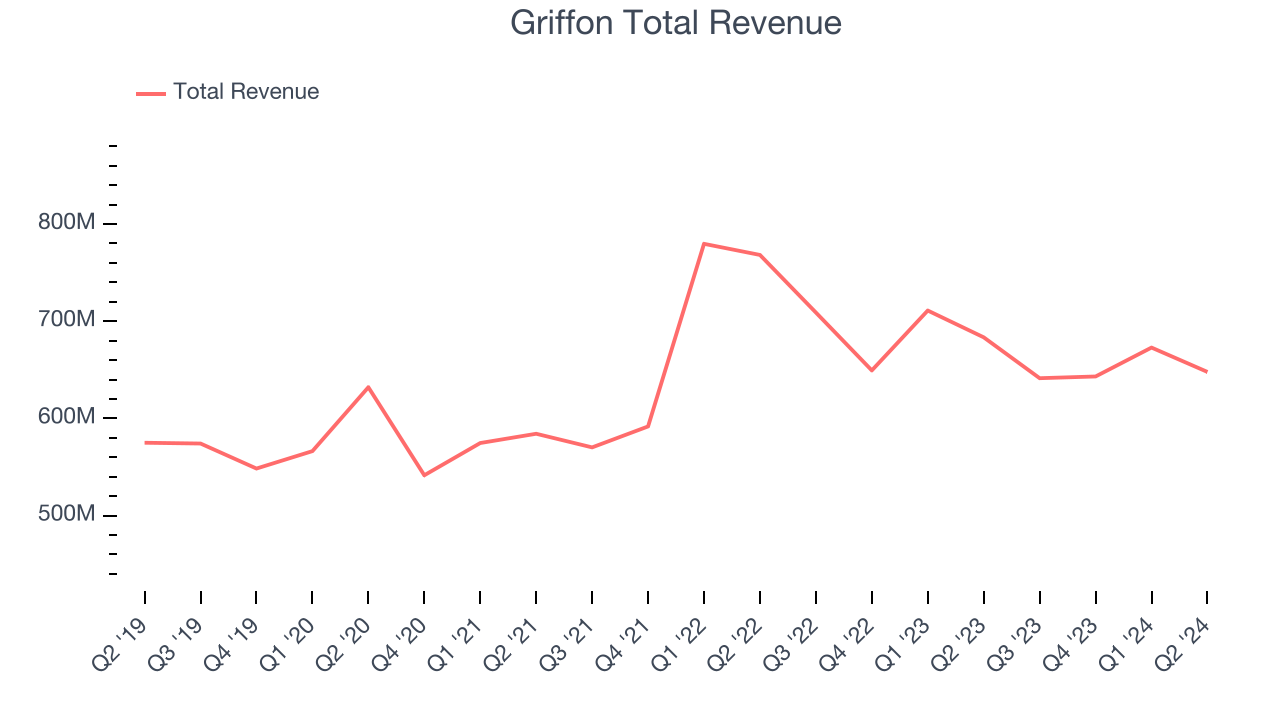

Multi-industry consumer and professional products manufacturer Griffon Corporation (NYSE:GFF) fell short of analysts' expectations in Q2 CY2024, with revenue down 5.2% year on year to $647.8 million. On the other hand, the company's outlook for the full year was close to analysts' estimates with revenue guided to $2.65 billion at the midpoint.

Is now the time to buy Griffon? Find out in our full research report.

Griffon (GFF) Q2 CY2024 Highlights:

- Revenue: $647.8 million vs analyst estimates of $688.9 million (6% miss)

- The company reconfirmed its revenue guidance for the full year of $2.65 billion at the midpoint

- EBITDA guidance for the full year is $555 million at the midpoint, above analyst estimates of $505.9 million

