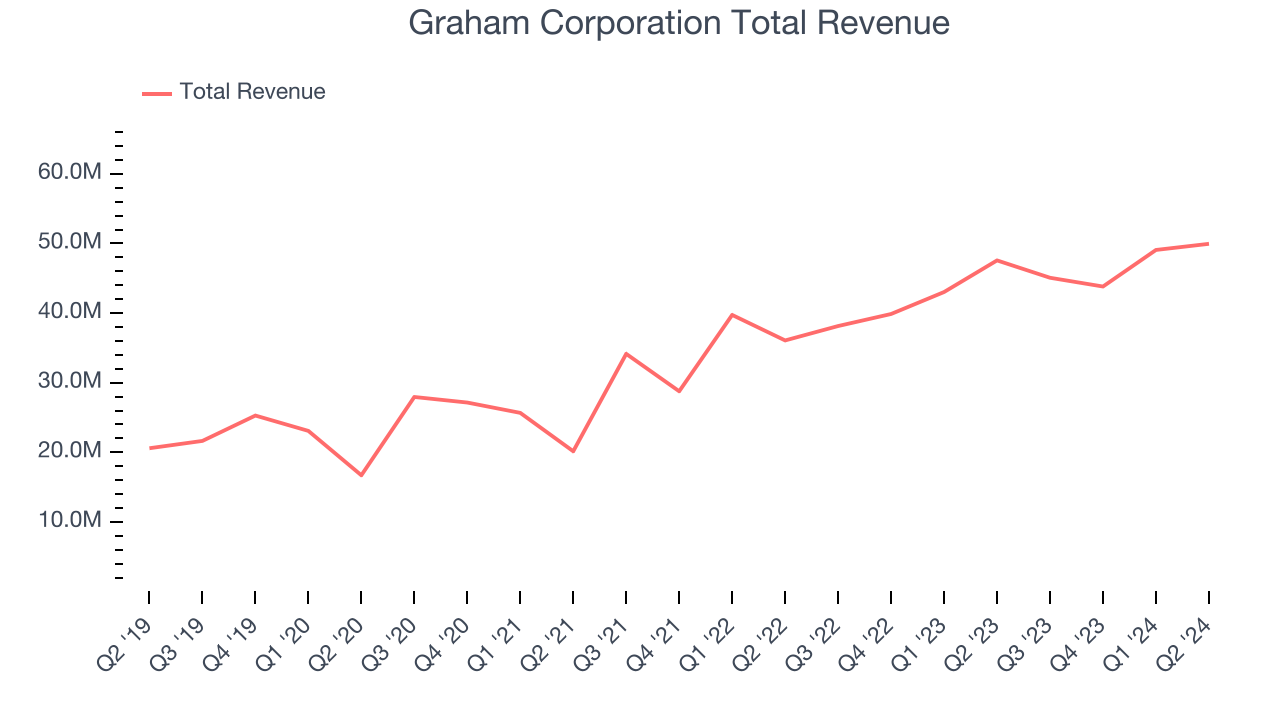

Industrial fluid and energy systems manufacturer Graham Corporation (NYSE: GHM) reported results in line with analysts' expectations in Q2 CY2024, with revenue up 5% year on year to $49.95 million. On the other hand, the company's full-year revenue guidance of $205 million at the midpoint came in slightly below analysts' estimates. It made a GAAP profit of $0.27 per share, improving from its profit of $0.25 per share in the same quarter last year.

Is now the time to buy Graham Corporation? Find out in our full research report.

Graham Corporation (GHM) Q2 CY2024 Highlights:

- Revenue: $49.95 million vs analyst estimates of $50.1 million (small miss)

- EPS: $0.27 vs analyst estimates of $0.14 ($0.13 beat)

- The company reconfirmed its revenue guidance for the full year of $205 million at the midpoint

- EBITDA guidance for the full year is $18 million at the midpoint, below analyst estimates of $18.98 million

- Gross Margin (GAAP): 24.8%, up from 23.1% in the same quarter last year

- EBITDA Margin: 10.3%, in line with the same quarter last year

- Free Cash Flow of $5.74 million, up 24.6% from the previous quarter

- Market Capitalization: $315.5 million

“We are delivering consistent improvement, solid growth and strengthening profitability,” commented Daniel J. Thoren, President and Chief Executive Officer.

Founded when its founder patented a unique design for a vacuum system used in the sugar refining process, Graham (NYSE:GHM) provides vacuum and heat transfer equipment for the energy, petrochemical, refining, and chemical sectors.