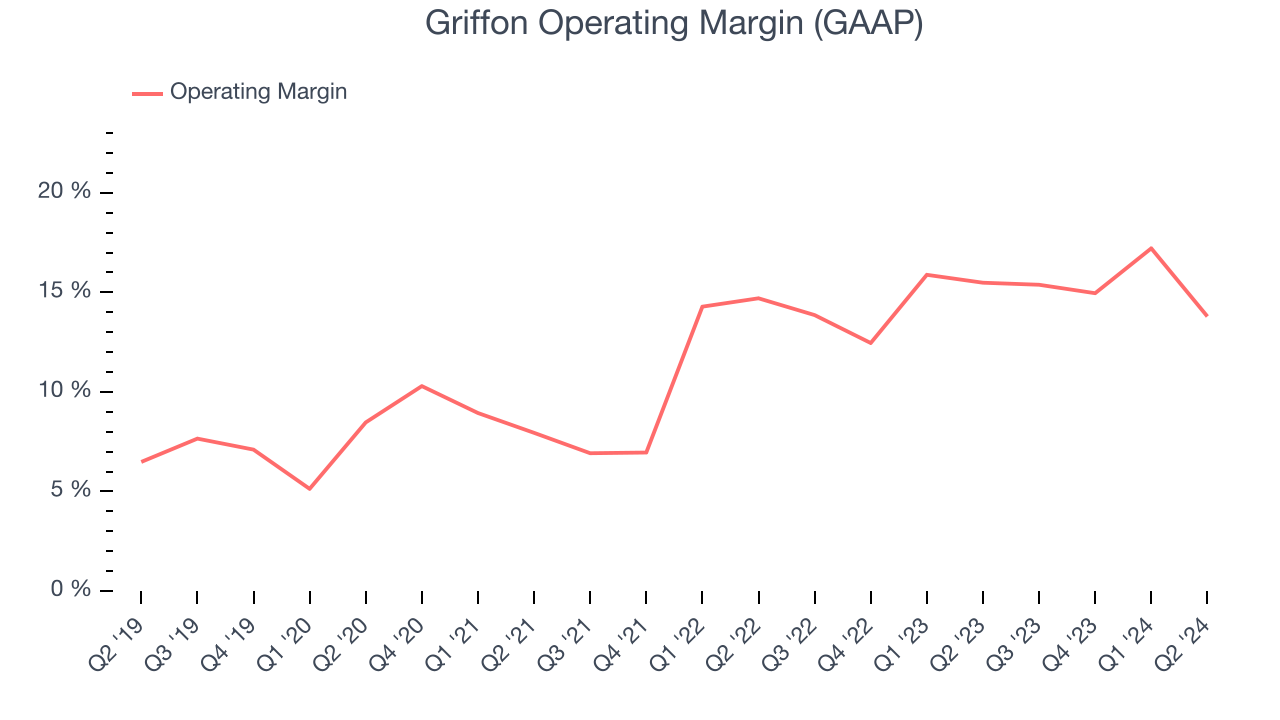

- Gross Margin (GAAP): 38.5%, down from 40.4% in the same quarter last year

- EBITDA Margin: 21.7%

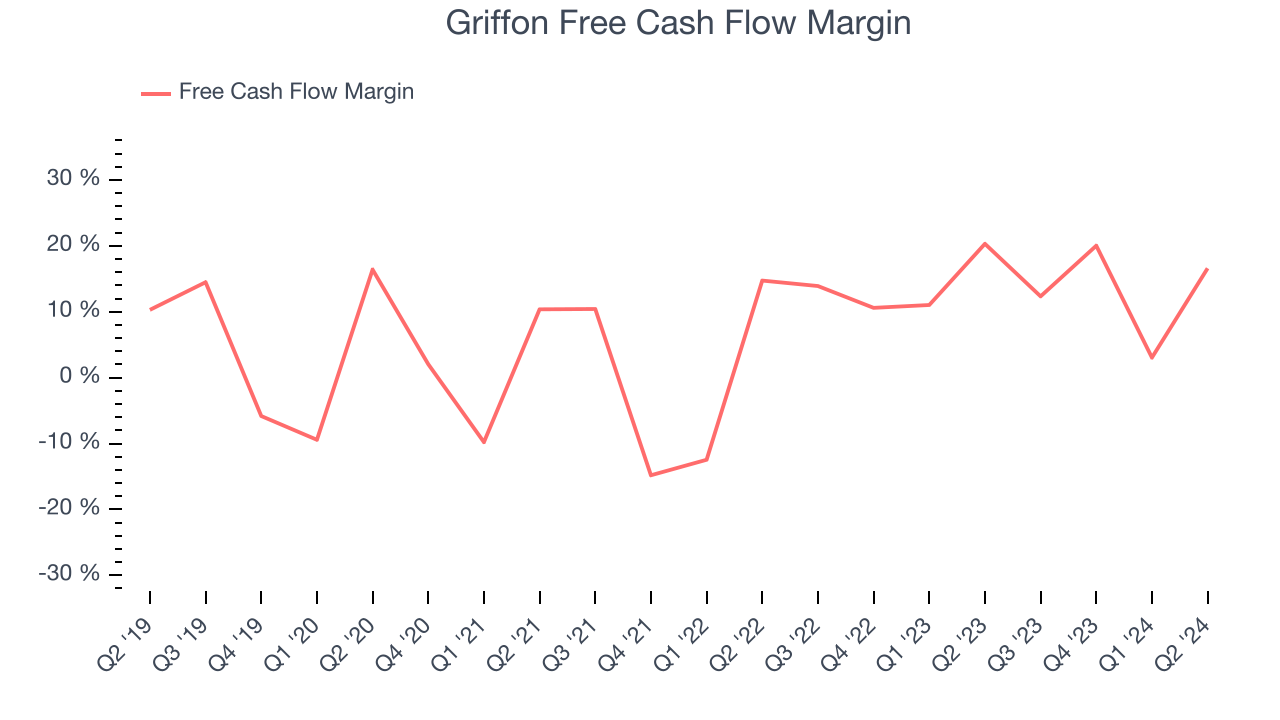

- Free Cash Flow of $107.5 million, up from $20.5 million in the previous quarter

- Market Capitalization: $3.45 billion

“Griffon's third quarter results were highlighted by solid operating performance from Home and Building Products (“HBP”), improved profitability at Consumer and Professional Products (“CPP”) and strong free cash flow conversion,” said Ronald J. Kramer, Chairman and Chief Executive Officer.

Initially in the defense industry, Griffon (NYSE:GFF) is a now diversified company specializing in home improvement, professional equipment, and building products.

Home Construction Materials

Traditionally, home construction materials companies have built economic moats with expertise in specialized areas, brand recognition, and strong relationships with contractors. More recently, advances to address labor availability and job site productivity have spurred innovation that is driving incremental demand. However, these companies are at the whim of residential construction volumes, which tend to be cyclical and can be impacted heavily by economic factors such as interest rates. Additionally, the costs of raw materials can be driven by a myriad of worldwide factors and greatly influence the profitability of home construction materials companies.

Sales Growth

A company’s long-term performance can indicate its business quality. Any business can put up a good quarter or two, but many enduring ones tend to grow for years. Over the last five years, Griffon grew its sales at a weak 3.7% compounded annual growth rate. This shows it failed to expand in any major way and is a rough starting point for our analysis.

Long-term growth is the most important, but within industrials, a half-decade historical view may miss new industry trends or demand cycles. Griffon's history shows it grew in the past but relinquished its gains over the last two years, as its revenue fell by 1.9% annually.