Engineered Components and Systems

Engineered components and systems companies possess technical know-how in sometimes narrow areas such as metal forming or intelligent robotics. Lately, automation and connected equipment collecting analyzable data have been trending, creating new demand. On the other hand, like the broader industrials sector, engineered components and systems companies are at the whim of economic cycles. Consumer spending and interest rates, for example, can greatly impact the industrial production that drives demand for these companies’ offerings.

Sales Growth

Examining a company's long-term performance can provide clues about its business quality. Any business can put up a good quarter or two, but the best consistently grow over the long haul. Thankfully, Graham Corporation's 18.4% annualized revenue growth over the last five years was incredible. This is a great starting point for our analysis because it shows Graham Corporation's offerings resonate with customers.

We at StockStory place the most emphasis on long-term growth, but within industrials, a half-decade historical view may miss cycles, industry trends, or a company capitalizing on catalysts such as a new contract win or a successful product line. Graham Corporation's annualized revenue growth of 16.4% over the last two years is below its five-year trend, but we still think the results were good and suggest demand was strong.

This quarter, Graham Corporation grew its revenue by 5% year on year, and its $49.95 million of revenue was in line with Wall Street's estimates. Looking ahead, Wall Street expects sales to grow 12.3% over the next 12 months, an acceleration from this quarter.

Unless you’ve been living under a rock, it should be obvious by now that generative AI is going to have a huge impact on how large corporations do business. While Nvidia and AMD are trading close to all-time highs, we prefer a lesser-known (but still profitable) semiconductor stock benefitting from the rise of AI. Click here to access our free report on our favorite semiconductor growth story.

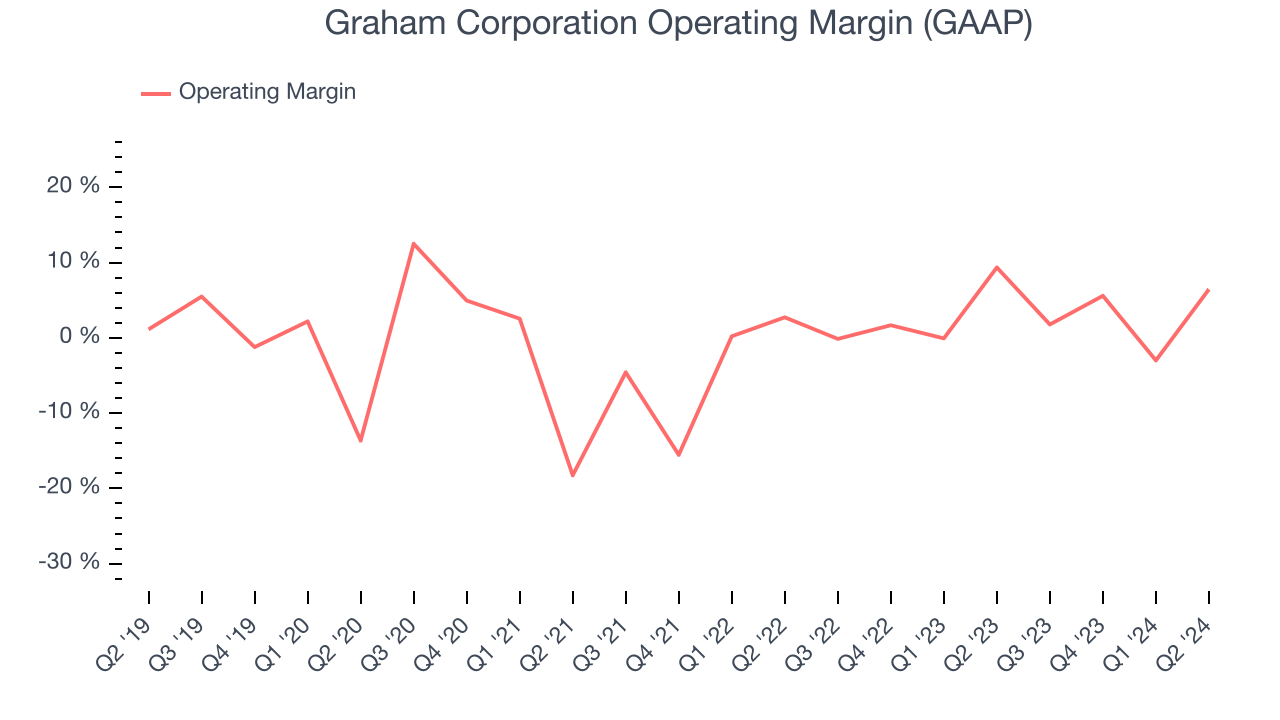

Operating Margin

Operating margin is one of the best measures of profitability because it tells us how much money a company takes home after procuring and manufacturing its products, marketing and selling them, and, most importantly, keeping them relevant through research and development.