This quarter, Griffon missed Wall Street's estimates and reported a rather uninspiring 5.2% year-on-year revenue decline, generating $647.8 million of revenue. Looking ahead, Wall Street expects sales to grow 3.8% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Griffon has managed its expenses well over the last five years. It demonstrated solid profitability for an industrials business, producing an average operating margin of 11.8%. This result isn't too surprising as its gross margin gives it a favorable starting point.

Looking at the trend in its profitability, Griffon's annual operating margin rose by 8.2 percentage points over the last five years, showing its efficiency has meaningfully improved.

This quarter, Griffon generated an operating profit margin of 13.8%, down 1.7 percentage points year on year. Since Griffon's gross margin decreased more than its operating margin, we can assume its recent inefficiencies were driven more by weaker leverage on its cost of sales rather than increased sales, marketing, R&D, and administrative overhead expenses.

Cash Is King

Although earnings are undoubtedly valuable for assessing company performance, we believe cash is king because you can't use accounting profits to pay the bills.

Griffon has shown decent cash profitability, giving it some flexibility to reinvest or return capital to investors. The company's free cash flow margin averaged 6.8% over the last five years, slightly better than the broader industrials sector.

Taking a step back, we can see that Griffon's margin expanded by 8.5 percentage points during that time. This is encouraging because it gives the company more optionality.

Griffon's free cash flow clocked in at $107.5 million in Q2, equivalent to a 16.6% margin. The company's cash profitability regressed as it was 3.7 percentage points lower than in the same quarter last year, but it's still above its five-year average. We wouldn't put too much weight on this quarter's decline because investment needs can be seasonal, causing short-term swings. Long-term trends carry greater meaning.

Key Takeaways from Griffon's Q2 Results

We were impressed by Griffon's optimistic full-year EBITDA forecast, which blew past analysts' expectations. On the other hand, its revenue unfortunately missed. Overall, this quarter was mixed. The stock remained flat at $69.60 immediately after reporting.

So should you invest in Griffon right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.