Graham Corporation was roughly breakeven when averaging the last five years of quarterly operating profits, inadequate for an industrials business. This result isn't too surprising given its low gross margin as a starting point.

On the bright side, Graham Corporation's annual operating margin rose by 3.7 percentage points over the last five years, as its sales growth gave it operating leverage

This quarter, Graham Corporation generated an operating profit margin of 6.5%, down 2.9 percentage points year on year. Conversely, the company's revenue and gross margin actually rose, so we can assume it was recently less efficient because its operating expenses like sales, marketing, R&D, and administrative overhead grew faster than its revenue.

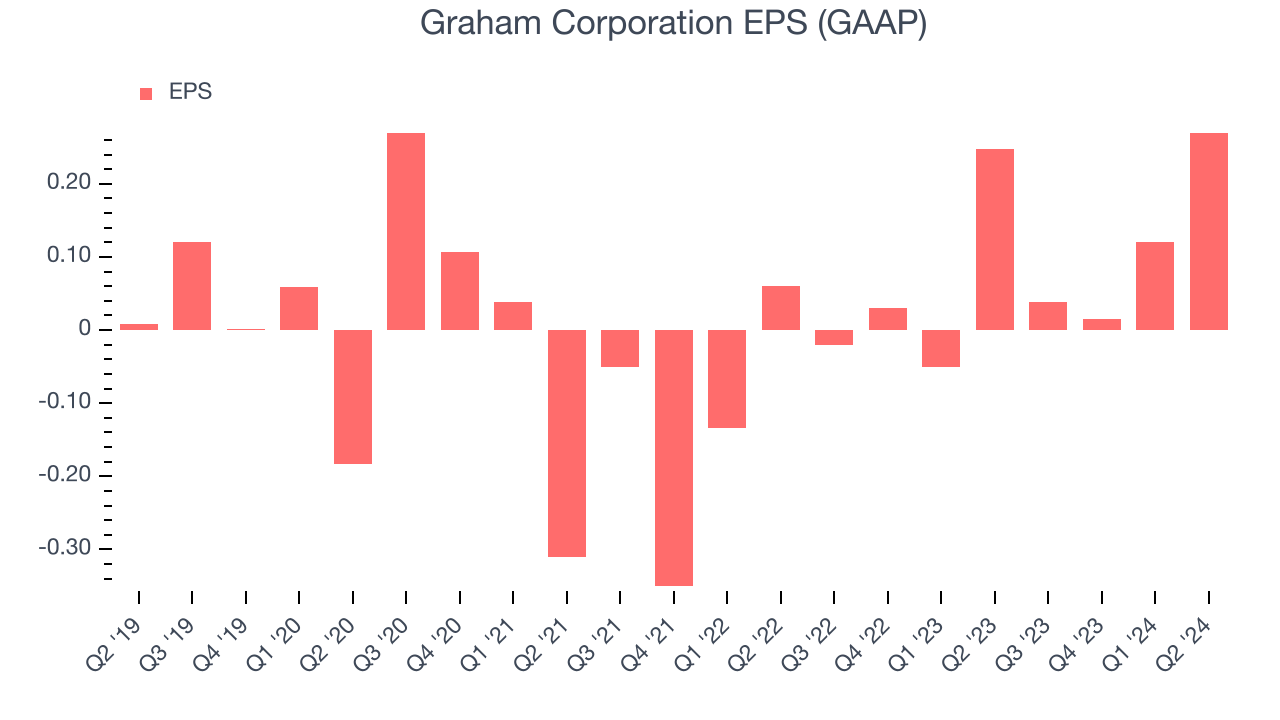

EPS

We track the long-term growth in earnings per share (EPS) for the same reason as long-term revenue growth. Compared to revenue, however, EPS highlights whether a company's growth was profitable.

Graham Corporation's full-year EPS flipped from negative to positive over the last five years. This is a good sign and shows it's at an inflection point.

In Q2, Graham Corporation reported EPS at $0.27, up from $0.25 in the same quarter last year. This print easily cleared analysts' estimates, and shareholders should be content with the results. Over the next 12 months, Wall Street expects Graham Corporation to grow its earnings. Analysts are projecting its EPS of $0.44 in the last year to climb by 61.2% to $0.72.

Key Takeaways from Graham Corporation's Q2 Results

We were impressed by how significantly Graham Corporation blew past analysts' EPS expectations this quarter. For the full year, the company reconfirmed its revenue guidance. Zooming out, we think this was still a decent, albeit mixed, quarter, showing the company is staying on track. The stock traded up 11.1% to $32.26 immediately after reporting.

So should you invest in Graham Corporation right now? When making that decision, it's important to consider its valuation, business qualities, as well as what has happened in the latest quarter. We cover that in our actionable full research report which you can read here, it's free.